Can You Get Business Insurance Without a Business License

Starting a business involves numerous legal and financial considerations, and securing insurance is often a top priority. However, a common question arises: Can you obtain business insurance without holding a formal business license? The answer depends on factors like your location, industry, and insurer requirements. While many providers mandate a license as proof of legitimate operations, some may offer coverage to unlicensed businesses, particularly freelancers, startups, or home-based ventures. This article explores the nuances of acquiring business insurance without a license, potential limitations, and alternative solutions for entrepreneurs navigating this gray area. Understanding these dynamics is crucial for protecting your enterprise while complying with local regulations.

- Can You Obtain Business Insurance Without a Business License?

-

Can you get business insurance without a business?

- Can You Get Business Insurance If You Don’t Have a Formal Business?

- Does a Side Hustle or Part-Time Venture Qualify for Business Insurance?

- What Insurance Options Exist for Freelancers or Independent Contractors?

- Can You Insure a Business Idea or Unlaunched Venture?

- Is Business Insurance Required for Informal or Cash-Based Operations?

- Do you need a business license to be insured?

- What do I need for small business insurance?

- Should I insure myself or my LLC?

- Frequently Asked Questions (FAQs)

Can You Obtain Business Insurance Without a Business License?

Understanding the Relationship Between Business Licenses and Insurance

While a business license and business insurance serve different purposes, insurers often require proof of legal operation. However, certain policies, like general liability insurance or professional liability insurance, may be available without a license, depending on the insurer and business type. For example, freelancers or sole proprietors might secure coverage even if their local jurisdiction doesn’t mandate a license.

See Also Venture Capital Investment Bootcamp Randall Reade's Posts

Venture Capital Investment Bootcamp Randall Reade's Posts| Key Factors | Details |

| Business Type | Freelancers, consultants, or home-based businesses may not need licenses. |

| State Laws | Licensing requirements vary by state and industry. |

| Insurer Policies | Some insurers may ask for a license, while others focus on risk assessment. |

Types of Business Insurance That May Not Require a License

Certain insurance policies are more accessible without a business license. General liability insurance protects against third-party claims, while professional liability insurance covers errors in services. Business owner’s policies (BOPs) or home-based business insurance might also be options for unlicensed small operations.

| Insurance Type | Coverage Scope |

| General Liability | Bodily injury, property damage, advertising injury. |

| Professional Liability | Negligence, misrepresentation, or inaccurate advice. |

| Business Property | Equipment, inventory, or workspace damage. |

State-Specific Requirements for Business Licenses and Insurance

State laws heavily influence licensing and insurance needs. For instance, California requires licenses for most businesses, while Texas has fewer restrictions. In states with lenient licensing rules, insurers may prioritize business activity validation over formal licenses. Always check local regulations before applying.

See Also Is 50 Million Enough Money to Start a Vc Firm and Become a Billionaire

Is 50 Million Enough Money to Start a Vc Firm and Become a Billionaire| State | License Requirement |

| California | Most businesses need a license. |

| Florida | Varies by county and industry. |

| Wyoming | No state-level license for sole proprietors. |

Risks of Operating Without a Business License

Operating unlicensed can lead to legal penalties, fines, or voided insurance claims. Even if you secure insurance, insurers may deny claims if your business is deemed illegal. For example, a contractor without a license might face claim rejections for workplace accidents.

| Risk | Impact |

| Legal Penalties | Fines or business shutdowns. |

| Claim Denials | Insurers may reject claims tied to unlicensed operations. |

| Reputation Damage | Clients may avoid unlicensed businesses. |

Steps to Secure Business Insurance Without a License

1. Research state and local licensing laws to confirm exemptions.

2. Identify insurers specializing in high-risk or unlicensed businesses.

3. Provide alternative documentation, like an Employer Identification Number (EIN) or business plan.

4. Consider short-term policies while working toward licensure.

What Are Some Good Questions That a Founder Should Ask a Vc Firm or an Angel Investor

What Are Some Good Questions That a Founder Should Ask a Vc Firm or an Angel Investor| Step | Action |

| Documentation | Use tax IDs, contracts, or client agreements as proof of operations. |

| Broker Assistance | Work with brokers familiar with niche insurance markets. |

Can you get business insurance without a business?

Can You Get Business Insurance If You Don’t Have a Formal Business?

Yes, you can obtain business insurance even without a formal business structure. Many providers offer coverage for freelancers, independent contractors, or sole proprietors who operate under their personal name. This is common for individuals providing services or selling goods informally. Key options include:

See AlsoHow Can One Start a Venture With No Money?- General liability insurance: Protects against third-party claims like bodily injury or property damage.

- Professional liability insurance: Covers errors or negligence in services provided.

- Business property insurance: Safeguards equipment or tools used for work, even if operated from home.

Does a Side Hustle or Part-Time Venture Qualify for Business Insurance?

Even side hustles or part-time ventures may qualify for business insurance. Insurers often evaluate the level of risk and revenue generated rather than business formalization. Examples include:

- Business owner’s policy (BOP): Combines liability and property coverage for small-scale operations.

- Inland marine insurance: Covers movable assets used for gig work, like photography gear.

- Cyber liability insurance: Protects against data breaches if handling client information online.

What Insurance Options Exist for Freelancers or Independent Contractors?

Freelancers and independent contractors often require tailored policies to mitigate risks. Common solutions include:

See AlsoIf Money is a Root of Evil, Then What is Poverty?- Professional liability (E&O) insurance: Addresses client disputes over work quality or missed deadlines.

- Commercial auto insurance: Necessary if using a vehicle for business deliveries or services.

- Workers’ compensation: Required if hiring subcontractors, even temporarily.

Can You Insure a Business Idea or Unlaunched Venture?

While unlaunched ventures typically don’t qualify for standard policies, certain protections apply during the planning phase:

- Product liability insurance: Covers prototypes or samples tested before market launch.

- Event insurance: Protects pop-up events or trade shows used to promote the idea.

- Professional advisory coverage: Shields against legal costs if consulting experts during development.

Is Business Insurance Required for Informal or Cash-Based Operations?

Informal businesses, including cash-based operations, may still need insurance to avoid personal financial risk. Considerations include:

- Liability claims: A customer could sue even without a formal business entity.

- Asset protection: Personal savings or property may be at risk without coverage.

- Contract requirements: Clients or landlords might mandate insurance for collaborations or rentals.

Do you need a business license to be insured?

Is a Business License Required to Obtain Insurance?

Whether you need a business license to secure insurance depends on the insurer, jurisdiction, and type of coverage. Most insurers require proof of a legally recognized business entity to issue policies, as operating without proper licensing may invalidate claims. For example:

- Insurers often verify business legitimacy to mitigate fraud risks.

- Licensing ensures compliance with local regulations, which affects policy eligibility.

- Certain industries (e.g., construction or healthcare) may face stricter licensing requirements to qualify for coverage.

How Business Licensing Affects Insurance Coverage

A valid business license demonstrates operational compliance, which insurers use to assess risk and determine premiums. Without it:

- Insurers may deny claims if the business operates illegally.

- Coverage gaps could arise if licensing violations are discovered post-claim.

- Specialized policies (e.g., professional liability) often require proof of industry-specific licenses.

Types of Insurance That May Require a Business License

Certain insurance policies explicitly mandate a business license as a prerequisite:

- General Liability Insurance: Often requires proof of legal business status.

- Commercial Auto Insurance: May need a license to validate business vehicle use.

- Workers’ Compensation: Licensing proves employer legitimacy for employee coverage.

Operating Without a License: Risks to Insurance Validity

Running an unlicensed business jeopardizes insurance validity in multiple ways:

- Claims may be denied due to non-compliance with local laws.

- Insurers can void policies retroactively if unlicensed status is revealed.

- Legal penalties for unlicensed operations might exclude coverage for fines or lawsuits.

Alternatives If You Lack a Business License

In rare cases, businesses without licenses might still obtain limited coverage:

- Freelancers or sole proprietors may qualify for personal liability policies with fewer requirements.

- Insurers might accept pending license applications or provisional permits.

- Non-licensed entities could explore industry-specific exceptions (e.g., informal trades).

What do I need for small business insurance?

Common Types of Small Business Insurance

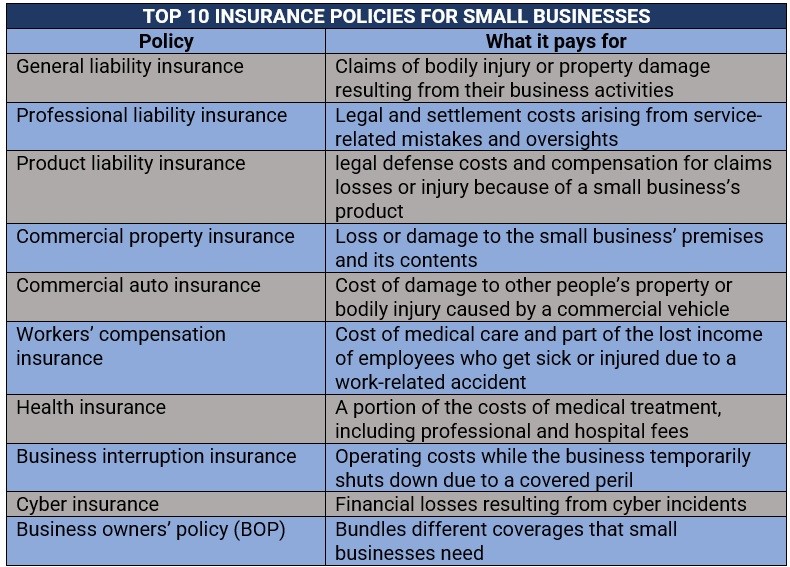

To protect your business, several insurance types are essential. The most common policies include:

- General Liability Insurance: Covers third-party claims like bodily injury, property damage, or advertising harm.

- Professional Liability Insurance: Protects against negligence, errors, or omissions in services (critical for consultants or advisors).

- Commercial Property Insurance: Safeguards physical assets like buildings, equipment, or inventory from fire, theft, or natural disasters.

Factors Influencing Your Insurance Needs

Your business’s specific risks determine the coverage required. Key factors include:

- Industry: High-risk sectors (e.g., construction) may need additional policies like workers’ compensation.

- Number of Employees: States often mandate workers’ comp if you have employees.

- Location: Local laws or environmental risks (e.g., floods) might require specialized coverage.

Steps to Obtain Small Business Insurance

Follow these steps to secure the right coverage:

- Assess Risks: Identify vulnerabilities (e.g., client lawsuits, equipment damage).

- Research Providers: Compare insurers specializing in your industry or business size.

- Customize Policies: Bundle coverage (e.g., a Business Owner’s Policy) for cost efficiency.

Cost Considerations for Business Insurance

Insurance costs vary based on multiple factors:

- Coverage Limits: Higher limits increase premiums but reduce out-of-pocket risks.

- Deductibles: Opting for a higher deductible can lower monthly payments.

- Claims History: A history of frequent claims may raise premiums.

Industry-Specific Insurance Requirements

Certain sectors have unique insurance obligations:

- Healthcare: Malpractice insurance for medical professionals.

- Transportation: Commercial auto insurance for company vehicles.

- Retail: Product liability insurance to cover defective goods.

Should I insure myself or my LLC?

Understanding Personal vs. LLC Insurance Needs

Determining whether to insure yourself or your LLC depends on your role, assets, and business risks. Personal insurance (e.g., health, disability, or life insurance) protects you individually, while LLC insurance (e.g., general liability, professional liability) safeguards the business. Consider:

- Liability separation: An LLC legally separates personal and business assets, but insurance adds another layer of protection.

- Risk exposure: If your work involves high client interaction, LLC insurance may be critical.

- Legal requirements: Some states mandate specific LLC coverage, while personal insurance is often voluntary.

Key Types of Insurance for Individuals

Personal insurance focuses on protecting your health, income, and assets. Essential policies include:

- Health insurance: Covers medical expenses unrelated to business activities.

- Disability insurance: Replaces income if you cannot work due to injury or illness.

- Umbrella liability: Extends coverage beyond standard policies for personal lawsuits.

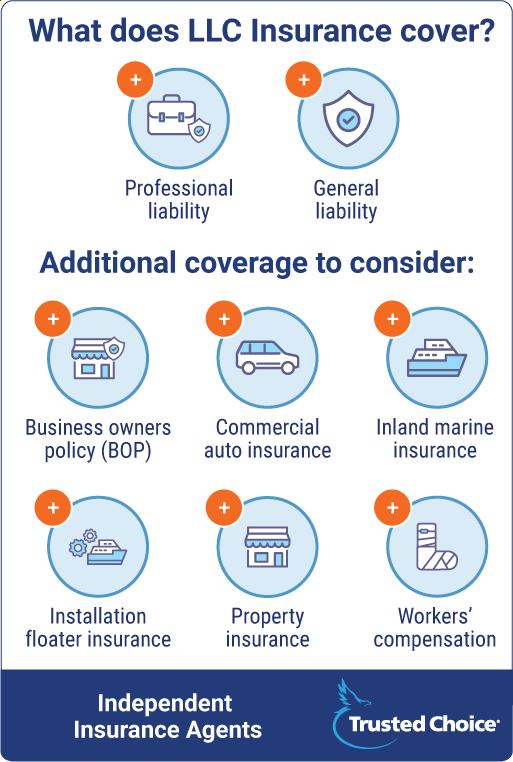

Essential Insurance Policies for Your LLC

LLC insurance shields the business from financial losses and legal claims. Critical policies include:

- General liability insurance: Covers third-party injuries, property damage, or advertising harm.

- Professional liability (E&O): Protects against claims of negligence or errors in services.

- Commercial property insurance: Safeguards business equipment, inventory, or workspace.

When to Prioritize Personal Insurance Over LLC Coverage

Focus on personal insurance if your livelihood or personal assets are at greater risk. Examples include:

- Self-employed without employees: Your health and income directly impact business operations.

- High personal net worth: Umbrella policies protect against lawsuits exceeding LLC coverage.

- Industry risks: Professions like consulting may expose you to personal liability claims.

When Your LLC Insurance Should Take Precedence

Prioritize LLC insurance if the business faces significant operational risks. Scenarios include:

- Multiple employees: Workers’ compensation is often legally required.

- Client contracts: Many agreements require proof of liability coverage.

- Physical business premises: Property insurance mitigates damage or theft risks.

Frequently Asked Questions (FAQs)

Can You Get Business Insurance Without a Business License?

Yes, in some cases, you can obtain business insurance without a business license, but this depends on the insurer and the nature of your business. Certain types of coverage, like general liability insurance or professional liability insurance, may be available to freelancers, independent contractors, or sole proprietors operating without formal licensing. However, insurers often require proof of legitimate business activity, such as contracts, client invoices, or tax documents. Operating without a license may limit your coverage options and could expose you to legal or financial risks if local regulations mandate licensing for your industry.

Why Do Some Insurers Require a Business License for Coverage?

Insurers may require a business license to verify that your operations comply with local laws, reducing their risk of covering illegitimate or high-risk activities. A license serves as proof of legitimacy, confirming that your business meets regulatory standards, zoning requirements, and industry-specific regulations. Without this documentation, insurers might view your business as higher risk or question its long-term viability, potentially leading to higher premiums or denial of coverage.

What Types of Business Insurance Might Not Require a License?

Certain policies, such as professional liability insurance (errors and omissions) or equipment insurance, may be accessible without a business license, especially for solopreneurs or gig workers. Commercial auto insurance might also be obtainable if you use vehicles for work but lack formal licensing. However, these exceptions vary by insurer and jurisdiction. Always clarify requirements upfront, as industry-specific policies (e.g., construction or healthcare) are more likely to mandate licensing.

What Are the Risks of Getting Insurance Without a Business License?

While possible, securing insurance without a license carries risks. If a claim arises, insurers might investigate your business’s legal standing and deny coverage if unlicensed operations violate policy terms. Additionally, local authorities could penalize you for operating without required licenses, even if you have insurance. This could leave you financially liable for damages or legal fees. Always consult legal or insurance professionals to ensure compliance and avoid coverage gaps or legal complications.

Leave a Reply

Our Recommended Articles