Can I Start an Insurance Company as a Sole Proprietor?

Starting an insurance company as a sole proprietor is a question many aspiring entrepreneurs ponder, especially those drawn to the industry’s potential for steady revenue and client impact. While a sole proprietorship offers simplicity in setup and direct control over business decisions, the insurance sector is heavily regulated, raising unique challenges. Licensing requirements, financial solvency standards, and compliance with state-specific regulations are critical considerations. Additionally, personal liability exposure in a claims-driven industry may pose significant risks. This article explores whether launching an insurance venture as a sole proprietor is feasible, examining legal frameworks, operational hurdles, and strategies to mitigate potential drawbacks in this complex field.

-

Can You Start an Insurance Company as a Sole Proprietor?

- Legal Requirements for Starting an Insurance Company as a Sole Proprietor

- Licensing and Regulatory Compliance for Sole Proprietor Insurance Businesses

- Financial Considerations and Capital Requirements

- Risks and Liabilities of Operating as a Sole Proprietor in Insurance

- Alternatives to Sole Proprietorship for Insurance Startups

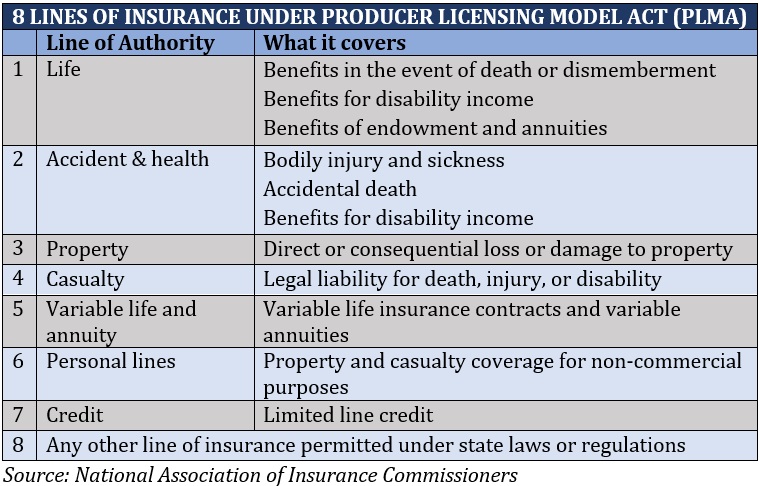

- What licenses do you need to open an insurance company?

- How much capital do you need to start an insurance company?

- Do I need an LLC as an insurance agent?

-

Frequently Asked Questions (FAQs)

- Can I Legally Start an Insurance Company as a Sole Proprietor?

- What Are the Risks of Running an Insurance Company as a Sole Proprietor?

- Are There Alternatives to a Sole Proprietorship for Starting an Insurance Company?

- What Licenses and Certifications Are Required to Start an Insurance Company as a Sole Proprietor?

Can You Start an Insurance Company as a Sole Proprietor?

Starting an insurance company as a sole proprietor is legally possible in many jurisdictions, but it comes with significant challenges. Insurance businesses are heavily regulated, requiring adherence to strict licensing, capital requirements, and compliance standards. As a sole proprietor, you’d bear unlimited personal liability for business debts or legal claims, which is risky in an industry prone to high-stakes disputes. Additionally, securing partnerships with reinsurers or meeting state-mandated financial reserves might be difficult without a corporate structure. While a sole proprietorship offers simplicity in setup, the insurance sector’s complexity often makes forming an LLC or corporation a safer choice.

See Also Is 50 Million Enough Money to Start a Vc Firm and Become a Billionaire

Is 50 Million Enough Money to Start a Vc Firm and Become a BillionaireLegal Requirements for Starting an Insurance Company as a Sole Proprietor

To operate an insurance company as a sole proprietor, you must fulfill state-specific licensing and regulatory obligations. This includes obtaining an insurance producer license or agency license, depending on your services. You’ll also need to demonstrate financial stability, often through minimum capital reserves. Compliance with insurance laws, such as filing policy forms and adhering to consumer protection standards, is mandatory.

| Requirement | Description |

| Business Registration | Register your business name and structure with local authorities. |

| Licensing | Obtain state insurance licenses (e.g., producer, adjuster, or agency licenses). |

| Compliance | Follow state insurance codes and federal regulations (e.g., anti-fraud laws). |

| Errors & Omissions Insurance | Secure professional liability coverage to mitigate risks. |

Licensing and Regulatory Compliance for Sole Proprietor Insurance Businesses

Licensing varies by state but generally involves passing exams (e.g., property/casualty or life/health), submitting fingerprints, and paying fees. As a sole proprietor, you must also maintain ongoing education credits and renew licenses periodically. Regulatory compliance includes transparent client communication, ethical sales practices, and timely claim resolutions.

See Also As a Vc or Business Angel What is Your Checklist When You Invest in a Startup

As a Vc or Business Angel What is Your Checklist When You Invest in a Startup| License Type | Key Details |

| Producer License | Allows selling insurance policies; requires exam completion. |

| Surplus Lines License | Needed for high-risk policies not covered by standard insurers. |

| Adjuster License | Required to assess and settle insurance claims. |

Financial Considerations and Capital Requirements

Insurance companies must maintain minimum capital reserves to ensure solvency. As a sole proprietor, securing sufficient funds personally can be daunting. Startups often need reinsurance partnerships to offset risk exposure. Operating costs like marketing, technology systems, and staffing add further financial pressure.

| Financial Factor | Details |

| Capital Reserves | State-mandated minimums (e.g., $500,000+ for certain lines). |

| Reinsurance Costs | Fees to transfer risk to larger insurers. |

| Operational Expenses | Software, office space, and employee salaries. |

Risks and Liabilities of Operating as a Sole Proprietor in Insurance

Sole proprietors face unlimited personal liability, meaning personal assets (e.g., home, savings) can be seized to cover business losses. Insurance companies are vulnerable to catastrophic claims and fraudulent lawsuits, amplifying financial risks. Without a corporate shield, recovering from legal disputes or insolvency becomes harder.

See Also What's the Typical Route to Becoming a Vc?

What's the Typical Route to Becoming a Vc?| Risk Type | Impact |

| Legal Liability | Personal responsibility for lawsuits or regulatory penalties. |

| Financial Losses | Debts or unpaid claims affecting personal credit. |

| Reputation Damage | Client disputes harming future business prospects. |

Alternatives to Sole Proprietorship for Insurance Startups

Forming an LLC or corporation limits personal liability and enhances credibility with clients and reinsurers. Partnerships or MGA (Managing General Agent) arrangements allow sharing regulatory burdens. Some entrepreneurs begin as insurance brokers instead of underwriters to reduce capital demands.

| Alternative Structure | Benefits |

| LLC | Asset protection, tax flexibility, and easier compliance. |

| Corporation | Strong liability shield and investor appeal. |

| Brokerage Model | Lower capital needs by selling third-party policies. |

What licenses do you need to open an insurance company?

Venture Capital Investment Bootcamp Randall Reade's Posts

Venture Capital Investment Bootcamp Randall Reade's PostsState Licensing Requirements for Insurance Companies

To open an insurance company, you must obtain a state-specific license from the regulatory authority in each state where you plan to operate. Requirements vary by jurisdiction but generally include submitting financial statements, business plans, and proof of compliance with capital and surplus standards.

- Application forms detailing company structure and ownership.

- Financial audits to demonstrate solvency and reserve adequacy.

- Fees ranging from hundreds to thousands of dollars, depending on the state.

A Certificate of Authority (COA) is the primary license allowing an insurer to underwrite policies in a state. It requires approval from the state’s Department of Insurance, which evaluates the company’s financial stability and operational readiness.

- Detailed business plan outlining products and risk management strategies.

- Minimum capital and surplus requirements (e.g., $2 million to $5 million).

- Approval from the NAIC (National Association of Insurance Commissioners) for interstate operations.

Licensing for Agents and Brokers

Individuals selling insurance products on behalf of the company must hold state-issued producer licenses. These licenses ensure agents meet education, examination, and ethical standards.

- Pre-licensing education hours (e.g., 20–40 hours per line of insurance).

- State-administered exams covering laws, ethics, and product knowledge.

- Background checks to verify no history of fraud or felonies.

Reinsurance Company Licensing

Reinsurance companies, which insure other insurers, require specialized licenses to operate. These often involve enhanced financial scrutiny and adherence to international regulatory frameworks.

- Collateral requirements to protect ceding insurers.

- Approval under the NAIC’s Reinsurance Accreditation Program.

- Compliance with Solvency II (in the EU) or similar standards in other regions.

Surplus Lines Insurance Licensing

Insurers offering surplus lines coverage (high-risk or non-standard policies) need a separate license. These are regulated differently, often with fewer rate and form restrictions.

- Eligibility certification proving the insurer meets state financial requirements.

- Listing on the state’s surplus lines white list.

- Tax filings and stamping fees for policies issued.

How much capital do you need to start an insurance company?

Regulatory Capital Requirements

The minimum capital requirement to start an insurance company varies by jurisdiction and insurance type. For example:

- In the U.S., states mandate $500,000 to $3 million for property/casualty insurers, while life insurers may need $1–5 million.

- The EU’s Solvency II framework requires €2–4 million for non-life insurers and higher amounts for life insurers.

- Emerging markets like India or Nigeria often set lower thresholds ($100,000–$500,000), but require approval from regulators like IRDAI.

Type of Insurance Offered

Capital needs depend on the insurance products you plan to offer. High-risk policies require larger reserves:

- Life insurance demands higher capital due to long-term liabilities and actuarial risks.

- Health insurance may require $1–3 million to cover claims volatility.

- Property/casualty insurance often needs $500,000–$2 million, but catastrophic coverage (e.g., hurricanes) can double this.

Business Model and Operational Costs

Your business structure significantly impacts startup costs:

- A direct-to-consumer digital insurer may save on agent commissions but requires $1–2 million for tech infrastructure.

- Traditional agencies with brokers might spend $2–5 million on staffing and office space.

- Marketing and underwriting software add $200,000–$500,000 annually.

Reinsurance Considerations

Reinsurance agreements reduce risk but affect capital planning:

- Purchasing reinsurance treaties costs 10–20% of premiums, requiring upfront liquidity.

- Insurers retaining more risk must hold higher capital reserves (e.g., $3–10 million for catastrophe coverage).

- Reinsurers may demand collateral or guarantees, tying up additional funds.

Additional Financial Reserves for Solvency

Regulators require solvency margins beyond initial capital:

- Maintain a risk-based capital (RBC) ratio of 200–300% to cover unexpected claims.

- Set aside $500,000–$2 million for liquidity during economic downturns.

- Reserve 10–15% of premiums annually to meet future obligations.

Do I need an LLC as an insurance agent?

Do You Need an LLC to Operate as an Insurance Agent?

While forming an LLC (Limited Liability Company) is not legally required to work as an insurance agent, it offers significant advantages. Insurance agents face risks like lawsuits, errors, or client disputes, and an LLC provides personal asset protection by separating your business liabilities from personal finances. Additionally, it enhances professional credibility and may offer tax flexibility. However, sole proprietorships are simpler and cheaper to manage if you prefer minimal administrative work.

- Liability Protection: Shields personal assets (e.g., home, savings) from business-related lawsuits.

- Tax Flexibility: Choose between pass-through taxation or corporate tax structures.

- Credibility: An LLC often appears more professional to clients and partners.

Benefits of an LLC for Insurance Agents

An LLC provides insurance agents with structural and financial advantages. For instance, it limits your personal liability if a client sues over alleged negligence or errors. It also allows you to build business credit separately from your personal credit history. Furthermore, tax deductions for business expenses (e.g., office supplies, marketing) become more streamlined.

- Asset Protection: Legal separation between personal and business finances.

- Tax Deductions: Claim expenses like licensing fees, training, and equipment.

- Scalability: Easier to add partners or investors under an LLC structure.

Drawbacks of Not Forming an LLC as an Insurance Agent

Operating without an LLC exposes you to unlimited personal liability. For example, if a client files a lawsuit, your personal savings or property could be at risk. Sole proprietorships also lack the perceived professionalism of an LLC, which might deter potential clients or partnerships. Additionally, tax opportunities, like splitting income, are limited.

- Financial Risk: Personal assets are vulnerable to business debts or legal claims.

- Limited Tax Options: No flexibility to elect corporate taxation.

- Perception Issues: Clients may view unregistered businesses as less established.

How to Form an LLC as an Insurance Agent

Forming an LLC involves several steps, starting with registering your business name and filing Articles of Organization with your state. You’ll also need an Operating Agreement, obtain an EIN (Employer Identification Number) from the IRS, and secure necessary insurance licenses. Compliance with state-specific insurance regulations is critical.

- Choose a Name: Ensure it’s unique and complies with state rules.

- File Documentation: Submit Articles of Organization and pay fees.

- Obtain Licenses: Maintain proper insurance agent licensing alongside LLC registration.

Alternatives to an LLC for Insurance Agents

If an LLC seems too complex, consider alternatives like a sole proprietorship or S corporation. Sole proprietorships require no formal setup but lack liability protection. S corporations offer tax benefits but involve stricter compliance. Partnerships or Professional LLCs (PLLCs) may also suit multi-agent firms.

- Sole Proprietorship: Simplest structure but no liability protection.

- S Corporation: Reduces self-employment taxes but requires payroll setup.

- Professional LLC (PLLC): Ideal for licensed professionals in certain states.

Frequently Asked Questions (FAQs)

Can I Legally Start an Insurance Company as a Sole Proprietor?

Starting an insurance company as a sole proprietor is legally possible in many jurisdictions, but it is subject to strict regulatory requirements. Insurance businesses are highly regulated due to their financial and public trust implications. Sole proprietors must obtain the necessary licenses, such as a business license and an insurance producer or agency license, depending on the services offered. Additionally, compliance with state or national insurance regulations, capital requirements, and proof of financial stability are mandatory. Many jurisdictions require proof of sufficient reserves to cover potential claims, which can be challenging for a sole proprietor without significant personal assets or backing.

What Are the Risks of Running an Insurance Company as a Sole Proprietor?

Operating an insurance company as a sole proprietor exposes you to unlimited personal liability. This means your personal assets, such as savings or property, could be at risk if the business faces lawsuits or cannot cover claims. Insurance companies also require substantial capital reserves to meet regulatory standards and policyholder obligations, which can strain a sole proprietor’s finances. Furthermore, the lack of structural separation between personal and business assets may deter clients or partners who prefer working with legally protected entities like corporations or LLCs.

Are There Alternatives to a Sole Proprietorship for Starting an Insurance Company?

Yes, forming a corporation or limited liability company (LLC) is often recommended for insurance ventures. These structures provide liability protection, separating personal assets from business debts or legal claims. They also enhance credibility with clients and regulators. Some jurisdictions may even require insurance companies to operate as corporations due to regulatory mandates. While a sole proprietorship offers simplicity, the complexity and risks of the insurance industry typically necessitate a more formal business structure.

What Licenses and Certifications Are Required to Start an Insurance Company as a Sole Proprietor?

To legally operate an insurance company as a sole proprietor, you must obtain a business license and specific insurance-related licenses. These often include an insurance producer license or agency license, which may require passing exams and completing pre-licensing education. Additionally, you may need certifications for specialized insurance products, such as life, health, or property insurance. Compliance with state or national regulatory bodies, such as the National Association of Insurance Commissioners (NAIC) in the U.S., is critical. Regular audits and financial reporting are also typically mandated to maintain licensure.

Leave a Reply

Our Recommended Articles