Slingshot Rental Business Insurance

Operating a slingshot rental business offers a thrilling opportunity in the growing recreational vehicle market, but it also comes with unique risks that demand careful risk management. As these three-wheeled vehicles attract adventure-seeking customers, owners must navigate potential liabilities, from accidents and property damage to customer injuries. Comprehensive insurance is essential to safeguard assets, ensure regulatory compliance, and maintain customer trust. Key coverage options include general liability, collision, and comprehensive policies, alongside protections against theft or vandalism. Tailoring insurance plans to address specific operational needs—such as seasonal demand or fleet size—can further mitigate financial exposure. Understanding these protections is critical for sustaining a resilient and profitable slingshot rental venture.

- Understanding Slingshot Rental Business Insurance: Coverage and Essentials

-

What insurance do I need for a rental business?

- What Types of Insurance Are Essential for a Rental Business?

- Why Do Rental Businesses Need Liability Coverage?

- How Does Equipment Breakdown Insurance Protect Rental Businesses?

- Is Business Interruption Insurance Necessary for Rental Companies?

- What Role Does Workers’ Compensation Play in a Rental Business?

- Do you need insurance to drive a slingshot?

- How much is insurance for a bike rental business?

- What kind of insurance do you need for a trailer rental business?

-

Frequently Asked Questions (FAQs)

- What types of insurance coverage are essential for a slingshot rental business?

- How does slingshot rental insurance handle customer-related accidents?

- Are there specific state requirements for insuring slingshot rental businesses?

- What factors influence the cost of slingshot rental business insurance?

Understanding Slingshot Rental Business Insurance: Coverage and Essentials

Why Slingshot Rental Businesses Need Specialized Insurance

Slingshot rental businesses face unique risks due to the high-performance nature of these vehicles and their exposure to inexperienced drivers. Standard auto insurance policies often exclude commercial rental activities or lack adequate coverage for liabilities like third-party injuries, vehicle damage, or legal disputes. Specialized insurance ensures protection against collision repairs, theft, and customer injury claims, which are critical for financial stability.

See AlsoBusiness Insurance for Candle Makers| Coverage Type | Key Protections | Exclusions |

|---|---|---|

| Liability Insurance | Covers third-party injuries/property damage | Intentional misconduct |

| Collision Coverage | Repairs for rental vehicle damage | Wear and tear |

| Comprehensive Insurance | Theft, vandalism, natural disasters | Mechanical failures |

Key Liability Risks in Slingshot Rentals

Liability risks include accidents caused by renters, passenger injuries, and property damage. Without proper coverage, businesses may face lawsuits or out-of-pocket expenses. For example, if a renter crashes into another vehicle, the business could be held liable for medical bills or legal fees.

| Risk Category | Potential Costs | Insurance Solution |

|---|---|---|

| Bodily Injury | Hospitalization, lawsuits | General liability insurance |

| Property Damage | Vehicle repairs, third-party claims | Commercial auto liability |

How to Choose the Right Insurance Policy

Evaluate policies based on coverage limits, deductibles, and exclusions. Look for insurers familiar with recreational vehicle rentals. Ensure the policy covers uninsured/underinsured motorists and includes on-hook towing for breakdowns. Compare quotes and read reviews to avoid gaps in protection.

See AlsoAuto Detailing Business Insurance| Factor | Consideration | Example |

|---|---|---|

| Coverage Limits | Minimum state requirements vs. optimal protection | $1M liability limit |

| Deductible Costs | Impact on premiums | $500–$1,000 per claim |

Cost Factors for Slingshot Rental Insurance

Premiums depend on fleet size, vehicle value, rental location, and driver screening processes. Urban areas with higher accident rates may incur higher costs. Discounts are often available for safety features like GPS tracking or driver training programs.

| Factor | Impact on Cost | Mitigation Strategy |

|---|---|---|

| Location | High-traffic areas = higher risk | Choose low-risk zones |

| Driver Age | Under 25 = higher premiums | Enforce age restrictions |

Common Claims and How to Avoid Them

Frequent claims include collision damage, theft, and liability disputes. Mitigate risks by implementing pre-rental inspections, security deposits, and mandatory safety briefings. Use telematics devices to monitor renter behavior and reduce reckless driving.

See AlsoCan You Get Business Insurance Without a Business License| Claim Type | Preventive Measure | Tool/Policy |

|---|---|---|

| Collision | Pre-rental vehicle checks | Checklist documentation |

| Theft | GPS tracking systems | Real-time monitoring |

What insurance do I need for a rental business?

What Types of Insurance Are Essential for a Rental Business?

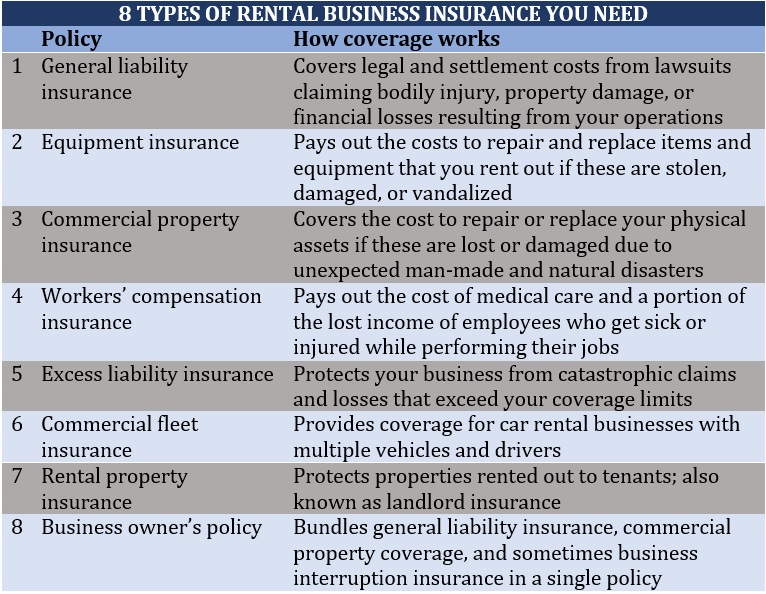

For a rental business, general liability insurance is critical to protect against third-party claims like bodily injury or property damage. Property insurance covers physical assets, such as buildings, equipment, or inventory. Additionally, commercial auto insurance is necessary if you use vehicles for deliveries or rentals.

- General Liability Insurance: Covers legal fees, medical costs, and settlements from accidents involving customers.

- Property Insurance: Safeguards your rental location, tools, or stored goods from fire, theft, or natural disasters.

- Commercial Auto Insurance: Protects company vehicles and drivers against accidents or damages during business use.

Why Do Rental Businesses Need Liability Coverage?

Liability coverage shields your business from financial risks if a customer or vendor sues for injuries or damages. Product liability insurance is also vital if you rent out equipment, as it covers harm caused by defective items.

- Third-Party Claims: Addresses lawsuits from slip-and-fall accidents or property damage on your premises.

- Product Liability: Covers legal costs if rented equipment malfunctions and causes harm.

- Advertising Injury: Protects against claims of slander, copyright infringement, or misleading advertising.

How Does Equipment Breakdown Insurance Protect Rental Businesses?

Equipment breakdown insurance covers repairs or replacements if machinery or rented tools fail due to mechanical or electrical issues. This prevents unexpected costs from disrupting operations.

- Repair Costs: Pays for fixing or replacing damaged equipment.

- Business Interruption: Compensates for lost income during downtime.

- Additional Expenses: Covers temporary rentals or expedited shipping for replacement parts.

Is Business Interruption Insurance Necessary for Rental Companies?

Business interruption insurance helps recover lost income and operating expenses if your rental business halts due to covered events like fires or floods.

- Income Replacement: Compensates for lost revenue during closures.

- Ongoing Expenses: Covers rent, payroll, and utilities while operations pause.

- Relocation Costs: Funds temporary workspace if your primary location is unusable.

What Role Does Workers’ Compensation Play in a Rental Business?

Workers’ compensation insurance is legally required in most regions if you have employees. It covers medical bills and lost wages for work-related injuries or illnesses.

- Employee Protection: Pays for treatment and rehabilitation costs.

- Legal Compliance: Avoids fines or penalties for non-compliance.

- Lawsuit Prevention: Reduces the risk of employees suing over workplace injuries.

Do you need insurance to drive a slingshot?

Is Insurance Legally Required to Drive a Slingshot?

Yes, in most U.S. states, insurance is legally required to drive a Polaris Slingshot. While classification varies by state, the Slingshot is often categorized as an autocycle or three-wheeled motorcycle, which typically mandates liability insurance.

- State laws differ: For example, states like Florida classify it as an autocycle, requiring motorcycle-like insurance, while others treat it as a car.

- Minimum liability coverage: Most states require coverage for bodily injury and property damage.

- Proof of insurance: You may need to show proof during traffic stops or registration renewals.

What Happens If You Drive a Slingshot Without Insurance?

Driving a Slingshot without insurance can result in severe penalties, including fines, license suspension, or even vehicle impoundment.

- Legal fines: Penalties range from $100 to over $1,000, depending on the state.

- License repercussions: Repeat offenses may lead to suspended driving privileges.

- Financial risk: You’re personally liable for damages or injuries in an accident.

Does Financing a Slingshot Affect Insurance Requirements?

If you finance or lease a Slingshot, lenders typically require full coverage insurance to protect their investment.

- Comprehensive and collision: Lenders often mandate these to cover theft, vandalism, or accidents.

- Higher premiums: Full coverage costs more but ensures financial protection for both you and the lender.

- Lease agreements: Failure to maintain coverage may breach the contract, leading to repossession.

What Types of Insurance Coverage Are Recommended for a Slingshot?

Beyond legal minimums, additional coverage options provide broader protection.

- Collision insurance: Covers repairs to your Slingshot after an accident.

- Uninsured motorist coverage: Protects you if the at-fault driver lacks insurance.

- Accessory coverage: Insures custom upgrades like audio systems or paint jobs.

How Does Slingshot Classification Impact Insurance Costs?

The Slingshot’s unique classification as an autocycle or motorcycle influences insurance rates.

- Lower rates in some states: If classified as a motorcycle, premiums may be cheaper than car insurance.

- Safety features: Some insurers offer discounts for stability control or anti-theft devices.

- Driver history: Clean records and completion of motorcycle safety courses can reduce costs.

How much is insurance for a bike rental business?

Factors Influencing Bike Rental Business Insurance Costs

The cost of insurance for a bike rental business depends on variables like location, number of bikes, and coverage types. High-traffic urban areas may incur higher premiums due to theft or accident risks. Similarly, businesses with larger fleets or premium bikes face increased liability exposure. Common factors include:

- Business size: More bikes or employees raise costs.

- Coverage limits: Higher liability limits increase premiums.

- Claims history: Prior incidents may lead to higher rates.

Types of Insurance Coverage for Bike Rental Businesses

Insurance policies for bike rentals typically include general liability, property insurance, and inland marine coverage. Optional add-ons like non-owned vehicle insurance or equipment breakdown coverage may apply. Key options:

- General Liability: Covers third-party injuries or property damage.

- Commercial Property Insurance: Protects bikes, shops, and gear.

- Inland Marine Insurance: Covers bikes during transit or off-site use.

Average Insurance Costs for Bike Rental Businesses

Annual premiums for bike rental insurance range from $1,000 to $5,000+, depending on scale. A small operation with 10 bikes might pay $1,200–$2,500, while larger fleets could exceed $7,000. Breakdowns include:

- General Liability: $500–$1,500 annually.

- Commercial Property Insurance: $300–$1,000 per year.

- Workers’ Compensation: Required if hiring staff; varies by state.

Businesses can lower costs through risk mitigation strategies and policy adjustments. Examples include installing GPS trackers or requiring rental agreements. Effective methods:

- Safety Training: Educate staff and customers on bike safety.

- Secure Storage: Invest in locked facilities to deter theft.

- Higher Deductibles: Opting for higher deductibles reduces premiums.

State-Specific Insurance Requirements for Bike Rentals

Insurance regulations vary by state, particularly for liability minimums and workers’ compensation. For example, California mandates higher liability limits for tourist-heavy areas. Considerations include:

- Liability Minimums: States like Florida require $1M+ coverage for coastal rentals.

- Seasonal Adjustments: Premiums may fluctuate in seasonal markets (e.g., Colorado ski towns).

- Local Permits: Some cities require proof of insurance for business licenses.

What kind of insurance do you need for a trailer rental business?

General Liability Insurance

General liability insurance is essential for a trailer rental business to protect against third-party claims of bodily injury, property damage, or personal injury. This coverage addresses legal fees, medical expenses, and settlements if a customer or bystander is harmed during trailer use. For example, if a rented trailer accidentally damages a client’s property, this insurance would cover repair costs.

- Bodily injury claims: Covers medical bills if someone is injured due to trailer operations.

- Property damage: Pays for repairs if the trailer damages a third party’s property.

- Legal defense costs: Handles attorney fees and court expenses in lawsuits.

Commercial Auto Insurance

Commercial auto insurance is critical for vehicles used to tow or transport trailers. Standard personal auto policies often exclude business-related activities, leaving gaps in coverage. This insurance protects against accidents, theft, or vandalism involving company vehicles or trailers in transit.

- Collision coverage: Repairs or replaces vehicles/trailers damaged in accidents.

- Liability coverage: Addresses injuries or damages caused to others while towing.

- Uninsured motorist protection: Covers costs if an at-fault driver lacks insurance.

Physical Damage Coverage

Physical damage coverage specifically protects rented trailers against accidental damage, such as collisions, fires, or theft. This ensures the business can repair or replace trailers without significant financial loss, even if the renter is at fault.

- Comprehensive coverage: Covers non-collision incidents (e.g., weather, theft).

- Collision reimbursement: Pays for repairs after accidents.

- Renter negligence: Addresses damages caused by improper trailer use.

Inland Marine Insurance

Inland marine insurance covers trailers while they are rented, transported, or stored off-premises. It bridges gaps left by other policies, ensuring protection during transit or temporary storage at a client’s location.

- Transit coverage: Protects trailers during transportation.

- Off-premises damage: Covers losses occurring away from the business’s primary location.

- Equipment breakdown: Addresses mechanical failures during rentals.

Workers’ Compensation Insurance

If the business has employees, workers’ compensation insurance is legally required in most states. It covers medical costs and lost wages if employees are injured while maintaining, towing, or handling trailers.

- Medical expenses: Pays for treatment of work-related injuries.

- Disability benefits: Supports employees unable to work temporarily or permanently.

- Employer liability: Protects against lawsuits from injured employees.

Frequently Asked Questions (FAQs)

What types of insurance coverage are essential for a slingshot rental business?

Liability insurance is critical for protecting your business against claims involving bodily injury or property damage caused by renters. Additionally, collision and comprehensive coverage safeguards your slingshots against accidents, theft, or vandalism. You may also need uninsured/underinsured motorist coverage to address incidents involving drivers without adequate insurance. Finally, contingent liability coverage can fill gaps when renters fail to purchase their required insurance policies.

If a customer causes an accident while renting your slingshot, your commercial auto insurance policy typically covers third-party injuries or property damage, subject to your policy limits. However, if the renter’s negligence exceeds coverage limits, umbrella insurance may provide additional protection. Ensure your policy includes rental reimbursement coverage to offset income loss during vehicle repairs. Always verify that renters sign a liability waiver to clarify their financial responsibilities in case of incidents.

Are there specific state requirements for insuring slingshot rental businesses?

Insurance requirements vary by state, but most mandate minimum liability coverage for bodily injury and property damage. For example, states like California or Florida may require higher coverage limits due to tourism-heavy traffic. Some states also enforce physical damage coverage for rented vehicles. Consult a local insurance agent or legal expert to ensure compliance with state-specific regulations, such as mandatory uninsured motorist coverage or rental agreement disclosures.

What factors influence the cost of slingshot rental business insurance?

Premiums depend on factors like your business location, as high-traffic or urban areas often pose greater risks. The size of your fleet and slingshot models (e.g., higher-performance vehicles) also impact costs. Your claims history, chosen deductibles, and coverage limits play significant roles. Insurers may offer discounts for implementing safety programs, GPS tracking, or requiring renters to complete driver training. Regularly review policies to balance cost and coverage as your business scales.

Leave a Reply

Our Recommended Articles