What is the Typical Structure of a Vc Fund?

Venture capital (VC) funds play a pivotal role in fueling innovation by providing capital to startups and high-growth companies. Understanding the typical structure of a VC fund is essential for entrepreneurs, investors, and anyone interested in the venture ecosystem. These funds are typically organized as limited partnerships, comprising general partners (GPs) who manage the fund and limited partners (LPs) who provide the capital. The structure includes key elements such as fund size, investment strategy, management fees, carried interest, and the lifecycle of the fund. This article explores the foundational components of a VC fund, shedding light on how they operate and generate returns for stakeholders.

What is the Typical Structure of a VC Fund?

A Venture Capital (VC) fund is a pooled investment vehicle that provides capital to early-stage, high-potential, and often high-risk startups. The structure of a VC fund is designed to align the interests of the investors (Limited Partners) and the fund managers (General Partners) while managing risks and maximizing returns. Below, we break down the typical structure of a VC fund into key components.

See Also How Do Vc Firms Raise Their Funds?

How Do Vc Firms Raise Their Funds?1. Limited Partners (LPs) and General Partners (GPs)

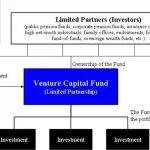

The Limited Partners (LPs) are the investors who provide the capital for the VC fund. These can include institutional investors, high-net-worth individuals, and family offices. The General Partners (GPs) are the fund managers responsible for making investment decisions, managing the portfolio, and ensuring the fund's success. LPs have limited liability, meaning they are not involved in day-to-day operations, while GPs assume full responsibility for managing the fund.

2. Fund Lifecycle

A VC fund typically has a lifecycle of 10 years, divided into two main phases: the investment period (first 3-5 years) and the harvesting period (remaining years). During the investment period, the fund deploys capital into startups. In the harvesting period, the focus shifts to exiting investments through IPOs, acquisitions, or secondary sales to return profits to LPs.

See Also How Do the Different Types of Partners in a Venture Capital Firm Differ General Partner Operating Partner Investment Partner Etc

How Do the Different Types of Partners in a Venture Capital Firm Differ General Partner Operating Partner Investment Partner Etc3. Management Fees and Carried Interest

VC funds charge management fees, usually around 2% of the committed capital, to cover operational costs. Additionally, GPs earn carried interest, typically 20% of the profits, after returning the initial capital to LPs. This structure incentivizes GPs to generate high returns.

4. Investment Strategy and Portfolio Construction

VC funds follow a specific investment strategy, such as focusing on a particular industry (e.g., tech, healthcare) or stage (e.g., seed, Series A). They build a diversified portfolio of 20-30 startups to spread risk. The goal is to have a few home runs that generate outsized returns to offset losses from other investments.

See Also How Much Do Analysts Senior Analysts at Vc Firms Make How is Compensation Structured

How Much Do Analysts Senior Analysts at Vc Firms Make How is Compensation Structured5. Legal and Regulatory Framework

VC funds operate under a legal structure, often as a limited partnership, to provide liability protection and tax advantages. They must comply with regulatory requirements, such as SEC regulations in the U.S., and adhere to investment agreements that outline terms like capital commitments, distribution waterfalls, and reporting obligations.

| Component | Description |

|---|---|

| Limited Partners (LPs) | Investors who provide capital but have no operational role. |

| General Partners (GPs) | Fund managers responsible for investment decisions and operations. |

| Fund Lifecycle | Typically 10 years, divided into investment and harvesting periods. |

| Management Fees | ~2% of committed capital to cover operational costs. |

| Carried Interest | ~20% of profits earned by GPs after returning initial capital to LPs. |

| Investment Strategy | Focus on specific industries or stages to build a diversified portfolio. |

| Legal Structure | Often a limited partnership for liability protection and tax benefits. |

How are VC funds structured?

What is the General Structure of a VC Fund?

Venture capital (VC) funds are typically structured as limited partnerships, where the fund operates as the general partner (GP) and the investors serve as limited partners (LPs). The GP manages the fund's operations, including making investment decisions, while the LPs provide the capital. The structure ensures that LPs have limited liability, meaning they are only liable up to the amount they invest. The fund's lifespan is usually 10 years, with an option to extend for a few more years to manage exits.

- General Partner (GP): Manages the fund and makes investment decisions.

- Limited Partners (LPs): Provide capital and have limited liability.

- Fund Lifespan: Typically 10 years, with possible extensions.

How is Capital Committed and Called in VC Funds?

In VC funds, capital is committed by LPs at the outset, but it is not immediately transferred. Instead, the GP calls capital as needed for investments or operational expenses. This process is known as capital calls or drawdowns. LPs are usually given notice before a capital call, and they must fulfill their commitment within a specified timeframe. This structure allows the fund to manage cash flow efficiently and ensures that capital is only used when necessary.

- Capital Commitment: LPs promise a specific amount of capital.

- Capital Calls: GP requests funds as needed for investments.

- Drawdowns: LPs transfer funds upon request.

What are the Key Terms in VC Fund Agreements?

VC fund agreements include several key terms that define the relationship between the GP and LPs. These terms include the management fee, which is typically 2% of the committed capital, and the carried interest, usually 20% of the profits. Other terms include the hurdle rate, which is the minimum return LPs must receive before the GP can claim carried interest, and the clawback provision, which ensures that the GP returns excess carried interest if the fund underperforms.

- Management Fee: Typically 2% of committed capital.

- Carried Interest: Usually 20% of profits.

- Hurdle Rate: Minimum return required before GP earns carried interest.

How are VC Fund Investments Managed?

VC funds invest in early-stage or high-growth companies, often in exchange for equity. The GP conducts due diligence to identify promising startups and negotiates terms such as valuation and equity stakes. Once an investment is made, the GP may take an active role in the company, providing guidance and leveraging their network to help the startup grow. The goal is to achieve a successful exit, either through an IPO or an acquisition, which generates returns for both the GP and LPs.

- Due Diligence: GP evaluates potential investments.

- Equity Stakes: Fund acquires ownership in startups.

- Active Involvement: GP may assist in company growth.

What is the Role of Limited Partners in VC Funds?

Limited partners (LPs) are the primary source of capital for VC funds. They include institutional investors like pension funds, endowments, and family offices, as well as high-net-worth individuals. LPs have limited control over the fund's operations but rely on the GP's expertise to generate returns. In return for their investment, LPs receive a share of the profits, typically after the GP takes its carried interest. LPs also benefit from diversification, as their capital is spread across multiple startups.

- Institutional Investors: Major source of capital.

- Limited Control: LPs rely on GP for decision-making.

- Profit Sharing: LPs receive returns after GP's carried interest.

What is the hierarchy of a VC fund?

Understanding the Structure of a VC Fund

The hierarchy of a venture capital (VC) fund is designed to manage investments, decision-making, and operations efficiently. At the top, the Limited Partners (LPs) provide the capital, while the General Partners (GPs) manage the fund and make investment decisions. Below them, the Investment Team handles due diligence and portfolio management, and the Advisory Board offers strategic guidance.

- Limited Partners (LPs): These are the investors who provide the capital for the fund, such as institutional investors, high-net-worth individuals, or family offices.

- General Partners (GPs): They are responsible for managing the fund, making investment decisions, and ensuring returns for the LPs.

- Investment Team: This group conducts due diligence, evaluates startups, and manages the portfolio companies.

Roles and Responsibilities of Limited Partners (LPs)

Limited Partners (LPs) are the backbone of a VC fund, providing the necessary capital to fuel investments. They typically include institutional investors, pension funds, and wealthy individuals. Their primary role is to invest capital while leaving the management and decision-making to the General Partners (GPs).

- Capital Providers: LPs supply the funds but do not engage in day-to-day operations.

- Risk Takers: They bear the financial risk of the investments.

- Passive Role: LPs rely on the expertise of GPs to generate returns.

General Partners (GPs): The Decision-Makers

The General Partners (GPs) are the driving force behind a VC fund. They are responsible for sourcing deals, making investment decisions, and managing the portfolio. GPs often have significant experience in entrepreneurship, finance, or specific industries, enabling them to identify high-potential startups.

- Deal Sourcing: GPs identify and evaluate potential investment opportunities.

- Investment Decisions: They decide which startups to fund and negotiate terms.

- Portfolio Management: GPs work closely with portfolio companies to ensure growth and success.

The Investment Team: Executing the Strategy

The Investment Team plays a critical role in executing the fund's strategy. This team includes analysts, associates, and principals who conduct due diligence, analyze market trends, and support portfolio companies. They are the hands-on professionals who ensure that the fund's investments align with its goals.

- Due Diligence: The team evaluates startups' financials, market potential, and team capabilities.

- Market Analysis: They research industry trends to identify promising sectors.

- Portfolio Support: They assist portfolio companies with strategic advice and operational support.

The Advisory Board: Strategic Guidance

The Advisory Board provides strategic guidance to the VC fund. Composed of industry experts, successful entrepreneurs, and seasoned investors, this board helps the fund navigate complex decisions and capitalize on emerging opportunities.

- Expertise: Members bring deep industry knowledge and experience.

- Strategic Input: They offer insights on market trends and investment strategies.

- Network Access: The board often provides valuable connections for the fund and its portfolio companies.

What is the 80/20 rule in venture capital?

The 80/20 rule in venture capital refers to the observation that a small percentage of investments (typically around 20%) generate the majority of returns (around 80%). This principle highlights the importance of identifying and focusing on high-potential startups, as most investments may not yield significant returns. Venture capitalists often rely on this rule to prioritize their portfolio strategies and allocate resources effectively.

Understanding the 80/20 Rule in Venture Capital

The 80/20 rule, also known as the Pareto Principle, is a concept that suggests a disproportionate relationship between inputs and outputs. In venture capital, this means that a small fraction of investments drive the majority of profits. Key points include:

- 20% of investments typically account for 80% of returns.

- This rule emphasizes the importance of selective investment strategies.

- It highlights the high-risk, high-reward nature of venture capital.

Why the 80/20 Rule Matters in Venture Capital

The 80/20 rule is crucial for venture capitalists because it helps them focus on maximizing returns while managing risks. Key reasons include:

- It encourages investors to identify and support high-potential startups.

- It underscores the need for diversification to mitigate losses from underperforming investments.

- It provides a framework for resource allocation and decision-making.

How Venture Capitalists Apply the 80/20 Rule

Venture capitalists use the 80/20 rule to optimize their investment strategies. Practical applications include:

- Focusing on due diligence to identify startups with the highest growth potential.

- Allocating more resources to portfolio companies that show early signs of success.

- Using the rule to evaluate and refine investment criteria over time.

Challenges of the 80/20 Rule in Venture Capital

While the 80/20 rule is a useful guideline, it comes with challenges. These include:

- Difficulty in predicting which startups will succeed.

- The risk of overconcentration in a few investments.

- Potential missed opportunities by focusing too narrowly on high-potential startups.

Examples of the 80/20 Rule in Venture Capital

The 80/20 rule is evident in many successful venture capital portfolios. Examples include:

- Sequoia Capital's investment in Apple, which generated outsized returns compared to other investments.

- Accel's early investment in Facebook, which became a significant portion of their portfolio's success.

- Andreessen Horowitz's bet on Instagram, which yielded massive returns after its acquisition by Facebook.

What is the 2:20 rule in venture capital?

What is the 2:20 Rule in Venture Capital?

The 2:20 rule in venture capital refers to the standard fee structure that venture capital (VC) firms typically charge their investors. This rule outlines that VC firms charge a 2% management fee on the total committed capital and a 20% performance fee (also known as carried interest) on the profits generated from investments. This structure aligns the interests of the VC firm with those of the investors, as the firm earns more when the investments perform well.

How Does the 2% Management Fee Work?

The 2% management fee is an annual fee charged by VC firms to cover operational costs, such as salaries, office expenses, and due diligence activities. Here’s how it works:

- The fee is calculated based on the total committed capital from investors.

- It is typically charged for the duration of the fund’s life, which is usually 10 years.

- This fee ensures that the VC firm has the resources to manage the fund effectively, even if the investments do not yield immediate returns.

What is the 20% Performance Fee?

The 20% performance fee, or carried interest, is the share of profits that the VC firm earns after returning the initial capital to investors. Key points include:

- This fee is only applied once the fund has returned the principal investment to the investors.

- It incentivizes the VC firm to maximize returns, as their earnings are directly tied to the fund’s success.

- The remaining 80% of profits are distributed to the investors.

Why is the 2:20 Rule Important in Venture Capital?

The 2:20 rule is crucial because it establishes a clear and standardized compensation model for VC firms. Its importance lies in:

- Aligning the interests of the VC firm and the investors by linking compensation to performance.

- Providing transparency in how fees are calculated and distributed.

- Ensuring that VC firms have the necessary resources to operate while being motivated to achieve high returns.

How Does the 2:20 Rule Impact Investors?

The 2:20 rule has significant implications for investors, including:

- Investors must account for the 2% management fee as an ongoing cost, which reduces the overall returns.

- The 20% performance fee means that investors receive 80% of the profits, which can still be substantial if the fund performs well.

- This structure encourages investors to carefully evaluate the track record and expertise of the VC firm before committing capital.

Are There Variations to the 2:20 Rule?

While the 2:20 rule is standard, there can be variations depending on the VC firm and the fund’s terms. Some examples include:

- Lower management fees (e.g., 1.5%) for larger funds or repeat investors.

- Higher performance fees (e.g., 25%) for funds with exceptional track records.

- Hurdle rates, where the VC firm only earns carried interest after achieving a minimum return threshold for investors.

Frequently Asked Questions (FAQs)

What is the typical structure of a VC fund?

A venture capital (VC) fund is typically structured as a limited partnership, consisting of general partners (GPs) and limited partners (LPs). The GPs are responsible for managing the fund, making investment decisions, and overseeing portfolio companies. The LPs, on the other hand, are the investors who provide the capital but have limited involvement in the day-to-day operations. The fund is usually established for a fixed term, often 10 years, with the possibility of extensions. During this period, the GPs invest in high-potential startups, aiming for significant returns.

How are VC funds typically financed?

VC funds are primarily financed through commitments from limited partners (LPs), which can include institutional investors like pension funds, endowments, and insurance companies, as well as high-net-worth individuals. These LPs commit a certain amount of capital to the fund, which is drawn down over time as the GPs identify and invest in promising startups. The fund may also charge a management fee, typically around 2% of the committed capital, to cover operational expenses. Additionally, GPs often receive a carried interest, usually around 20%, which is a share of the profits once the LPs have received their initial investment back.

What are the key stages in a VC fund's lifecycle?

The lifecycle of a VC fund can be divided into several key stages. The fundraising stage involves securing commitments from LPs. Once the fund is closed, the investment period begins, during which the GPs actively seek out and invest in startups. This is followed by the management and growth stage, where the GPs work closely with portfolio companies to help them scale. Finally, the exit stage involves selling the investments, either through an initial public offering (IPO) or a merger and acquisition (M&A), to realize returns for the LPs. The entire lifecycle typically spans 10 to 12 years.

What are the risks associated with investing in a VC fund?

Investing in a VC fund carries several risks. The most significant is the illiquidity of the investments, as capital is locked up for the duration of the fund's lifecycle. There is also a high risk of capital loss, as many startups fail to achieve profitability. Additionally, the returns are highly variable and depend on the success of a few standout investments. The long-term horizon of VC funds means that investors must be patient and prepared for potential delays in realizing returns. Despite these risks, the potential for high returns makes VC funds an attractive option for many investors.

Leave a Reply

Our Recommended Articles