How Does Carry in a Vc Partnership Vest

In venture capital (VC) partnerships, the concept of carry, or carried interest, plays a pivotal role in aligning the interests of general partners (GPs) and limited partners (LPs). Carry represents the share of profits that GPs earn from successful investments, typically after achieving a predetermined return threshold. However, the vesting of carry is a critical mechanism that ensures GPs remain committed to the long-term success of the fund. This article explores how carry vests in a VC partnership, examining the timelines, conditions, and implications for both GPs and LPs. Understanding this process is essential for anyone involved in or considering venture capital investments.

How Does Carry in a VC Partnership Vest?

In a venture capital (VC) partnership, carry refers to the share of profits that general partners (GPs) receive from the fund's successful investments. This is typically a percentage of the fund's profits, often around 20%, after returning the initial capital and any agreed-upon preferred returns to the limited partners (LPs). The vesting of carry determines how and when GPs earn their share of the profits over time. Vesting schedules are designed to align the interests of GPs with the long-term success of the fund and to incentivize them to remain actively involved in managing the investments.

See Also How Can Startup Companies Raise Money Initial Stage?

How Can Startup Companies Raise Money Initial Stage?What Is Carry in a VC Partnership?

Carry, or carried interest, is the portion of the profits that GPs earn from the fund's investments. It is a key component of compensation for GPs, as it rewards them for generating returns for the LPs. The carry is typically calculated as a percentage of the fund's profits, often 20%, after returning the initial capital and any preferred returns to the LPs. This structure ensures that GPs are incentivized to maximize the fund's performance.

How Does Carry Vesting Work?

Carry vesting refers to the process by which GPs earn their share of the carry over time. A typical vesting schedule might span 4 to 6 years, with a cliff period of 1 to 2 years. During the cliff period, no carry is vested. After the cliff, the carry vests monthly or quarterly until the full amount is earned. This structure ensures that GPs remain committed to the fund for the long term and are rewarded for their ongoing contributions.

See Also What are the pros and cons of going through accelerator programs like TechStars and Y Combinator?

What are the pros and cons of going through accelerator programs like TechStars and Y Combinator?What Are Common Vesting Schedules for Carry?

Vesting schedules for carry can vary, but they often follow a 4-year vesting period with a 1-year cliff. This means that GPs must remain with the fund for at least one year before any carry begins to vest. After the cliff, the carry vests monthly or quarterly over the remaining 3 years. Some funds may also include performance-based vesting, where additional carry is earned based on achieving specific milestones or returns.

What Happens to Unvested Carry If a GP Leaves?

If a GP leaves the fund before their carry is fully vested, the unvested portion is typically forfeited. This means that the GP will not receive any carry for the unvested portion. However, some funds may have provisions for partial vesting or accelerated vesting in certain circumstances, such as a GP's departure due to death or disability. These provisions are usually outlined in the fund's limited partnership agreement (LPA).

See AlsoHow Was Peter Thiel Able to Become a Venture Capitalist if He Had No Money to Invest to Begin WithHow Is Carry Distributed Among GPs?

The distribution of carry among GPs is usually determined by their ownership stakes or partnership agreements. In some cases, carry is distributed equally among all GPs, while in others, it may be allocated based on seniority, contribution, or performance. The specific distribution method is typically outlined in the fund's LPA and can vary significantly between different VC partnerships.

| Term | Definition |

|---|---|

| Carry | The share of profits that GPs earn from the fund's investments. |

| Vesting | The process by which GPs earn their carry over time. |

| Cliff Period | The initial period during which no carry is vested. |

| LPA | The legal agreement that outlines the terms of the fund, including carry vesting. |

| Performance-Based Vesting | Additional carry earned based on achieving specific milestones or returns. |

How much carry do VC partners get?

What is Carry in Venture Capital?

Carry, short for carried interest, is the share of profits that venture capital (VC) partners receive from the fund's successful investments. It is typically a percentage of the fund's profits after returning the initial capital to the limited partners (LPs). The standard carry percentage is around 20%, but this can vary depending on the fund's structure and agreements.

- Carry is a performance-based incentive for VC partners.

- It is calculated after returning the initial capital to LPs.

- The typical carry percentage is 20% of the profits.

How is Carry Distributed Among VC Partners?

The distribution of carry among VC partners depends on their roles, seniority, and contributions to the fund. Senior partners or founding partners often receive a larger share, while junior partners or associates may receive a smaller portion. The allocation is usually outlined in the fund's partnership agreement.

- Senior partners typically receive a larger share of carry.

- Junior partners or associates may receive a smaller portion.

- The distribution is detailed in the fund's partnership agreement.

What Factors Influence Carry Allocation?

Several factors influence how carry is allocated among VC partners, including their level of involvement in deal sourcing, due diligence, and portfolio management. Additionally, the fund's performance and the partners' tenure at the firm can also play a role in determining their share of carry.

- Involvement in deal sourcing and due diligence.

- Role in portfolio management and value creation.

- Fund performance and the partner's tenure at the firm.

What is the Vesting Schedule for Carry?

Carry often comes with a vesting schedule, meaning partners earn their share over time. A common vesting period is 4-6 years, with a one-year cliff. This ensures that partners remain committed to the fund for the long term and aligns their interests with those of the LPs.

- Carry typically vests over 4-6 years.

- Partners may face a one-year cliff before vesting begins.

- Vesting aligns partners' interests with the fund's long-term success.

How Does Carry Compare to Management Fees?

While carry is a share of the profits, VC partners also earn management fees, which are typically around 2% of the fund's committed capital annually. Management fees cover operational costs, while carry serves as a performance-based reward for generating returns.

- Management fees are usually 2% of committed capital.

- Fees cover operational costs, while carry rewards performance.

- Carry is a long-term incentive, unlike annual management fees.

How does carry work in a VC firm?

What is Carry in a Venture Capital Firm?

Carry, or carried interest, is the share of profits that venture capital (VC) professionals receive from the fund's successful investments. It is a key component of compensation for VC partners and is typically calculated as a percentage of the fund's profits, usually around 20%. The remaining 80% is returned to the limited partners (LPs) who invested in the fund. Carry incentivizes VCs to maximize returns, as their earnings are directly tied to the fund's performance.

- Carry is a profit-sharing mechanism between VC partners and LPs.

- It is typically calculated after the fund returns the initial capital to LPs.

- The standard carry percentage is 20%, but it can vary depending on the fund's terms.

How is Carry Distributed Among VC Partners?

Carry distribution among VC partners depends on the firm's structure and agreements. In most cases, carry is allocated based on seniority, contribution, and the role of each partner. Senior partners or founding members often receive a larger share, while junior partners or associates may receive a smaller portion. The distribution is outlined in the fund's operating agreement and can vary significantly between firms.

- Senior partners typically receive a larger share of carry.

- Junior partners or associates may receive a smaller percentage.

- The distribution is governed by the fund's operating agreement.

When is Carry Paid Out in a VC Fund?

Carry is paid out after the fund has returned the initial capital to its LPs and achieved a predetermined hurdle rate, often around 8%. This ensures that LPs receive their expected returns before the VC partners can claim their share of the profits. The timing of carry payouts depends on the fund's lifecycle, typically occurring during the later stages when successful exits (e.g., IPOs or acquisitions) generate returns.

- Carry is paid after returning the initial capital to LPs.

- A hurdle rate (e.g., 8%) must be met before carry is distributed.

- Payouts usually occur during the fund's later stages after successful exits.

What is the Difference Between Management Fees and Carry?

Management fees and carry are two distinct components of VC compensation. Management fees are annual fees, typically around 2% of the fund's committed capital, used to cover operational costs like salaries and office expenses. Carry, on the other hand, is a share of the fund's profits and is only earned if the fund performs well. While management fees provide steady income, carry aligns the interests of VC partners with those of the LPs by rewarding performance.

- Management fees are annual and cover operational costs.

- Carry is a performance-based share of the fund's profits.

- Management fees are typically 2% of committed capital.

How Does Carry Impact VC Decision-Making?

Carry plays a significant role in shaping VC decision-making by aligning the interests of the partners with the success of the fund. Since carry is only earned after achieving strong returns, VCs are incentivized to invest in high-potential startups and support their growth. This alignment ensures that VCs focus on long-term value creation rather than short-term gains, fostering a collaborative relationship with portfolio companies.

- Carry incentivizes VCs to invest in high-potential startups.

- It aligns the interests of VCs with the success of the fund.

- VCs focus on long-term value creation to maximize carry earnings.

How does a carried interest vest?

What is Carried Interest?

Carried interest is a share of the profits that investment managers receive as compensation, typically in private equity, hedge funds, or venture capital. It is often referred to as the carry and is usually a percentage of the fund's profits, commonly around 20%. This interest is earned after the fund's investors have received their initial capital and a predetermined rate of return, known as the hurdle rate.

- Carried interest is a performance-based incentive for fund managers.

- It is typically calculated as a percentage of the fund's profits, often 20%.

- Investors must first receive their initial capital and hurdle rate before carried interest is paid.

How Does Vesting Work for Carried Interest?

Vesting refers to the process by which fund managers earn the right to their carried interest over time. This mechanism ensures that managers remain committed to the fund's long-term success. Vesting schedules can vary but often span several years, with portions of the carried interest becoming available incrementally.

- Vesting schedules are designed to align the interests of fund managers with those of investors.

- Managers typically earn their carried interest over a period of 3 to 5 years.

- If a manager leaves before the vesting period is complete, they may forfeit unvested carried interest.

What Are the Common Vesting Schedules?

Vesting schedules for carried interest can vary depending on the fund's structure and agreements. Common schedules include cliff vesting, where the carried interest vests all at once after a certain period, and graded vesting, where it vests incrementally over time.

- Cliff vesting often occurs after 3 to 4 years of service.

- Graded vesting may allow for 20-25% of the carried interest to vest annually.

- Some funds use a hybrid approach, combining elements of both cliff and graded vesting.

What Happens if a Manager Leaves Before Vesting?

If a fund manager departs before their carried interest has fully vested, they may lose the unvested portion. This is intended to incentivize long-term commitment and discourage early exits. The specific terms are outlined in the fund's limited partnership agreement (LPA).

- Unvested carried interest is typically forfeited upon departure.

- The LPA governs the terms of vesting and forfeiture.

- Some agreements may allow for partial vesting based on the manager's tenure.

How is Carried Interest Taxed After Vesting?

Once carried interest vests, it is subject to taxation. In many jurisdictions, carried interest is taxed as capital gains rather than ordinary income, which typically results in a lower tax rate. However, tax regulations can vary, and some jurisdictions have specific rules for carried interest.

- Carried interest is often taxed at capital gains rates, which are lower than ordinary income rates.

- Tax treatment depends on the jurisdiction and specific regulations.

- Some countries have introduced legislation to tax carried interest as ordinary income.

How to calculate carry in VC?

What is Carry in Venture Capital?

Carry, or carried interest, is the share of profits that venture capital (VC) fund managers receive after returning the initial capital to investors. It is a performance-based incentive that aligns the interests of fund managers with those of the investors. Typically, carry is calculated as a percentage of the fund's profits, often around 20%, after the investors have received their initial investment back.

- Carry is a percentage of the fund's profits.

- It is usually around 20% of the profits.

- Investors receive their initial investment back before carry is distributed.

How is Carry Calculated?

To calculate carry, you first need to determine the total profits of the fund. This is done by subtracting the total amount of capital invested from the total returns generated by the fund. Once the profits are determined, the carry is calculated as a percentage of these profits. For example, if a fund generates $100 million in returns from a $50 million investment, the profit is $50 million. A 20% carry would then be $10 million.

- Subtract the total capital invested from the total returns to determine profits.

- Apply the carry percentage (e.g., 20%) to the profits.

- Distribute the carry to the fund managers after returning the initial capital to investors.

What is the Hurdle Rate in Carry Calculation?

The hurdle rate is the minimum rate of return that a VC fund must achieve before carry is paid out to the fund managers. This ensures that investors receive a certain level of return before the managers can take their share of the profits. The hurdle rate is often set at around 8% annually, but it can vary depending on the fund's terms.

- The hurdle rate is the minimum return required before carry is paid.

- It is typically set at around 8% annually.

- The hurdle rate protects investors by ensuring they receive a baseline return.

What is the Difference Between Committed Capital and Distributed Capital?

Committed capital refers to the total amount of money that investors have pledged to the fund, while distributed capital is the amount that has actually been invested or returned to investors. Carry is calculated based on the profits generated from the distributed capital, not the committed capital. This distinction is important because it affects how and when carry is paid out.

- Committed capital is the total amount pledged by investors.

- Distributed capital is the amount actually invested or returned.

- Carry is calculated based on profits from distributed capital.

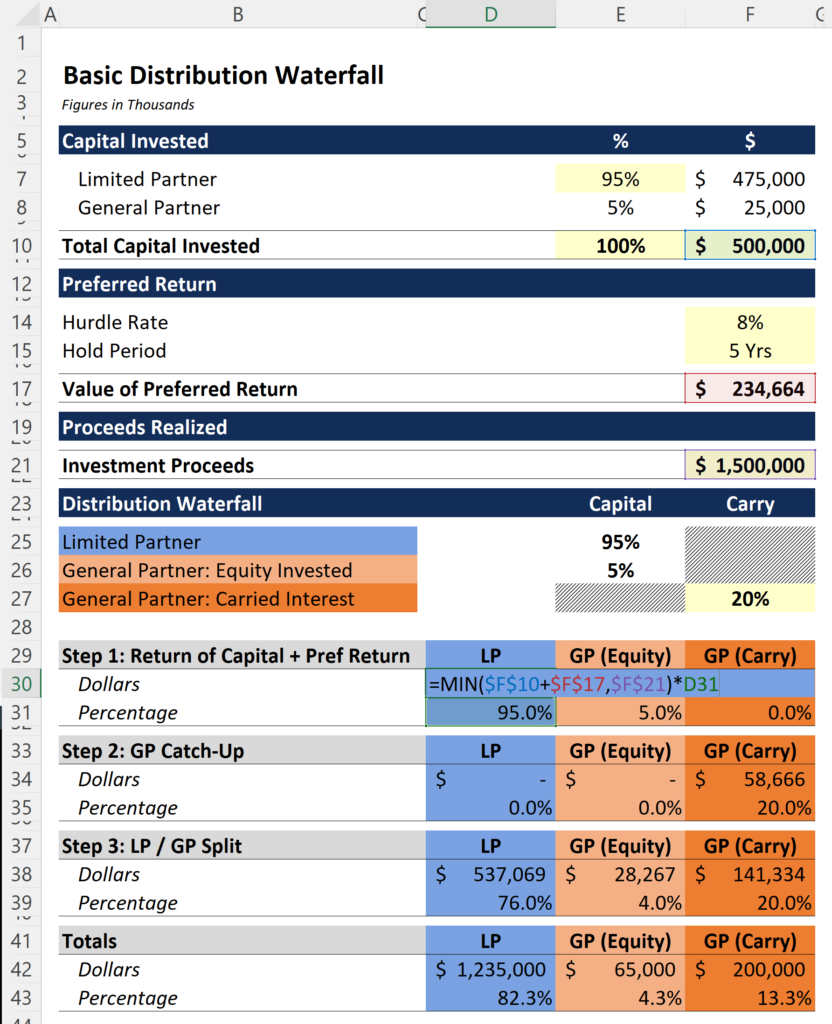

How Does the Waterfall Structure Affect Carry Calculation?

The waterfall structure outlines the order in which profits are distributed among investors and fund managers. Typically, investors receive their initial capital back first, followed by any returns up to the hurdle rate. Only after these conditions are met does the carry get distributed to the fund managers. This structure ensures that investors are prioritized in the distribution of profits.

- The waterfall structure dictates the order of profit distribution.

- Investors receive their initial capital and hurdle rate returns first.

- Carry is distributed to fund managers only after investor conditions are met.

Frequently Asked Questions (FAQs)

What is vesting in a VC partnership carry context?

Vesting in a VC partnership carry refers to the process by which partners earn their share of the carried interest over time. Carried interest, or carry, is the portion of the profits that the general partners (GPs) receive from the fund's investments, typically around 20%. Vesting ensures that GPs remain committed to the fund for a specified period, usually several years, before they can fully claim their share of the carry. This mechanism aligns the interests of the GPs with those of the limited partners (LPs) by incentivizing long-term performance and dedication.

How does the vesting schedule work for carry in a VC partnership?

The vesting schedule for carry in a VC partnership is typically structured over a period of 3 to 5 years, with a cliff period at the beginning. A common structure is a 4-year vesting period with a 1-year cliff, meaning that no carry is vested until the GP has been with the partnership for at least one year. After the cliff, the carry vests monthly or quarterly over the remaining period. If a GP leaves before the vesting period is complete, they forfeit the unvested portion of their carry, ensuring that only those who contribute to the fund's success over the long term benefit.

What happens to unvested carry if a GP leaves the VC partnership?

If a GP leaves the VC partnership before their carry is fully vested, the unvested portion is typically forfeited. This means that the GP will not receive any share of the carry that has not yet vested. The forfeited carry may be reallocated among the remaining GPs or returned to the LPs, depending on the terms of the partnership agreement. This policy is designed to protect the interests of the LPs and ensure that only those who have contributed to the fund's success over the required period benefit from the carry.

Can vesting terms for carry be negotiated in a VC partnership?

Yes, the vesting terms for carry in a VC partnership can often be negotiated, especially for senior or founding partners. While standard vesting schedules are common, experienced GPs or those with significant influence in the partnership may negotiate more favorable terms, such as a shorter vesting period or a larger initial vesting percentage. However, any deviations from the standard terms must be agreed upon by all parties involved, including the LPs, to ensure that the interests of all stakeholders are adequately protected.

Leave a Reply

Our Recommended Articles