Carry Liability Insurance

Liability insurance serves as a critical safeguard against financial risks arising from legal claims due to injuries, property damage, or negligence. Whether for individuals, businesses, or professionals, this coverage helps mitigate the costs of lawsuits, medical expenses, or repair bills that could otherwise devastate personal finances or operational stability. In an increasingly litigious society, even minor accidents can lead to costly legal battles, making liability protection indispensable. Policies vary widely, tailored to specific needs—from general coverage for homeowners to specialized plans for industries like healthcare or construction. Understanding the scope, limits, and exclusions of a policy is essential to ensure adequate protection, balancing affordability with comprehensive risk management.

- Understanding the Importance of Carry Liability Insurance

- What does carrier liability mean in insurance?

-

How much is

- At what point should you only carry liability insurance on your car?

-

Why carry general liability insurance?

- Why Is General Liability Insurance Essential for Businesses?

- How Does General Liability Insurance Mitigate Financial Risks?

- What Legal Protections Does General Liability Insurance Offer?

- Why Do Clients and Contracts Require General Liability Insurance?

- How Does General Liability Insurance Support Business Continuity?

- Frequently Asked Questions (FAQs)

Understanding the Importance of Carry Liability Insurance

What is Carry Liability Insurance?

Carry Liability Insurance is a policy designed to protect individuals or businesses from financial losses resulting from claims of negligence, property damage, or bodily injury caused to third parties. It covers legal fees, settlements, and medical costs if the insured is found legally responsible. This insurance is critical for professions involving physical work, client interactions, or asset management, as it mitigates risks associated with unforeseen accidents or errors.

See AlsoComputer Repair Business Insurance| Coverage Areas | Key Benefits | Common Claims |

|---|---|---|

| Bodily Injury | Medical expense coverage | Slip-and-fall incidents |

| Property Damage | Repair/replacement costs | Accidental destruction |

| Legal Defense | Lawyer and court fees | Lawsuits |

Who Needs Carry Liability Insurance?

This insurance is essential for contractors, freelancers, healthcare providers, and businesses handling client assets. For example, a contractor might face claims if a tool damages a client’s property, while a fitness trainer could be liable for a client’s injury. Even small businesses benefit, as lawsuits can cripple finances without coverage.

| Profession | Risk Exposure | Recommended Coverage |

|---|---|---|

| Contractors | Property damage | $1M+ general liability |

| Healthcare Workers | Malpractice claims | Professional liability |

| Freelancers | Client disputes | Errors & omissions |

Types of Carry Liability Insurance Coverage

Common types include General Liability, Professional Liability, and Product Liability Insurance. General Liability covers accidents on business premises, while Professional Liability addresses errors in services (e.g., incorrect advice). Product Liability applies to manufacturers for defective products.

See Also Can You Present an Idea to a Venture Capitalist or Do You Have to Have a Business Plan

Can You Present an Idea to a Venture Capitalist or Do You Have to Have a Business Plan| Type | Description | Example |

|---|---|---|

| General Liability | Physical risks | Customer injury in-store |

| Professional Liability | Service errors | Architect’s design flaw |

| Product Liability | Defective goods | Faulty electronics |

How to Choose the Right Coverage

Assess industry risks, business size, and client requirements. For instance, construction firms need higher coverage limits than consultants. Review policy exclusions, compare quotes, and consult an insurance broker to align coverage with specific risks.

| Step | Action | Consideration |

|---|---|---|

| Risk Assessment | Identify vulnerabilities | Past claims history |

| Policy Limits | Set coverage amount | State regulations |

| Broker Consultation | Customize plan | Budget constraints |

Common Misconceptions About Carry Liability Insurance

Many believe small businesses don’t need it or that personal insurance suffices. However, even home-based businesses face liability risks, and personal policies exclude commercial activities. Additionally, “occurrence-based” vs. “claims-made” policies are often misunderstood, affecting coverage timelines.

See Also What Are the Different Stages in Startup Funding?

What Are the Different Stages in Startup Funding?| Misconception | Reality | Impact |

|---|---|---|

| I’m too small to be sued | Lawsuits target all sizes | Financial ruin |

| Personal insurance covers it | Commercial exclusions apply | Denied claims |

| All policies are the same | Coverage varies widely | Gaps in protection |

What does carrier liability mean in insurance?

What Is Carrier Liability in Insurance?

Carrier liability refers to the legal responsibility of a transportation company (carrier) for loss, damage, or delay of goods during transit. In insurance, this concept determines the extent to which a carrier is financially accountable under contractual terms or legal frameworks. It often involves predefined limits based on industry standards, regulations, or agreements between the carrier and the shipper.

See Also Where Can I Find a Comprehensive List of All Venture Capital Firms in the Us?

Where Can I Find a Comprehensive List of All Venture Capital Firms in the Us?- Legal responsibility: Carriers must compensate for losses caused by negligence or failure to meet service terms.

- Coverage scope: Typically applies to goods in transit, including air, sea, rail, or road transport.

- Limited liability: Many carriers operate under standardized liability limits unless additional insurance is purchased.

Types of Carrier Liability Coverage

Carrier liability insurance varies based on the mode of transport and contractual agreements. Common types include limited liability (default coverage under laws like the Carmack Amendment) and full-value liability (enhanced protection). Shippers often purchase supplemental cargo insurance to fill gaps in carrier liability coverage.

- Limited liability: Covers a fixed amount per pound or unit, often insufficient for high-value goods.

- All-risk coverage: Protects against most perils unless explicitly excluded.

- Named-peril policies: Covers only risks specified in the contract, such as theft or fire.

Legal Frameworks Governing Carrier Liability

Carrier liability is shaped by international conventions and national laws. For example, the Hague-Visby Rules govern maritime transport, while the Montreal Convention applies to air cargo. These frameworks set liability limits and define acceptable claims.

- International agreements: CMR Convention (road), Warsaw/Montreal Conventions (air).

- Liability caps: Maritime carriers may limit liability to ~$500 per container under Hague-Visby.

- Mandatory compliance: Carriers must adhere to local and international regulations to avoid penalties.

Exclusions in Carrier Liability Insurance

Carrier liability policies often exclude specific risks, shifting responsibility to shippers. Common exclusions include inherent vice (natural deterioration), improper packaging, or force majeure events like natural disasters.

- Force majeure: Wars, earthquakes, or strikes are typically excluded.

- Negligent packaging: Damage due to insufficient packaging voids claims.

- Concealed damage: Losses discovered post-delivery may not be covered.

Filing a Claim Under Carrier Liability

To claim compensation, shippers must follow strict procedures, including timely notification and documentation. Failure to comply may result in denied claims.

- Immediate reporting: Notify the carrier within 24–48 hours of discovering damage.

- Documentation: Provide bills of lading, photos, and inspection reports.

- Legal deadlines: File lawsuits within 9–12 months, as per conventions like CMR.

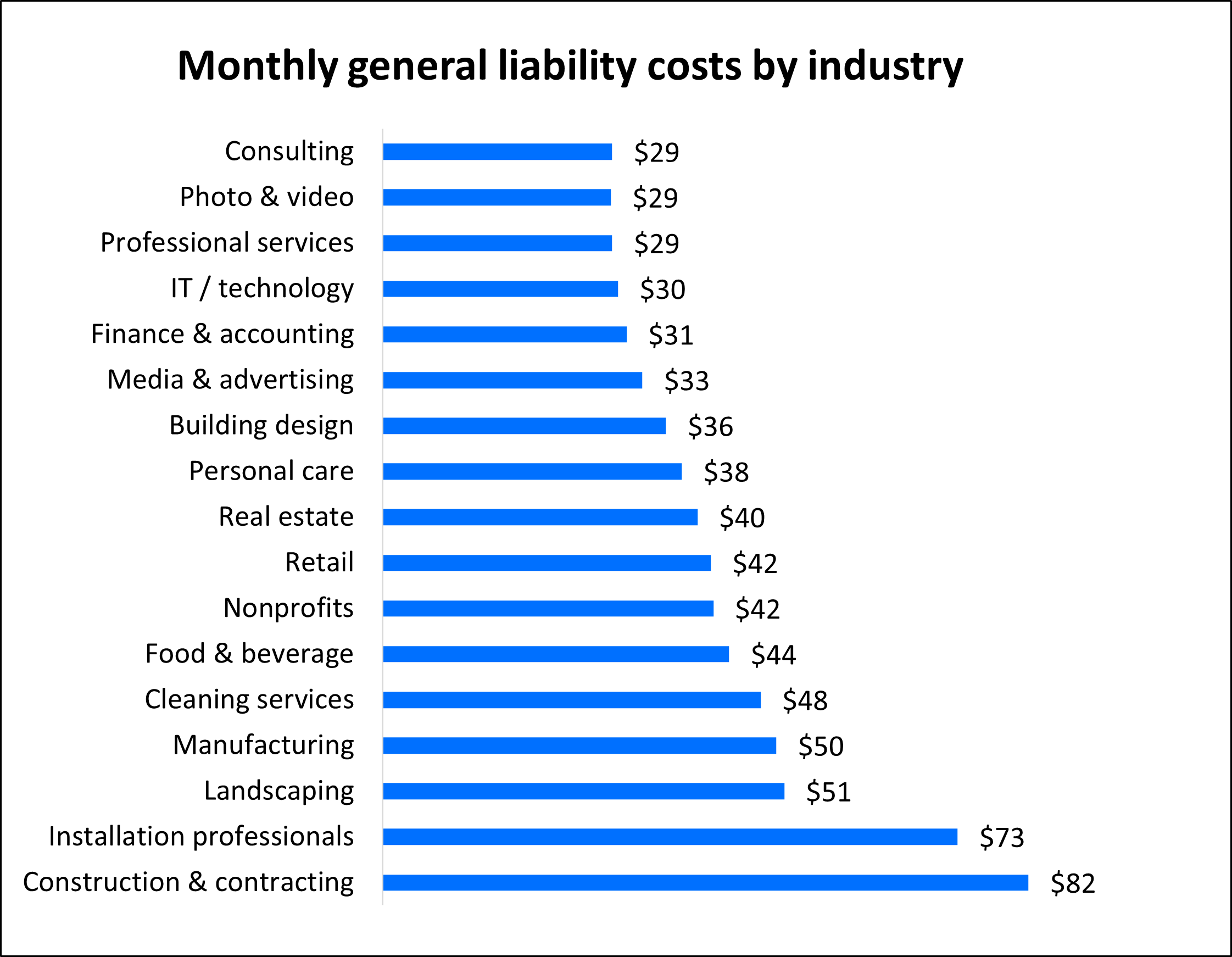

How much is $1,000,000 liability insurance a month?

Factors Influencing the Cost of $1,000,000 Liability Insurance

The monthly cost of a $1,000,000 liability insurance policy depends on several variables.

- Industry and risk level: High-risk sectors like construction or healthcare often pay higher premiums.

- Business size: Larger companies with more employees or clients may face increased costs.

- Coverage type: General liability vs. professional liability insurance can vary in pricing.

- Claims history: A history of frequent claims may raise premiums.

- Location: States with higher litigation rates or regulatory requirements may increase costs.

On average, small businesses might pay $25 to $50 per month for a $1 million liability policy.

- Low-risk industries (e.g., consulting): Closer to $25–$35/month.

- Medium-risk industries (e.g., retail): Around $35–$45/month.

- High-risk industries (e.g., roofing): $50–$200+/month due to elevated exposure.

How to Get an Accurate Quote for $1,000,000 Coverage

To determine your exact monthly cost, follow these steps:

- Contact insurers directly: Provide details about your business operations and risks.

- Use online tools: Many providers offer instant quote calculators.

- Compare policies: Evaluate coverage limits, exclusions, and deductibles.

- Consider bundling: Combining liability insurance with other policies (e.g., property insurance) may lower costs.

Ways to Reduce Your Liability Insurance Costs

Lower your monthly premiums with these strategies:

- Implement risk management practices: Safety training or improved workplace protocols can reduce claims risk.

- Opt for higher deductibles: Accepting a higher out-of-pocket deductible may lower monthly payments.

- Maintain a clean claims history: Avoid frequent or severe claims to qualify for discounts.

- Review coverage annually: Adjust policies as your business evolves to avoid overpaying.

Why $1,000,000 Liability Insurance Is Essential for Businesses

A $1 million policy provides critical financial protection:

- Legal compliance: Many contracts or state regulations require this coverage.

- Lawsuit protection: Covers legal fees, settlements, or judgments up to $1 million.

- Client trust: Demonstrates professionalism and reliability to customers.

- Asset safeguarding: Shields business assets from being seized in litigation.

At what point should you only carry liability insurance on your car?

When Your Car’s Value is Significantly Lower Than Insurance Costs

Carrying only liability insurance becomes practical when your vehicle’s market value is low enough that comprehensive or collision coverage would cost more than the car’s worth. For example:

- Older vehicles with high mileage or significant wear and tear.

- When annual premiums for full coverage exceed 10% of the car’s current value.

- If repair costs for minor accidents would outweigh the car’s depreciated value.

If You Can Afford to Replace the Vehicle Out of Pocket

Opting for liability-only coverage may be viable if you have sufficient savings to replace or repair the car without financial strain. Consider this if:

- You have an emergency fund covering potential vehicle replacement.

- The car is a secondary or non-essential vehicle in your household.

- You prioritize lower monthly premiums over potential future repair costs.

When the Car is Fully Paid Off

Owners of paid-off vehicles have more flexibility to drop comprehensive/collision coverage. This applies when:

- There’s no lienholder or loan agreement requiring full coverage.

- The car’s age or condition makes repairs impractical.

- You’re willing to assume financial responsibility for damage to your own vehicle.

Drivers classified as high-risk (e.g., due to accidents or violations) might choose liability-only to reduce costs when:

- Full coverage premiums become prohibitively expensive.

- You’re temporarily using the car while rebuilding your driving record.

- The vehicle isn’t driven frequently, lowering exposure to risk.

When Using the Car for Short-Term or Limited Purposes

Liability-only insurance may suffice for vehicles with limited use, such as:

- Seasonal or recreational vehicles stored most of the year.

- Cars used exclusively for short commutes or occasional errands.

- Backup vehicles that could be easily replaced without significant financial impact.

Why carry general liability insurance?

Why Is General Liability Insurance Essential for Businesses?

General liability insurance safeguards businesses from financial losses arising from third-party claims, including bodily injury, property damage, or advertising-related disputes. Without it, companies risk paying out-of-pocket for legal fees, medical bills, or settlements, which can cripple operations.

- Protects against unexpected lawsuits and legal expenses.

- Covers medical costs if someone is injured on your premises.

- Shields your business from reputational damage caused by public disputes.

How Does General Liability Insurance Mitigate Financial Risks?

This insurance transfers financial liability to the insurer, reducing the burden of costly claims. For example, if a client slips and falls in your office, the policy covers their medical bills and potential legal fees.

- Prevents cash flow disruptions from sudden expenses.

- Supports settlement negotiations without draining business funds.

- Covers property damage caused by your operations.

What Legal Protections Does General Liability Insurance Offer?

It provides legal defense coverage, even for groundless claims. Lawsuits can arise from accidents, defamation, or copyright infringement, and defending against them requires significant resources.

- Pays for attorney fees and court costs.

- Addresses libel or slander allegations in advertising.

- Handles settlement demands to avoid prolonged litigation.

Why Do Clients and Contracts Require General Liability Insurance?

Many clients and vendors mandate proof of insurance before collaboration. It signals professionalism and ensures you can cover liabilities, making your business a safer partner.

- Meets contractual obligations for projects or partnerships.

- Enhances credibility during client negotiations.

- Fulfills industry-specific regulations (e.g., construction, retail).

How Does General Liability Insurance Support Business Continuity?

By absorbing unforeseen costs, this insurance ensures operations continue smoothly despite claims. Without it, a single lawsuit could force a business to downsize or close.

- Maintains operational stability during legal challenges.

- Preserves business assets from seizure or liquidation.

- Reduces stress on management and staff during crises.

Frequently Asked Questions (FAQs)

What is Carry Liability Insurance?

Carry Liability Insurance is a type of coverage designed to protect individuals or businesses from financial losses resulting from claims of injury, property damage, or negligence caused to third parties. This insurance is critical for professionals, contractors, or service providers whose work involves potential risks to others. It typically covers legal fees, medical expenses, and repair costs if the policyholder is found legally responsible. Without this coverage, individuals may face significant out-of-pocket expenses in lawsuits or settlements.

Who Needs to Carry Liability Insurance?

Liability insurance is essential for anyone whose actions or services could inadvertently harm others or their property. Business owners, freelancers, healthcare providers, contractors, and event organizers often require this coverage. For example, a construction company might need it to address accidents on-site, while a consultant could use it to mitigate risks of professional errors. Certain industries or clients may also mandate this insurance as a contractual requirement to ensure accountability.

How Much Liability Insurance Should I Carry?

The appropriate coverage amount depends on factors like industry risks, business size, and potential claim severity. General liability policies often start at $1 million per occurrence, but high-risk fields like healthcare or construction may require higher limits. Umbrella policies can supplement existing coverage for added protection. Consulting an insurance professional helps tailor limits to specific needs, ensuring compliance with legal or client requirements while avoiding overpayment for unnecessary coverage.

What Does Liability Insurance Typically Exclude?

While liability insurance covers third-party claims, it usually excludes intentional acts, employee injuries (covered by workers’ compensation), or professional errors (covered by E&O insurance). Property damage to the policyholder’s own assets or contractual liabilities not explicitly included in the policy may also be excluded. Reviewing policy terms thoroughly and adding endorsements or separate policies for uncovered risks is crucial to avoid gaps in protection.

Leave a Reply

Our Recommended Articles