Whats a Better Way to Structure a Vc Fund Evergreen or Regular Vc

Venture capital (VC) funds are a cornerstone of innovation, fueling startups and driving economic growth. However, the traditional VC model, with its fixed lifespan and rigid structure, is increasingly being challenged by the evergreen fund approach. While regular VC funds operate on a 10-year cycle, requiring exits and distributions to limited partners, evergreen funds are designed to reinvest returns indefinitely, offering greater flexibility and long-term alignment with portfolio companies. This article explores the key differences between these two structures, examining their advantages, drawbacks, and suitability for different investment strategies. By understanding these models, investors and entrepreneurs can better navigate the evolving landscape of venture capital.

What’s a Better Way to Structure a VC Fund: Evergreen or Regular VC?

What is an Evergreen VC Fund?

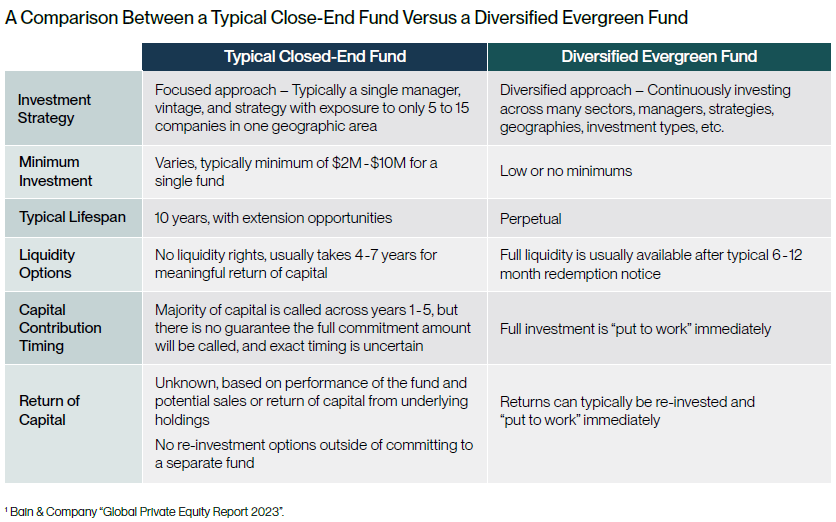

An Evergreen VC Fund is a venture capital fund that does not have a fixed lifespan. Instead, it operates on a continuous cycle, reinvesting returns from successful exits back into new investments. This structure allows the fund to remain active indefinitely, providing long-term support to startups and avoiding the pressure of traditional fund lifecycles.

See Also Why Are There So Many Venture Capitalists and Businesses Moving to Miami From San Francisco

Why Are There So Many Venture Capitalists and Businesses Moving to Miami From San FranciscoWhat is a Regular VC Fund?

A Regular VC Fund follows a traditional structure with a fixed lifespan, typically around 10 years. It raises capital from limited partners (LPs), invests in startups during the investment period (usually 3-5 years), and then focuses on managing and exiting those investments to return profits to LPs within the fund’s lifecycle.

Key Differences Between Evergreen and Regular VC Funds

The main differences lie in their lifespan, capital recycling, and investment strategy. Evergreen funds focus on long-term growth and reinvestment, while regular VC funds prioritize timely exits and returns to LPs within a set timeframe. Evergreen funds are often more flexible but may face challenges in aligning investor expectations.

See Also Why Should I Choose Equity Crowdfunding Instead of Venture Capital

Why Should I Choose Equity Crowdfunding Instead of Venture CapitalAdvantages of an Evergreen VC Fund

Evergreen funds offer flexibility and long-term alignment with portfolio companies. They avoid the pressure of fundraising cycles and can support startups through multiple growth stages. Additionally, they benefit from compounding returns as profits are reinvested into new opportunities.

Advantages of a Regular VC Fund

Regular VC funds provide a clear structure and defined timelines, which can align well with investor expectations. They also allow LPs to realize returns within a predictable timeframe, making them a more traditional and widely understood model in the venture capital industry.

See Also What is the Hierarchy Like at a Venture Capital Firm and How Long Does It Take to Reach Each Level

What is the Hierarchy Like at a Venture Capital Firm and How Long Does It Take to Reach Each Level| Aspect | Evergreen VC Fund | Regular VC Fund |

|---|---|---|

| Lifespan | Indefinite | Fixed (typically 10 years) |

| Capital Recycling | Yes | No |

| Investment Strategy | Long-term, flexible | Time-bound, exit-focused |

| Investor Alignment | Long-term growth | Timely returns |

| Fundraising Pressure | Low | High (every 3-5 years) |

What are the disadvantages of evergreen funds?

Limited Liquidity for Investors

Evergreen funds often have limited liquidity compared to traditional investment funds. This can pose challenges for investors who need quick access to their money. Key points include:

- Investors may face lock-up periods or restrictions on withdrawals.

- Liquidity is often tied to the fund's ability to sell underlying assets, which can be slow or difficult.

- This lack of liquidity can be a significant disadvantage during financial emergencies or market downturns.

Higher Management Fees

Evergreen funds typically charge higher management fees compared to other investment vehicles. These fees can erode returns over time. Key points include:

- Management fees are often used to cover ongoing operational costs, which can be substantial.

- Investors may also face additional charges, such as performance fees or administrative costs.

- These higher fees can make evergreen funds less attractive compared to lower-cost alternatives.

Complex Structure and Transparency Issues

The structure of evergreen funds can be complex and opaque, making it difficult for investors to fully understand their investments. Key points include:

- Investors may struggle to assess the true value of the fund's assets due to limited transparency.

- The fund's structure can involve multiple layers, such as special purpose vehicles, which add complexity.

- This lack of clarity can lead to misunderstandings or misaligned expectations between investors and fund managers.

Potential for Conflicts of Interest

Evergreen funds may be prone to conflicts of interest between investors and fund managers. Key points include:

- Fund managers may prioritize their own financial interests over those of the investors.

- Decisions about reinvesting profits or distributing returns can create tension between stakeholders.

- These conflicts can undermine trust and lead to dissatisfaction among investors.

Exposure to Market Risks

Evergreen funds are not immune to market risks, which can impact their performance. Key points include:

- Fluctuations in the value of underlying assets can lead to losses for investors.

- Economic downturns or sector-specific challenges can negatively affect the fund's returns.

- Unlike closed-end funds, evergreen funds may not have a fixed investment horizon, exposing investors to prolonged market volatility.

What is the 80/20 rule in venture capital?

The 80/20 rule in venture capital refers to the observation that a small percentage of investments (typically around 20%) generate the majority of returns (around 80%). This principle, also known as the Pareto Principle, highlights the uneven distribution of outcomes in venture capital, where a few high-performing startups drive most of the profits for investors.

Understanding the 80/20 Rule in Venture Capital

The 80/20 rule is a fundamental concept in venture capital that emphasizes the importance of identifying and investing in high-potential startups. Key points include:

- Uneven returns: Most venture capital funds rely on a small number of investments to deliver the bulk of their returns.

- Risk management: Investors accept that many startups will fail, but the few that succeed can compensate for losses.

- Focus on outliers: Venture capitalists prioritize finding startups with the potential to become unicorns or billion-dollar companies.

Why the 80/20 Rule Matters in Venture Capital

The 80/20 rule is critical for venture capitalists because it shapes their investment strategy and decision-making process. Key reasons include:

- Portfolio construction: Investors build diversified portfolios to increase the chances of finding high-performing startups.

- Resource allocation: Venture capitalists focus their time and resources on startups with the highest growth potential.

- Performance metrics: The rule helps investors evaluate the success of their portfolios based on a few standout investments.

How Venture Capitalists Apply the 80/20 Rule

Venture capitalists use the 80/20 rule to guide their investment approach and maximize returns. Key strategies include:

- Early-stage investments: Investing in startups during their early stages to capture higher growth potential.

- Due diligence: Conducting thorough research to identify startups with disruptive technologies or business models.

- Follow-on funding: Providing additional capital to high-performing startups to fuel their growth.

Examples of the 80/20 Rule in Venture Capital

The 80/20 rule is evident in the success stories of many venture capital funds. Notable examples include:

- Sequoia Capital: Investments in companies like Apple, Google, and Airbnb have driven the majority of their returns.

- Andreessen Horowitz: Their stakes in Facebook, Twitter, and Slack have contributed significantly to their overall performance.

- Accel Partners: Early investments in companies like Dropbox and Spotify have yielded substantial returns.

Challenges of the 80/20 Rule in Venture Capital

While the 80/20 rule is a guiding principle, it also presents challenges for venture capitalists. Key challenges include:

- Identifying outliers: Predicting which startups will succeed is inherently uncertain and difficult.

- High failure rates: Many startups fail, requiring investors to have a high tolerance for risk.

- Competition: The race to invest in high-potential startups can drive up valuations and reduce returns.

How to structure a venture capital fund?

Understanding the Legal Framework

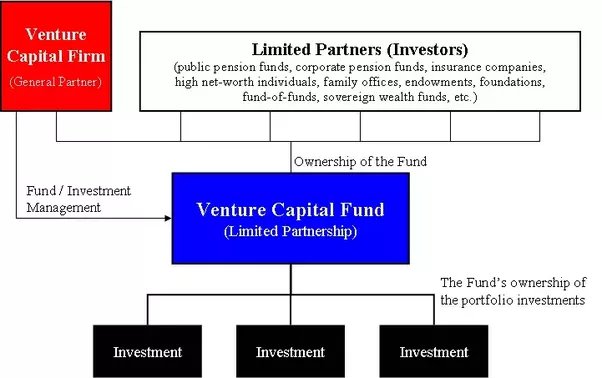

Structuring a venture capital fund begins with understanding the legal framework. This involves selecting the appropriate legal structure, which is typically a limited partnership (LP). Here are the key steps:

- Choose the jurisdiction: Select a jurisdiction with favorable tax laws and regulations for venture capital funds.

- Draft the partnership agreement: This document outlines the roles, responsibilities, and profit-sharing arrangements between the general partners (GPs) and limited partners (LPs).

- Register the fund: Ensure compliance with local regulations by registering the fund with the appropriate authorities.

Defining the Fund's Investment Strategy

A clear investment strategy is crucial for the success of a venture capital fund. This strategy should align with the fund's goals and the expertise of its management team. Consider the following:

- Target industries: Identify the industries or sectors the fund will focus on, such as technology, healthcare, or clean energy.

- Investment stages: Decide whether the fund will invest in early-stage startups, growth-stage companies, or a mix of both.

- Geographic focus: Determine if the fund will invest locally, regionally, or globally.

Raising Capital from Limited Partners

Raising capital is a critical step in structuring a venture capital fund. This involves securing commitments from limited partners (LPs), such as institutional investors, high-net-worth individuals, and family offices. Key considerations include:

- Develop a compelling pitch: Highlight the fund's unique value proposition, track record, and potential returns.

- Set a target fund size: Determine the amount of capital to be raised, considering the fund's investment strategy and market conditions.

- Negotiate terms: Agree on terms such as management fees, carried interest, and the fund's lifespan with LPs.

Establishing the Fund's Management Team

The management team plays a pivotal role in the success of a venture capital fund. This team is responsible for sourcing deals, conducting due diligence, and managing portfolio companies. Important steps include:

- Assemble a skilled team: Recruit professionals with expertise in investment, industry knowledge, and operational experience.

- Define roles and responsibilities: Clearly outline the roles of general partners (GPs), investment managers, and other key personnel.

- Establish decision-making processes: Create a structured process for evaluating and approving investments.

Setting Up Operational Infrastructure

An efficient operational infrastructure is essential for managing a venture capital fund. This includes setting up systems for fund administration, compliance, and reporting. Key elements to consider are:

- Fund administration: Choose a fund administrator to handle accounting, investor reporting, and regulatory compliance.

- Technology and tools: Implement software for deal flow management, portfolio tracking, and performance analysis.

- Compliance and reporting: Ensure adherence to regulatory requirements and establish regular reporting mechanisms for LPs.

What is the 2:20 rule in venture capital?

What is the 2:20 Rule in Venture Capital?

The 2:20 rule in venture capital refers to the standard fee structure that venture capital (VC) firms typically charge their investors. This rule outlines that VC firms take a 2% management fee on the total committed capital and a 20% performance fee (also known as carried interest) on the profits generated from investments. This structure aligns the interests of the VC firm with those of the investors, as the firm earns more when the investments perform well.

How Does the 2% Management Fee Work?

The 2% management fee is an annual charge that covers the operational costs of the VC firm. Here’s how it works:

- The fee is calculated based on the total amount of capital committed by investors.

- It is used to pay for salaries, office expenses, due diligence, and other administrative costs.

- This fee is typically charged for the life of the fund, which is usually 10 years, but it may decrease after the investment period ends.

What is the 20% Performance Fee (Carried Interest)?

The 20% performance fee, or carried interest, is the share of profits that the VC firm earns after returning the initial capital to investors. Key points include:

- It is only earned once the fund has returned the principal amount to investors.

- This fee incentivizes the VC firm to maximize returns, as their earnings are directly tied to the fund's success.

- Carried interest is often subject to a hurdle rate, ensuring investors receive a minimum return before the VC firm takes its share.

Why is the 2:20 Rule Important in Venture Capital?

The 2:20 rule is crucial because it establishes a clear and standardized compensation model for VC firms. Its importance lies in:

- Aligning the interests of investors and fund managers by linking compensation to performance.

- Providing transparency in how VC firms are compensated for their services.

- Encouraging VC firms to focus on generating high returns to earn their carried interest.

How Does the 2:20 Rule Impact Investors?

For investors, the 2:20 rule has several implications:

- It ensures that VC firms are motivated to deliver strong returns, as their earnings depend on it.

- Investors must account for the 2% management fee, which reduces the overall capital available for investments.

- The 20% carried interest means investors share a portion of the profits, but only after achieving a return on their initial investment.

Are There Variations to the 2:20 Rule?

While the 2:20 rule is standard, some VC firms may negotiate different terms. Variations include:

- Lower management fees (e.g., 1.5%) for larger funds or repeat investors.

- Higher carried interest (e.g., 25%) for funds targeting higher-risk, higher-reward strategies.

- Custom hurdle rates or clawback provisions to protect investors' interests.

Frequently Asked Questions (FAQs)

What is the difference between an evergreen VC fund and a regular VC fund?

Evergreen VC funds and regular VC funds differ primarily in their structure and lifespan. A regular VC fund typically has a fixed lifespan, usually around 10 years, during which it raises capital, makes investments, and eventually exits those investments to return profits to its limited partners (LPs). In contrast, an evergreen VC fund operates on a perpetual or rolling basis, continuously raising and deploying capital without a fixed end date. This structure allows evergreen funds to reinvest returns and maintain a long-term investment horizon, making them more flexible but also potentially more complex to manage.

What are the advantages of an evergreen VC fund structure?

The evergreen VC fund structure offers several advantages. First, it provides long-term flexibility, allowing fund managers to hold investments for extended periods without the pressure of a fixed timeline. This can be particularly beneficial for startups that require more time to mature. Second, evergreen funds can reinvest returns into new opportunities, creating a self-sustaining cycle of capital deployment. Additionally, this structure can attract investors seeking consistent returns over time, as it avoids the need to frequently raise new funds. However, it requires strong governance and alignment between LPs and fund managers to ensure long-term success.

What are the challenges of managing an evergreen VC fund?

Managing an evergreen VC fund comes with unique challenges. One major issue is the need for continuous fundraising, as the fund relies on ongoing contributions from LPs to sustain its operations. This can be more demanding than the traditional VC model, where capital is raised in fixed cycles. Additionally, the lack of a fixed timeline can create alignment challenges between LPs and fund managers, as LPs may have different expectations regarding liquidity and returns. Furthermore, the perpetual nature of evergreen funds requires robust governance and transparency to ensure that the fund’s strategy remains aligned with its investors’ goals over the long term.

Which type of VC fund structure is better for startups?

The choice between an evergreen VC fund and a regular VC fund depends on the startup’s needs and growth trajectory. Evergreen funds may be better suited for startups that require long-term support and are not pressured to deliver quick exits, as these funds can provide sustained capital and mentorship over many years. On the other hand, regular VC funds might be more appropriate for startups aiming for rapid growth and exit, as the fixed timeline aligns with the need to achieve milestones within a specific period. Ultimately, startups should consider the fund’s investment philosophy, timeline, and alignment with their own goals when choosing between these structures.

Leave a Reply

Our Recommended Articles