Business Insurance for Candle Makers

Candle making, a craft blending artistry and entrepreneurship, has seen a surge in popularity as consumers seek handmade, eco-friendly products. However, turning this passion into a sustainable business requires more than creativity—it demands careful risk management. From fire hazards in production to liability claims from product use, candle makers face unique challenges that can threaten their operations. Business insurance tailored to this niche industry provides essential protection against unforeseen setbacks, covering risks like property damage, legal disputes, or supply chain disruptions. Whether you operate from a small studio or sell online, understanding the right coverage options ensures your enterprise can thrive while safeguarding your craft, assets, and peace of mind.

- Understanding Business Insurance Needs for Candle Makers

- What insurance do you need for a candle business?

-

What insurance do you need for candle-making?

- What Types of Insurance Are Essential for Candle-Making?

- Why Do Candle Makers Need Product Liability Insurance?

- How Does General Liability Insurance Protect Candle Businesses?

- What Does Commercial Property Insurance Cover for Candle Makers?

- Is Business Interruption Insurance Necessary for Candle-Making?

- Should Candle Makers Consider Workers’ Compensation Insurance?

- Do I need insurance to make and sell candles?

-

How much is

- Frequently Asked Questions (FAQs)

Understanding Business Insurance Needs for Candle Makers

Why General Liability Insurance is Essential for Candle Makers

Candle makers face risks such as third-party injuries (e.g., burns from hot wax) or property damage caused by accidental fires. General liability insurance covers legal fees, medical expenses, and settlements if your business is held responsible. For example, if a customer slips in your store or a defective candle damages a client’s property, this policy protects your financial stability.

See AlsoDog Walking Business Insurance| Coverage | Details |

|---|---|

| Bodily Injury | Covers medical costs if a customer is injured. |

| Property Damage | Pays for repairs to third-party property. |

| Legal Defense | Includes attorney fees and court costs. |

Candles inherently carry risks like fire hazards or allergic reactions to fragrances. Product liability insurance shields your business if a candle causes harm. For instance, if a candle’s design flaw leads to a house fire, this policy covers lawsuits, recalls, or settlements.

| Risk | Coverage Scope |

|---|---|

| Defective Products | Claims due to manufacturing errors. |

| Mislabeling | Inaccurate safety warnings or ingredients. |

| Design Flaws | Inherent dangers in the candle’s structure. |

Protecting Your Workspace with Property Insurance

Candle-making requires equipment like wax melters, fragrance mixers, and inventory. Property insurance covers damage to your workspace, tools, or stock from fire, theft, or natural disasters. Without it, replacing a destroyed workshop could bankrupt your business.

See AlsoAuto Detailing Business Insurance| Asset | Covered Perils |

|---|---|

| Equipment | Fire, vandalism, burst pipes. |

| Inventory | Theft, smoke damage. |

| Building | Storms, explosions. |

Business Interruption Insurance for Unexpected Closures

If a disaster forces temporary closure (e.g., a fire), business interruption insurance compensates for lost income and ongoing expenses (rent, salaries). This ensures you can recover without draining savings.

| Component | Details |

|---|---|

| Lost Revenue | Based on average past earnings. |

| Operating Costs | Rent, utilities, payroll. |

| Recovery Period | Typically 3–12 months. |

Comparing Insurance Policies for Candle Businesses

Evaluate policies based on coverage limits, exclusions, and premium costs. For example, a home-based candle maker might prioritize product liability, while a large workshop needs property insurance.

See AlsoIs It Illegal to Not Have Business Insurance?| Policy Type | Best For | Average Cost/Year |

|---|---|---|

| General Liability | All businesses | $400–$1,000 |

| Product Liability | Candle-specific risks | $600–$1,200 |

| Business Owner’s Policy (BOP) | Combined coverage | $800–$2,500 |

What insurance do you need for a candle business?

General Liability Insurance for Candle Businesses

A candle business should prioritize general liability insurance to protect against third-party claims. This coverage addresses bodily injury, property damage, or advertising injuries that could arise during operations. For example, a customer slipping in your store or a vendor’s equipment being damaged during a delivery.

See AlsoRv Storage Business Insurance Cost- Bodily injury claims: Covers medical costs if someone is hurt at your workspace.

- Property damage: Protects against costs if your business damages a client’s property.

- Legal defense fees: Helps pay for lawsuits, even if claims are unfounded.

Product Liability Insurance for Candle Makers

Product liability insurance is critical for candle businesses due to risks like fires or allergic reactions caused by candles. It covers claims related to product defects, improper labeling, or safety hazards.

- Defective product claims: Addresses lawsuits if a candle malfunctions (e.g., causing a fire).

- Allergic reactions: Covers incidents from fragrances or materials.

- Labeling errors: Protects against fines or lawsuits due to missing safety warnings.

Commercial Property Insurance for Candle Workshops

Commercial property insurance safeguards your physical assets, such as workshops, equipment, and inventory, from risks like fire, theft, or natural disasters.

See AlsoWhat is a Reasonable Hourly Rate to Charge for a Contract Business Analyst?- Building coverage: Repairs or replaces your workspace if damaged.

- Equipment protection: Covers machinery, molds, or melting tools.

- Inventory loss: Compensates for destroyed raw materials or finished candles.

Business Interruption Insurance for Candle Companies

Business interruption insurance helps recover lost income if operations halt due to covered events (e.g., fire or flood). This is vital for maintaining cash flow during downtime.

- Lost revenue: Replaces income during closure periods.

- Ongoing expenses: Covers rent, utilities, or payroll while rebuilding.

- Relocation costs: Funds temporary workspace if needed.

Workers’ Compensation Insurance for Candle Manufacturing

If you have employees, workers’ compensation insurance is legally required in most states. It covers medical bills and lost wages if an employee is injured while making or handling candles.

- Workplace injuries: Addresses burns, chemical exposure, or repetitive strain injuries.

- Disability benefits: Provides partial income for employees unable to work.

- Legal compliance: Avoids fines for lacking mandatory coverage.

What insurance do you need for candle-making?

What Types of Insurance Are Essential for Candle-Making?

Candle-making involves risks like fire hazards, product liability, and property damage. Essential insurance policies protect against financial losses from accidents, lawsuits, or operational disruptions. Key policies include:

- Product Liability Insurance: Covers claims if a candle causes injury or property damage.

- General Liability Insurance: Protects against third-party bodily injury or property damage claims at your workspace.

- Commercial Property Insurance: Safeguards equipment, inventory, and workspace from fire, theft, or natural disasters.

Why Do Candle Makers Need Product Liability Insurance?

Product liability insurance is critical because candles pose risks like fires, allergic reactions, or defective products. If a customer sues due to harm caused by your candles, this policy covers legal fees and settlements.

- Covers claims related to flammability issues or improper labeling.

- Protects against lawsuits from allergic reactions to fragrances or materials.

- Includes coverage for recall costs if a product batch is faulty.

How Does General Liability Insurance Protect Candle Businesses?

General liability insurance addresses risks unrelated to the product itself, such as accidents in your workspace. For example, a client slipping during a workshop or a delivery person injured on your premises.

- Coverage for third-party injuries or property damage.

- Legal defense costs for non-product-related claims.

- Protection against advertising injuries, like copyright infringement accusations.

What Does Commercial Property Insurance Cover for Candle Makers?

Commercial property insurance protects physical assets like equipment, raw materials, and inventory. This is vital for recovering from incidents like fires, which are a heightened risk in candle production.

- Replaces damaged equipment (e.g., melters, molds).

- Covers loss of inventory due to fire, theft, or water damage.

- Includes business interruption coverage for temporary closures.

Is Business Interruption Insurance Necessary for Candle-Making?

Business interruption insurance compensates for lost income if operations halt due to covered events (e.g., fire or natural disasters). For candle makers, this ensures financial stability during repairs or rebuilding.

- Replaces lost revenue during downtime.

- Covers ongoing expenses like rent or employee wages.

- Helps fund temporary relocation costs if needed.

Should Candle Makers Consider Workers’ Compensation Insurance?

If you have employees, workers’ compensation insurance is often legally required. It covers medical expenses and lost wages if an employee is injured while making candles or handling materials.

- Mandatory in most states for businesses with employees.

- Covers injuries from burns, chemical exposure, or repetitive strain.

- Protects against employee lawsuits over workplace injuries.

Do I need insurance to make and sell candles?

Is Insurance Legally Required for Making and Selling Candles?

While insurance is not universally mandated by law for small candle-making businesses, certain circumstances may require it. For example, if you hire employees, workers’ compensation insurance is often legally required. Additionally, selling at craft fairs or markets might require proof of liability insurance as part of vendor agreements. Always check local regulations and contractual obligations to ensure compliance.

- Local laws: Some jurisdictions may require specific business insurance.

- Vendor agreements: Event organizers often mandate liability coverage.

- Employees: Workers’ compensation is legally required in most regions if you have staff.

What Types of Insurance Are Relevant for Candle Businesses?

Candle makers should consider general liability insurance, product liability insurance, and home-based business insurance (if operating from home). General liability covers accidents (e.g., a customer slipping at your stall), while product liability protects against claims related to candle defects (e.g., fires or allergic reactions).

- General liability: Covers third-party injuries or property damage.

- Product liability: Addresses risks tied to product safety.

- Home-based policies: Standard homeowners’ insurance may exclude business activities.

What Risks Exist Without Insurance for Candle Sellers?

Operating without insurance exposes you to financial liability from lawsuits, recalls, or accidents. For instance, if a candle causes a fire, you could face costly legal fees or compensation claims. Even minor incidents, like allergic reactions to fragrances, might lead to disputes.

- Lawsuits: Legal defense costs can bankrupt small businesses.

- Product recalls: Expenses for retrieving defective products.

- Reputation damage: Uninsured incidents may harm customer trust.

Does Selling Online Affect Insurance Needs?

Selling candles online may increase risks, such as shipping damages or international liability. Platforms like Etsy or Amazon may not require insurance, but third-party claims (e.g., a customer injured by a melted candle) still pose risks. Consider e-commerce insurance or cyber liability coverage for online transactions.

- Shipping risks: Damaged goods could lead to refunds or claims.

- Platform requirements: Some marketplaces recommend vendor insurance.

- Cyber risks: Protect customer data with cyber liability coverage.

How to Choose the Right Insurance for a Candle Business?

Assess your business scale, sales channels, and risk exposure. Work with an insurance agent specializing in small businesses to customize coverage. Compare policies for premium costs, coverage limits, and exclusions (e.g., certain fragrance ingredients).

- Risk assessment: Identify high-risk areas (e.g., candle materials).

- Agent consultation: Tailor policies to your business model.

- Policy comparison: Balance affordability and comprehensive coverage.

How much is $1,000,000 liability insurance a month?

The monthly cost of a $1,000,000 liability insurance policy varies widely based on factors like industry type, business size, location, and risk exposure. On average, small businesses may pay between $300 to $600 per month, while high-risk industries (e.g., construction) could see premiums exceeding $1,000 monthly. Insurers also consider claims history, revenue, and deductible choices when determining rates.

Factors Influencing the Cost of $1,000,000 Liability Insurance

Several variables directly impact the monthly premium for a $1,000,000 liability insurance policy. Key factors include:

- Industry risk level: High-risk sectors (e.g., manufacturing) face higher premiums.

- Business location: States with higher litigation rates or regulatory costs may increase prices.

- Claims history: A track record of frequent claims can raise monthly costs significantly.

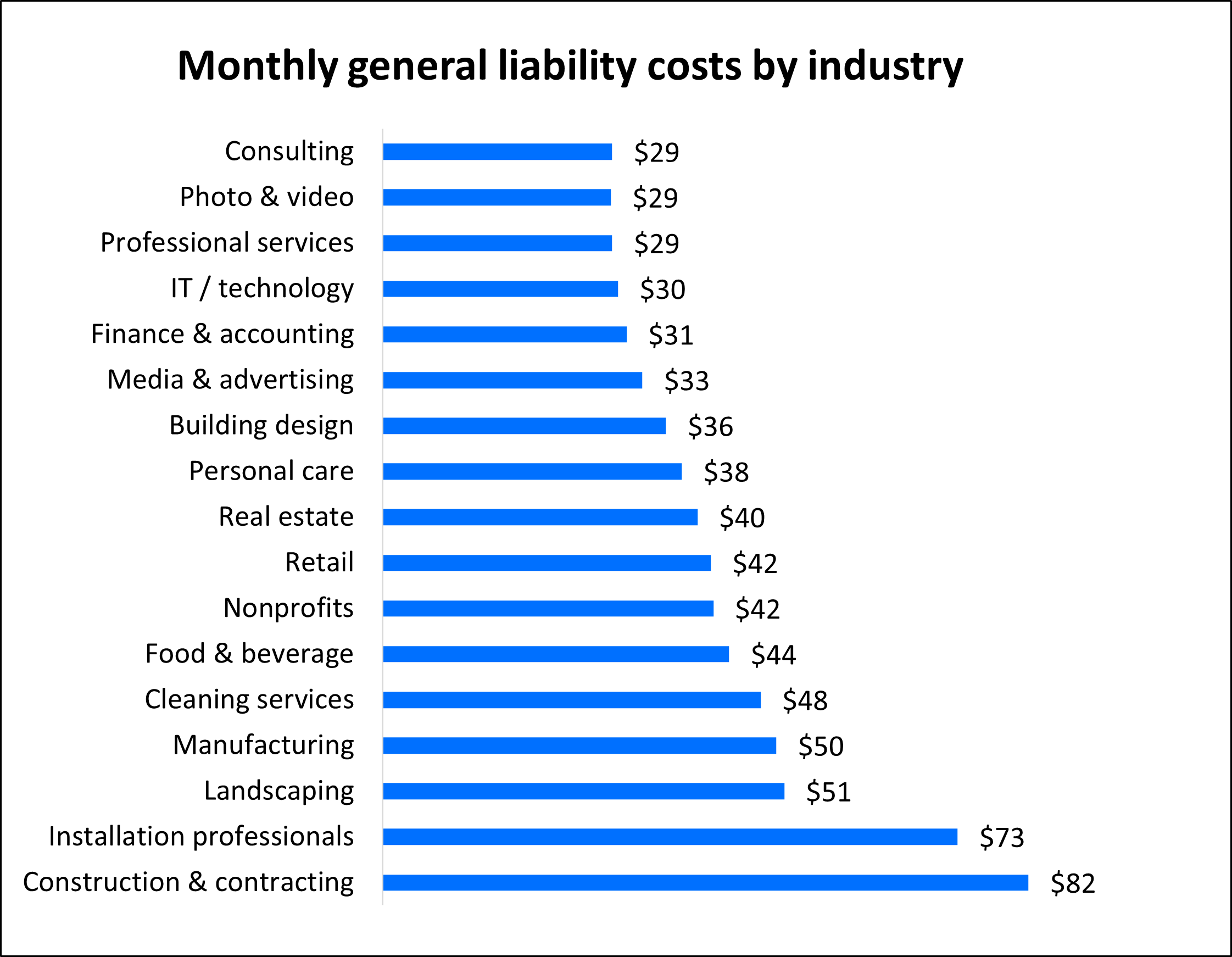

Monthly premiums for $1,000,000 liability coverage differ across industries. Examples include:

- Retail: $250–$500/month due to moderate risk exposure.

- Construction: $800–$1,500/month because of elevated workplace hazards.

- Consulting: $150–$300/month for lower physical risk.

How to Lower Your Liability Insurance Costs

Businesses can reduce monthly premiums for $1 million liability insurance by:

- Bundling policies: Combine liability with property insurance for discounts.

- Increasing deductibles: Higher deductibles often lower monthly payments.

- Implementing safety protocols: Demonstrating risk mitigation can qualify for reduced rates.

State-by-State Variations in Liability Insurance Rates

Geographic location heavily influences monthly liability insurance costs. For example:

- California: $400–$800/month due to strict regulations and litigation trends.

- Texas: $350–$700/month, influenced by industry-heavy economies.

- Florida: $500–$1,000/month because of hurricane-related risks.

Comparing Insurance Providers for Affordable Rates

To find competitive pricing for $1M liability coverage, consider:

- Online quotes: Compare rates from multiple insurers instantly.

- Specialized carriers: Providers focusing on your industry may offer better deals.

- Customer reviews: Prioritize insurers with strong financial stability and claims support.

Frequently Asked Questions (FAQs)

What types of insurance do candle makers need?

Business insurance for candle makers typically includes several key policies to address industry-specific risks. General liability insurance protects against third-party claims for bodily injury or property damage, such as a customer slipping in your store. Product liability insurance is critical, as it covers claims arising from defective candles causing harm, like fires or allergic reactions. Additionally, commercial property insurance safeguards your workspace, equipment, and inventory from events like fires or theft. If you operate from home, a home-based business endorsement might be necessary, as standard homeowner’s policies rarely cover business activities.

Why is product liability insurance important for candle makers?

Candle makers face unique risks due to the flammable nature of their products and potential allergens in fragrances or materials. Product liability insurance is essential to cover legal fees, medical costs, or settlements if a candle causes property damage, injuries, or health issues. For example, if a candle overheats and starts a fire, this policy can protect your business from devastating financial losses. Without it, you might personally shoulder costs that could bankrupt your business, especially in litigious environments.

Does home-based candle making require business insurance?

Even if you operate a small-scale candle business from home, insurance is still vital. Standard homeowner’s or renter’s insurance policies often exclude business-related claims, leaving you vulnerable. A home-based business endorsement or a standalone business owner’s policy (BOP) can fill this gap. These policies cover liabilities like a customer injured by a candle or damage to your inventory from a covered peril. Ignoring this coverage could result in denied claims or out-of-pocket expenses for incidents tied to your business activities.

How can candle makers choose the right insurance provider?

Selecting an insurance provider requires evaluating their experience with small businesses and familiarity with the craft and candle-making industry. Look for insurers offering tailored policies that address risks like product liability, fire damage, or supply chain disruptions. Compare quotes to balance cost-effectiveness with comprehensive coverage. Check reviews and ask about claims responsiveness, as delays can cripple a small business. Finally, consult an insurance agent specializing in artisan or handmade goods to ensure no critical exposures are overlooked.

Leave a Reply

Our Recommended Articles