Auto Detailing Business Insurance

Operating an auto detailing business involves more than just delivering exceptional service—it requires safeguarding against unforeseen risks. From accidental damage to client vehicles to potential liability claims, the industry’s unique challenges demand comprehensive insurance coverage. Whether you’re a mobile detailer or operate from a fixed location, having the right policies—such as general liability, commercial auto, workers’ compensation, or equipment protection—can shield your business from financial setbacks. This article explores essential insurance options for auto detailing professionals, helping you navigate coverage choices to ensure legal compliance, protect assets, and maintain peace of mind. Understanding these protections is critical to mitigating risks and securing your business’s long-term stability in a competitive market.

- Why Auto Detailing Business Insurance is Essential for Your Success

- What kind of insurance do I need for a detailing business?

- Do you need an LLC to start a car detailing business?

- How much does a cleaning business insurance cost?

- What business category is car detailing?

- Frequently Asked Questions (FAQs)

Why Auto Detailing Business Insurance is Essential for Your Success

Auto detailing business insurance protects your company from financial losses due to accidents, lawsuits, or property damage. Without proper coverage, unexpected events like customer vehicle damage, employee injuries, or theft of equipment could jeopardize your operations. Insurance ensures legal compliance, client trust, and financial stability, allowing you to focus on delivering quality services while mitigating risks inherent in the automotive care industry.

See AlsoComputer Repair Business InsuranceCommon Risks Faced by Auto Detailing Businesses

Auto detailing businesses encounter unique risks, including chemical spills, equipment malfunctions, and accidental damage to clients’ vehicles. For example, a scratched paint job during polishing could lead to costly repairs and legal disputes. Additionally, employees handling heavy machinery or hazardous substances face injury risks, potentially resulting in workers’ compensation claims.

| Risk | Description |

|---|---|

| Property Damage | Accidental harm to client vehicles or third-party property. |

| Theft | Loss of tools, detailing supplies, or customer belongings. |

| Bodily Injury | Injuries to employees or customers on your premises. |

Types of Insurance Coverage for Auto Detailing Businesses

Key insurance policies include General Liability Insurance, Commercial Auto Insurance, and Tools & Equipment Coverage. General Liability protects against third-party injury or property damage claims, while Commercial Auto Insurance covers company vehicles used for mobile detailing. Tools & Equipment Coverage safeguards against theft or damage to specialized tools like buffers or pressure washers.

See AlsoDump Trailer Rental Business Insurance| Coverage Type | Purpose |

|---|---|

| General Liability | Covers legal fees and settlements for third-party claims. |

| Commercial Property | Protects physical assets like your shop or storage unit. |

| Workers' Compensation | Supports employees injured on the job. |

Factors Influencing Insurance Costs

Insurance premiums depend on factors like business size, location, and coverage limits. A larger operation with multiple employees and high-value equipment typically pays more. Geographic risks, such as operating in areas prone to theft or natural disasters, also increase costs. Maintaining a clean claims history and implementing safety protocols can reduce premiums.

| Factor | Impact on Cost |

|---|---|

| Revenue | Higher revenue often correlates with higher premiums. |

| Deductibles | Choosing a higher deductible lowers monthly payments. |

| Services Offered | Specialized services (e.g., ceramic coating) may raise costs. |

How to Choose the Right Insurance Policy

Evaluate policies based on coverage scope, exclusions, and insurer reputation. Partner with providers experienced in the auto detailing industry, as they understand sector-specific risks. Compare quotes to balance affordability with adequate protection, and ensure policies cover mobile operations if applicable.

See AlsoVending Machine Business Insurance| Step | Action |

|---|---|

| Assess Risks | Identify vulnerabilities like equipment theft or customer lawsuits. |

| Review Policies | Verify inclusions like product liability or cyber insurance. |

| Consult an Agent | Seek tailored advice for your business model. |

Understanding Claims and Deductibles

A deductible is the amount you pay out-of-pocket before insurance covers a claim. For example, a $1,000 deductible means you pay the first $1,000 of a covered loss. Familiarize yourself with the claims process, including documentation requirements like photos of damage or incident reports, to ensure timely resolution.

| Term | Definition |

|---|---|

| Claim | A formal request for coverage after a loss. |

| Premium | Regular payment to maintain insurance coverage. |

| Policy Limit | Maximum amount an insurer will pay per claim. |

What kind of insurance do I need for a detailing business?

Essential Insurance Types for a Detailing Business

Operating a detailing business requires protection against common risks. The most critical policies include General Liability Insurance, Commercial Auto Insurance, and Workers’ Compensation. These policies safeguard your business from third-party claims, vehicle-related incidents, and employee injuries.

- General Liability Insurance: Covers property damage or bodily injury claims from clients.

- Commercial Auto Insurance: Protects company vehicles used for mobile detailing services.

- Workers’ Compensation: Mandatory if you have employees, covering workplace injury costs.

Why General Liability Insurance Is Crucial

General Liability Insurance is foundational for any detailing business. It addresses claims arising from accidents during operations, such as accidentally scratching a client’s car or water damage to their property.

- Covers legal fees and settlements in lawsuits.

- Protects against claims of property damage or bodily injury.

- Often required by clients or leasing companies.

Commercial Auto Insurance for Mobile Detailing

If your business involves traveling to clients, Commercial Auto Insurance is non-negotiable. Personal auto policies typically exclude business-related accidents.

- Covers collisions, theft, or damage to your work vehicles.

- Includes liability coverage for accidents caused by employees.

- May cover tools and equipment inside the vehicle.

Protecting Equipment with Inland Marine Insurance

Detailing relies on expensive tools like pressure washers and polishers. Inland Marine Insurance covers equipment that’s transported or used off-site.

- Replaces or repairs stolen or damaged tools.

- Covers equipment during transit or at client locations.

- Often excluded from standard property policies.

Workers’ Compensation and Employee Safety

If you hire staff, Workers’ Compensation Insurance is legally required in most states. It covers medical bills and lost wages if an employee is injured.

- Shields your business from employee lawsuits.

- Ensures compliance with state regulations.

- Covers repetitive stress injuries or chemical exposure.

Business Owner’s Policy (BOP) for Comprehensive Coverage

A Business Owner’s Policy bundles General Liability and Commercial Property Insurance, offering cost-effective protection for small detailing businesses.

- Combines property damage and liability coverage.

- May include business interruption insurance.

- Customizable with add-ons like equipment coverage.

Do you need an LLC to start a car detailing business?

Legal Requirements for Starting a Car Detailing Business

To start a car detailing business, you do not legally need an LLC. Most jurisdictions allow you to operate as a sole proprietorship or partnership without forming a formal business entity. However, you must comply with basic legal requirements:

- Obtain a business license or permit from your local government.

- Register your business name (if using a DBA, “Doing Business As”).

- Secure insurance, such as general liability or auto liability coverage.

Benefits of Forming an LLC for a Car Detailing Business

While not mandatory, forming an LLC offers advantages like personal liability protection and enhanced credibility. Key benefits include:

- Asset protection: Separates personal assets from business debts or lawsuits.

- Tax flexibility: Choose to be taxed as a sole proprietorship, partnership, or corporation.

- Professional image: An LLC may attract more clients or partnerships compared to unregistered businesses.

Liability Risks Without an LLC

Operating without an LLC exposes you to personal financial risks. For example:

- Lawsuits: Clients could sue you personally for damages or injuries related to your services.

- Debt liability: Business debts, like equipment loans, may impact your personal credit.

- Contract disputes: Unresolved vendor or client issues could lead to personal financial obligations.

Tax Implications for LLCs vs. Sole Proprietorships

Tax structures differ between LLCs and sole proprietorships:

- Pass-through taxation: Both entities typically report income on personal tax returns, but LLCs can opt for corporate taxation.

- Self-employment taxes: Sole proprietors pay self-employment tax on all profits, while LLC members may have more flexibility.

- Deductions: LLCs often qualify for more business expense deductions, reducing taxable income.

Steps to Form an LLC for a Car Detailing Business

If you choose to form an LLC, follow these steps:

- Choose a business name and ensure it’s available in your state.

- File Articles of Organization with your state’s business division, paying required fees.

- Create an Operating Agreement outlining ownership and management rules (not mandatory in all states).

- Obtain an EIN (Employer Identification Number) from the IRS for tax purposes.

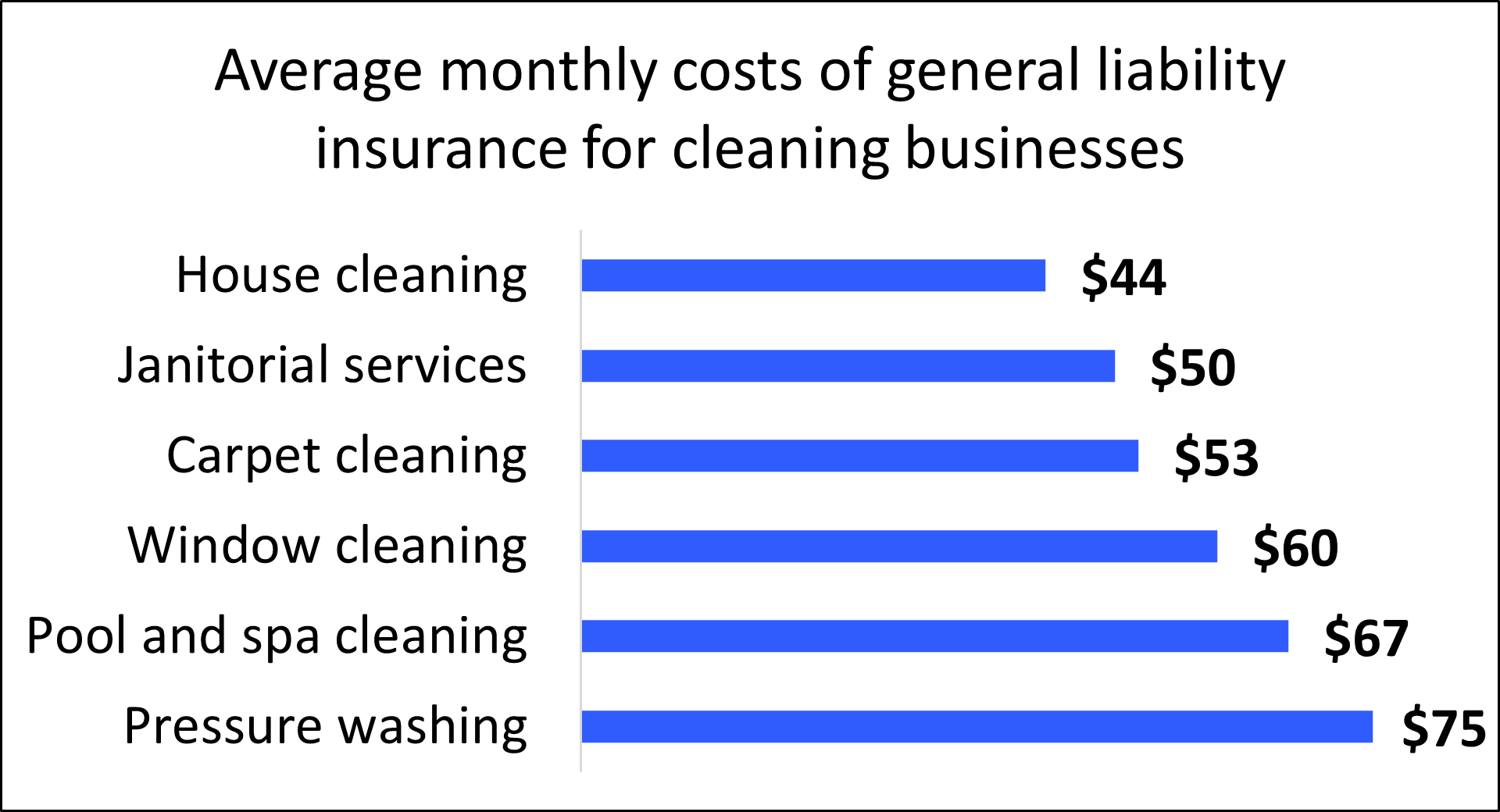

How much does a cleaning business insurance cost?

What Factors Influence the Cost of Cleaning Business Insurance?

The cost of cleaning business insurance depends on variables like business size, services offered, number of employees, and coverage limits. For example, a solo operator offering residential cleaning may pay less than a company with employees handling hazardous materials.

- Business size: Larger teams often require higher liability coverage.

- Service type: High-risk services (e.g., biohazard cleanup) increase premiums.

- Location: States with higher litigation rates may raise costs.

Average Costs for Common Cleaning Business Insurance Policies

Typical insurance costs for cleaning businesses range from $400 to $3,000+ annually, depending on policy types. Basic general liability insurance often starts at $400–$800/year, while bundled policies cost more.

- General Liability: $400–$1,000/year.

- Workers’ Compensation: $500–$2,500/year (based on payroll).

- Commercial Auto Insurance: $750–$1,200/year per vehicle.

Smaller cleaning businesses with fewer employees typically pay lower premiums. For example, a solo operator might spend $500–$800/year, while a 10-employee company could pay $2,000–$4,000 due to added risks.

- Sole proprietors: Lower premiums due to minimal liability exposure.

- Mid-sized teams: Higher costs for workers’ compensation and liability.

- Large companies: Require umbrella policies, increasing expenses.

State-Specific Variations in Cleaning Insurance Costs

Insurance costs vary by state regulations, local risk factors, and claim frequency. For instance, California and Florida often have higher premiums due to strict liability laws or natural disaster risks.

- High-cost states: NY, CA, FL (due to litigation rates).

- Low-cost states: Midwest regions (lower risk perception).

- State mandates: Workers’ comp requirements impact pricing.

Ways to Reduce Cleaning Business Insurance Expenses

Lowering insurance costs is achievable through bundling policies, maintaining safety protocols, and adjusting deductibles. Comparing quotes from multiple providers also helps secure competitive rates.

- Policy bundling: Save 10–20% with a Business Owner’s Policy (BOP).

- Safety training: Reduces workers’ comp claims.

- Higher deductibles: Lowers annual premiums (if cash flow allows).

What business category is car detailing?

Car detailing falls under the automotive services industry, specifically within the vehicle maintenance and cleaning subcategory. It combines elements of cosmetic care, restoration, and preservation for automobiles, operating at the intersection of professional cleaning services and automotive aftermarket solutions.

1. Automotive Maintenance and Care Services

Car detailing is a specialized branch of automotive maintenance, focusing on enhancing a vehicle’s appearance and longevity. It goes beyond basic washing to address paint protection, interior sanitation, and surface restoration. Key aspects include:

- Exterior detailing: Polishing, waxing, and paint correction to combat environmental damage.

- Interior detailing: Deep cleaning of upholstery, carpets, and dashboard components.

- Protective treatments: Application of ceramic coatings or sealants to shield surfaces.

2. Niche Cosmetic Automotive Services

This category emphasizes aesthetic enhancements rather than mechanical repairs. Car detailing businesses cater to owners seeking premium visual upkeep for their vehicles. Common offerings include:

- Paint correction: Removing swirl marks and scratches for a flawless finish.

- Leather conditioning: Preserving and restoring high-end interior materials.

- Headlight restoration: Improving visibility and appearance through lens polishing.

3. Professional Cleaning and Sanitation Industry

Car detailing overlaps with commercial cleaning services, but with a focus on automotive environments. It addresses hygiene concerns and allergen removal, particularly for shared or heavily used vehicles. Core features include:

- Steam cleaning: Eliminating bacteria from seats and air vents.

- Odor neutralization: Using specialized products to remove persistent smells.

- Disinfection protocols: Meeting health standards for rideshare or fleet vehicles.

4. Automotive Retail and Aftermarket Products

Many detailing businesses operate within the automotive retail space, selling products like waxes, microfiber towels, and cleaning kits. This dual role as service provider and retailer includes:

- Product recommendations: Advising clients on maintenance tools.

- Brand partnerships: Stocking professional-grade chemicals and equipment.

- Accessory sales: Offering seat covers or floor mats alongside services.

5. Small Business and Entrepreneurial Ventures

Car detailing often falls under small business ownership, with low startup costs and flexible operational models. It appeals to entrepreneurs due to:

- Mobile detailing options: Reducing overhead with on-location services.

- Scalable services: Offering basic washes to full concours-level packages.

- Local market focus: Building clientele through community engagement and repeat customers.

Frequently Asked Questions (FAQs)

What Types of Insurance Do Auto Detailing Businesses Need?

Auto detailing businesses typically require a combination of insurance policies to address industry-specific risks. General liability insurance is essential to cover third-party injuries, property damage, or advertising-related claims. Commercial property insurance protects your equipment, supplies, and workspace from perils like fire, theft, or vandalism. Additionally, garagekeepers liability insurance is critical for businesses that temporarily hold customers’ vehicles, as it covers damage to cars under your care. If you have employees, workers’ compensation insurance is often legally mandated to cover workplace injuries.

Does General Liability Insurance Cover Damage to a Customer’s Vehicle?

While general liability insurance covers third-party bodily injuries or property damage caused by your operations, it does not typically cover damage to vehicles directly under your care. For example, if a customer slips and falls in your shop, general liability would apply. However, accidental scratches, dents, or chemical damage to a vehicle during detailing require garagekeepers liability insurance. This specialized policy fills the gap, ensuring you’re protected against claims arising from damage to customers’ cars.

Is Insurance Required for a Home-Based Auto Detailing Business?

Even home-based auto detailing businesses need insurance. Standard homeowners’ insurance policies rarely cover commercial activities, leaving you exposed to risks like customer injuries or equipment theft. General liability insurance is a must to address third-party claims, while commercial property insurance can safeguard business-owned tools and supplies. If you store clients’ vehicles on your property, garagekeepers liability insurance becomes crucial. Always check local regulations, as some states or lenders may require specific coverage for licensure or leases.

How Much Does Auto Detailing Business Insurance Cost?

The cost of insurance varies based on factors like your business size, location, coverage limits, and claims history. On average, general liability insurance may cost $500–$1,500 annually, while garagekeepers liability insurance can range from $800–$2,500 per year. Bundling policies like a business owner’s policy (BOP) often reduces costs. High-risk factors, such as storing expensive vehicles or operating in a high-crime area, may increase premiums. Work with an insurer experienced in auto detailing risks to tailor coverage and avoid overpaying.

Leave a Reply

Our Recommended Articles