Computer Repair Business Insurance

Running a computer repair business involves navigating a complex landscape of technical challenges and client expectations. While expertise in hardware and software is essential, safeguarding your venture with the right insurance coverage is equally critical. From accidental damage to sensitive equipment and data breaches to potential liability claims, unexpected risks can threaten your operations and reputation. Comprehensive business insurance tailored to the IT industry helps mitigate these vulnerabilities, offering protection against property loss, professional errors, cyber incidents, and more. Understanding the types of coverage available—such as general liability, professional liability, and commercial property insurance—ensures your business remains resilient in an ever-evolving digital world.

Understanding the Importance of Insurance for Computer Repair Businesses

Computer repair business insurance is essential to protect your company from financial losses caused by risks like property damage, liability claims, or data breaches. Whether you operate from a storefront or provide on-site services, accidents, errors, or unforeseen events can disrupt operations and lead to costly lawsuits. Insurance policies tailored for computer repair businesses help mitigate these risks, covering expenses like client device damage, professional negligence claims, or cybersecurity incidents. Investing in comprehensive coverage ensures business continuity and builds trust with clients.

See Also As a Vc or Business Angel What is Your Checklist When You Invest in a Startup

As a Vc or Business Angel What is Your Checklist When You Invest in a StartupCommon Types of Insurance for Computer Repair Businesses

Computer repair businesses should consider several insurance policies to address industry-specific risks. General liability insurance covers third-party bodily injury or property damage, such as a client slipping in your store. Professional liability insurance (errors and omissions) protects against claims of inadequate work, like failing to repair a device properly. Commercial property insurance safeguards your physical assets, including tools and inventory, from fire or theft. Additionally, cyber liability insurance is critical for addressing data breaches involving client information.

| Insurance Type | Coverage | Key Benefits |

|---|---|---|

| General Liability | Third-party injuries/property damage | Legal fee coverage, settlements |

| Professional Liability | Negligence claims | Client compensation, legal defense |

| Commercial Property | Physical assets | Replacement costs, repairs |

| Cyber Liability | Data breaches | Notification costs, fines |

Factors Influencing Insurance Costs

Insurance premiums for computer repair businesses depend on factors like business size, coverage limits, and location. A larger company with multiple employees may pay higher premiums due to increased liability exposure. Opting for higher deductibles can lower costs but requires paying more out-of-pocket during claims. Your business’s claims history and the types of services offered (e.g., handling sensitive data) also affect pricing.

See Also What's the Typical Route to Becoming a Vc?

What's the Typical Route to Becoming a Vc?| Factor | Impact on Cost |

|---|---|

| Business Size | Larger teams = higher risk |

| Coverage Limits | Higher limits = higher premiums |

| Location | High-risk areas increase costs |

| Services Offered | Data handling = cyber liability |

How to Choose the Right Insurance Policy

Selecting the right insurance involves assessing your business’s unique risks. Start by identifying vulnerabilities, such as client data exposure or equipment damage. Compare policies from multiple providers, focusing on coverage exclusions and claim response times. Consult an insurance broker specializing in tech businesses to tailor a policy bundle. Ensure your plan includes equipment breakdown coverage if you rely on specialized tools.

| Step | Action |

|---|---|

| Risk Assessment | Identify liabilities (e.g., data, devices) |

| Compare Providers | Review coverage terms, costs |

| Consult Experts | Brokers or legal advisors |

| Customize Policy | Add endorsements as needed |

Why Cyber Liability Insurance is Non-Negotiable

Cyber liability insurance is crucial for computer repair businesses due to the rising threat of data breaches and ransomware attacks. If client data is compromised during repairs, your business could face regulatory fines, lawsuits, and reputational damage. This coverage helps pay for forensic investigations, customer notifications, and legal defense costs. Without it, a single breach could devastate a small business financially.

See AlsoHow to Dissolve an LLC in Alabama| Coverage Aspect | Details |

|---|---|

| Data Breach Response | Covers investigation and notifications |

| Regulatory Fines | Assists with GDPR/state penalties |

| Legal Fees | Defense against lawsuits |

| Ransomware | Negotiation and recovery costs |

Filing an insurance claim requires thorough documentation. For example, if a client sues over a botched repair, gather service records, communication logs, and witness statements. Notify your insurer immediately to avoid delays. For property damage claims, provide photos and repair estimates. Work closely with adjusters to ensure fair compensation, and keep records of all interactions.

| Claim Type | Required Documentation |

|---|---|

| Professional Liability | Service agreements, client complaints |

| Property Damage | Photos, repair invoices |

| Cyber Liability | Breach reports, forensic analysis |

How much does a $1,000,000 liability insurance policy cost?

Venture Capital Investment Bootcamp Randall Reade's Posts

Venture Capital Investment Bootcamp Randall Reade's PostsThe cost of a $1,000,000 liability insurance policy varies widely depending on factors like industry, business size, location, claims history, and coverage specifics. On average, small businesses might pay between $300 and $1,500 annually, while high-risk industries like construction could see premiums ranging from $5,000 to $25,000+ per year.

Factors Influencing the Cost of a $1,000,000 Liability Insurance Policy

The premium for a $1 million liability policy is determined by multiple variables.

- Industry risk level: High-risk sectors (e.g., construction, healthcare) face higher premiums.

- Business size: Revenue, payroll, and number of employees impact costs.

- Location: States with higher litigation rates or stricter regulations may increase prices.

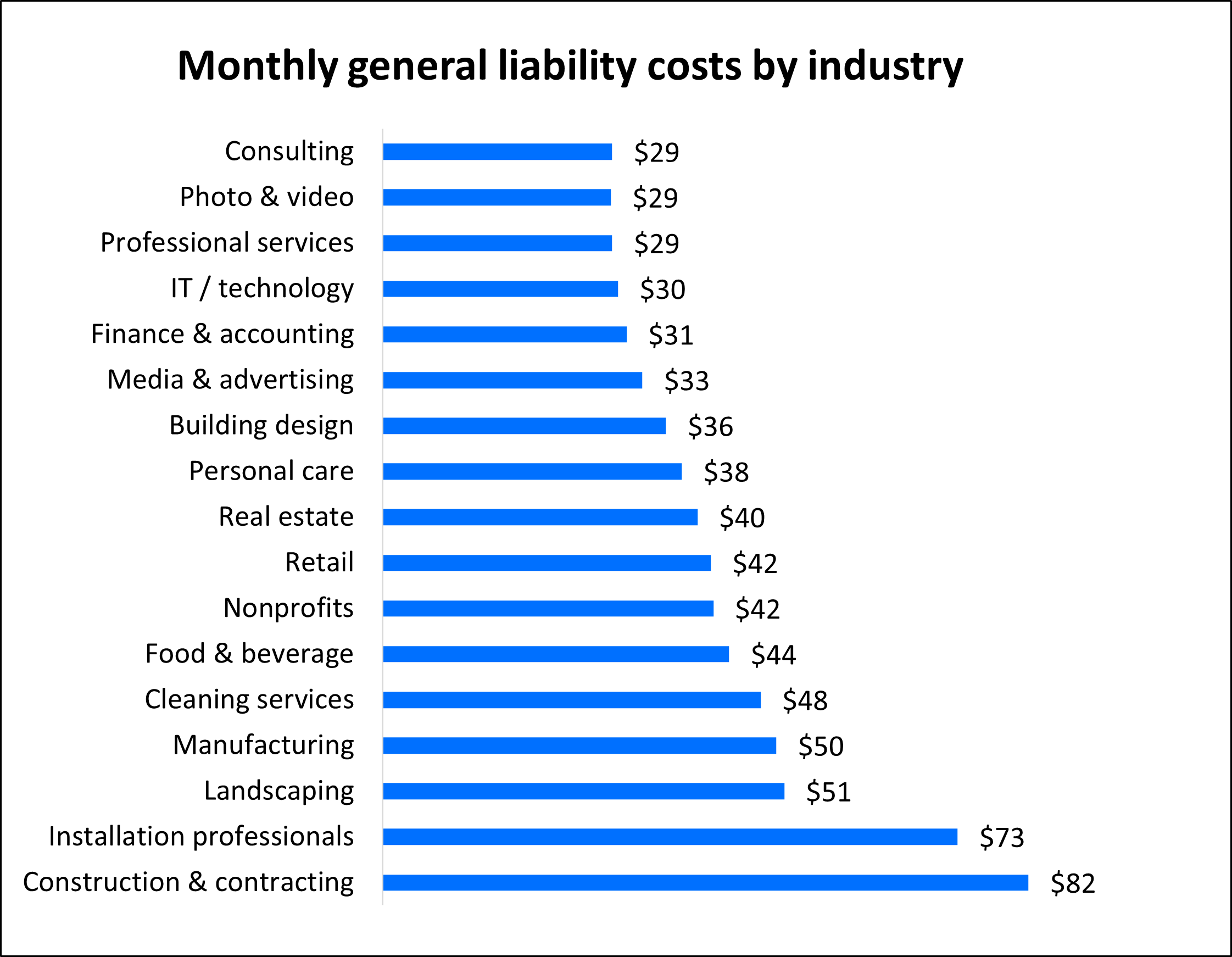

Average Costs by Industry for $1 Million Liability Coverage

Industries with higher liability risks typically pay more for coverage.

- Retail or consulting: $300–$1,200 annually for low-risk operations.

- Contractors: $5,000–$15,000+ due to physical risks and project complexity.

- Medical professionals: $7,000–$25,000+ annually for malpractice-heavy policies.

Larger businesses generally pay more due to increased exposure.

- Revenue: Higher income often correlates with greater liability risks.

- Number of employees: More staff may lead to higher workplace injury risks.

- Payroll size: Insurers use payroll as a metric for pricing in some industries.

State Regulations and Their Impact on Insurance Costs

Location plays a key role in determining premiums.

- Lawsuit frequency: States like California or Florida may have higher rates due to litigation trends.

- Minimum coverage requirements: Some states mandate higher coverage levels.

- Local risks: Areas prone to natural disasters may increase policy costs.

Businesses can take steps to lower their insurance expenses.

- Risk management: Implement safety protocols to minimize claims.

- Bundle policies: Combine liability insurance with other coverages for discounts.

- Increase deductibles: Opting for higher deductibles can reduce annual premiums.

What is business PC insurance?

What is Business PC Insurance?

Business PC insurance is a specialized policy designed to protect companies from financial losses due to damage, theft, or malfunctions of business-critical computers and related hardware. It typically covers repair costs, replacements, and sometimes even data recovery expenses. This insurance ensures minimal disruption to operations by safeguarding against risks like accidental damage, cyberattacks, or hardware failures.

Coverage Details of Business PC Insurance

Business PC insurance policies vary but generally include protection for physical damage, theft, and software-related issues. Some policies extend to cover data breaches or cyber incidents linked to insured devices.

- Hardware protection: Covers repairs or replacements for damaged components like screens, keyboards, or motherboards.

- Theft coverage: Compensates for stolen devices, often requiring proof of ownership and police reports.

- Cyber incident support: May include costs for malware removal or data recovery after an attack.

Key Benefits of Business PC Insurance

Investing in business PC insurance offers financial security and operational continuity. It reduces downtime and ensures businesses can recover swiftly from unexpected events.

- Minimized financial losses: Avoid out-of-pocket expenses for repairs or replacements.

- Business continuity: Fast resolution of issues keeps workflows uninterrupted.

- Liability coverage: Some policies protect against third-party claims from device-related incidents.

How Business PC Insurance Works

Business PC insurance operates through a structured claims process. After purchasing a policy, businesses pay premiums based on risk factors like device count or industry type.

- Policy purchase: Select coverage tiers (e.g., basic, comprehensive) tailored to business needs.

- Incident reporting: Notify the insurer immediately after an event, providing evidence like photos or invoices.

- Claim resolution: Insurers assess the claim and approve payouts or repairs as per policy terms.

Choosing the Right Business PC Insurance Policy

Selecting a suitable policy requires evaluating coverage scope, exclusions, and provider reliability.

- Assess risks: Identify vulnerabilities like frequent travel with devices or high cyberattack exposure.

- Compare providers: Review insurers’ claim response times and customer reviews.

- Review exclusions: Ensure accidental damage or cyber threats aren’t excluded from coverage.

Cost Factors for Business PC Insurance

Premiums depend on variables like device value, coverage limits, and business size.

- Number of devices: More PCs typically increase premiums.

- Coverage level: Comprehensive plans with cyber protection cost more than basic hardware coverage.

- Deductibles: Higher deductibles lower premiums but increase out-of-pocket costs during claims.

Does commercial insurance cover repairs?

What Types of Repairs Are Typically Covered by Commercial Insurance?

Commercial insurance may cover repairs resulting from covered perils, such as fire, vandalism, or water damage, depending on the policy. For example:

- Fire damage repairs to structures or equipment.

- Fixing water damage from burst pipes (but not floods, unless specified).

- Restoring vandalism-related damages, like broken windows or graffiti removal.

What Factors Determine Whether Repairs Are Covered?

Coverage depends on the policy type, cause of damage, and exclusions. Key factors include:

- Policy scope: General liability, property insurance, or specialized policies.

- Cause of damage: Covered perils (e.g., storms) vs. excluded events (e.g., wear and tear).

- Maintenance obligations: Insurers may deny claims if repairs stem from negligence.

Does Commercial Insurance Cover Routine Maintenance Repairs?

No, commercial insurance generally excludes routine maintenance, as it’s considered the owner’s responsibility. Examples include:

- HVAC system servicing or replacing worn-out parts.

- Repairing fading paint or minor structural wear.

- Addressing plumbing leaks due to aging pipes (unless sudden/accidental).

How to File a Repair Claim Under Commercial Insurance?

To file a claim, follow these steps:

- Document damage with photos, videos, and repair estimates.

- Notify your insurer promptly and submit required forms.

- Cooperate with adjusters to validate the claim’s legitimacy.

What Repairs Are Commonly Excluded from Commercial Insurance?

Exclusions often involve preventable or gradual damage. Typical exclusions include:

- Earthquake or flood repairs (unless added via endorsements).

- Fixing code violations uncovered during repairs.

- Damages from intentional acts or poor maintenance.

Does business insurance cover broken windows?

Does Business Insurance Cover Broken Windows?

Business insurance may cover broken windows depending on the type of policy and the cause of damage. Standard commercial property insurance, often included in a Business Owner’s Policy (BOP), typically covers damage caused by covered perils such as vandalism, fire, or severe weather. However, accidental breakage or wear and tear may not be covered unless specified in the policy. Review your policy details or consult your insurer to confirm coverage specifics.

Does Commercial Property Insurance Cover Broken Windows?

Commercial property insurance generally covers broken windows if the damage results from a covered peril. These perils often include:

- Vandalism: Broken windows due to intentional acts of destruction.

- Natural disasters: Damage from storms, hail, or wind.

- Fire or explosions: Shattered windows caused by fire-related incidents.

If the damage is due to excluded causes, such as gradual wear, coverage may not apply.

What Causes of Broken Windows Are Typically Covered?

Most policies cover sudden, accidental, or external causes. Common covered scenarios include:

- Theft or burglary: Broken windows during a break-in.

- Weather-related damage: Hurricanes, tornadoes, or heavy snowfall.

- Vehicle collisions: Accidents involving cars or equipment.

Exclusions often involve preventable maintenance issues or intentional acts by the policyholder.

Are There Exclusions for Window Damage in Business Insurance?

Yes, exclusions vary by policy but often include:

- Gradual deterioration: Cracks from age or poor maintenance.

- Employee negligence: Damage caused by staff mishandling.

- Earthquakes or floods: Unless add-on coverage is purchased.

Always verify policy exclusions to avoid unexpected out-of-pocket costs.

How to File a Claim for a Broken Window?

Follow these steps to file a claim:

- Document the damage: Take photos and note the cause.

- Review your policy: Confirm coverage limits and deductibles.

- Contact your insurer: Submit evidence and a repair estimate.

Prompt reporting improves the likelihood of a smooth claims process.

Can Preventative Measures Affect Window Damage Coverage?

Proactive steps may influence coverage and premiums:

- Install security systems: Reduces risk of vandalism or theft-related claims.

- Regular maintenance: Addresses wear before it leads to damage.

- Impact-resistant glass: May qualify for premium discounts.

Insurers often reward risk-mitigation efforts with better terms.

Frequently Asked Questions (FAQs)

What Types of Insurance Do Computer Repair Businesses Need?

Computer repair businesses typically require several types of insurance to mitigate risks. General liability insurance is essential to cover third-party bodily injuries or property damage. Professional liability insurance (errors and omissions) protects against claims of negligence or faulty repairs. Commercial property insurance safeguards your equipment, tools, and workspace from theft, fire, or natural disasters. Additionally, cyber liability insurance is critical to address data breaches or client data loss. Depending on your operations, you may also need workers' compensation if you have employees.

Why Is Professional Liability Insurance Important for Computer Repair Businesses?

Professional liability insurance is vital for computer repair businesses because it covers claims arising from mistakes or oversights in your services. For example, if a client accuses your business of data loss, misdiagnosis, or failed repairs that caused financial harm, this policy helps cover legal fees, settlements, or judgments. Without it, your business could face significant out-of-pocket expenses, damaging your reputation and finances.

How Much Does Computer Repair Business Insurance Cost?

The cost of insurance varies based on factors like business size, location, coverage limits, and claims history. On average, a small computer repair business might pay between $500 and $3,000 annually for a comprehensive policy. General liability insurance typically starts at around $300 per year, while professional liability insurance may range from $800 to $2,000. Bundling policies through a Business Owner’s Policy (BOP) can reduce costs by combining coverage types at a discounted rate.

Does Computer Repair Business Insurance Cover Data Breaches?

Standard general liability insurance does not cover data breaches. However, adding cyber liability insurance to your policy protects against costs related to data breaches, such as notifying affected clients, credit monitoring services, legal fees, and regulatory fines. This coverage is crucial for computer repair businesses that handle sensitive client data, as breaches can lead to severe financial and reputational damage. Ensure your policy includes first-party and third-party cyber coverage for comprehensive protection.

Leave a Reply

Our Recommended Articles