Vending Machine Business Insurance

The vending machine industry offers entrepreneurs a flexible and scalable business model, but like any enterprise, it comes with inherent risks that require strategic protection. From equipment malfunctions and theft to liability claims stemming from product safety or customer accidents, unforeseen events can disrupt operations and lead to significant financial losses. Securing comprehensive insurance tailored to vending machine businesses is essential to safeguard assets, mitigate liability, and ensure continuity. Whether you operate a single machine or a vast network, understanding coverage options—such as general liability, commercial property, product liability, and business interruption insurance—is critical. This article explores key policies, risk management insights, and tips to choose the right protection for your unique needs.

- Understanding Vending Machine Business Insurance: Coverage, Costs, and Key Considerations

- What type of insurance do vending machines need?

- How much is insurance for a vending machine business?

-

How much does a

-

Do I need an LLC for a vending machine?

- What Are the Advantages of Forming an LLC for a Vending Machine Business?

- Does a Vending Machine Business Require Legal Protection?

- How Does an LLC Affect Taxes for a Vending Machine Business?

- What Steps Are Needed to Form an LLC for a Vending Machine Business?

- Are There Alternatives to an LLC for a Vending Machine Business?

- Frequently Asked Questions (FAQs)

Understanding Vending Machine Business Insurance: Coverage, Costs, and Key Considerations

What Does Vending Machine Business Insurance Cover?

Vending machine business insurance typically includes general liability, property insurance, and product liability coverage. General liability protects against third-party injuries (e.g., slips near machines), while property insurance covers damage to machines from theft, fire, or vandalism. Product liability safeguards against claims related to contaminated or defective products sold through your machines. Some policies may also include business interruption insurance to compensate for lost income during repairs.

See AlsoComputer Repair Business Insurance| General Liability | Covers injuries/damages to third parties |

| Property Insurance | Protects machines and inventory |

| Product Liability | Addresses product-related claims |

Factors Influencing Insurance Costs for Vending Machines

Insurance premiums depend on machine location (high-risk areas cost more), number of machines, revenue, and coverage limits. Providers may also assess risks like crime rates in operating areas or whether machines sell perishable items. Installing security features (GPS tracking, cameras) can reduce costs.

| Location | High-crime areas increase premiums |

| Revenue | Higher sales may require broader coverage |

| Security Measures | Discounts for anti-theft devices |

How to Choose the Right Insurance Provider

Look for insurers specializing in small businesses or vending operations. Compare coverage exclusions, deductibles, and claim response times. Verify the provider’s financial stability through ratings from agencies like A.M. Best. Ask about add-ons like equipment breakdown coverage.

See Also What Vcs or Angel Investors Are Interested in the Food Industry

What Vcs or Angel Investors Are Interested in the Food Industry| Specialization | Providers familiar with vending risks |

| Coverage Flexibility | Tailored policies for unique needs |

| Customer Reviews | Feedback on claim handling |

Common Claims Filed by Vending Machine Owners

Frequent claims include theft of machines or cash, vandalism, electrical malfunctions, and customer injuries. For example, a damaged machine might leak refrigerant, causing slip hazards. Product recalls due to contamination also trigger claims.

| Theft/Vandalism | Most common physical risks |

| Equipment Failure | Electrical or mechanical issues |

| Product Recalls | Contaminated snacks/beverages |

Legal Requirements for Vending Machine Insurance

Most states require general liability insurance for public-facing businesses. If leasing machines, lenders may mandate property insurance. Contracts with property owners (e.g., malls) often stipulate minimum coverage limits.

See Also Can You Present an Idea to a Venture Capitalist or Do You Have to Have a Business Plan

Can You Present an Idea to a Venture Capitalist or Do You Have to Have a Business Plan| State Laws | Liability coverage often mandatory |

| Lease Agreements | Property owners’ requirements |

| Lender Policies | Insurance for financed equipment |

What type of insurance do vending machines need?

General Liability Insurance for Vending Machines

Vending machines require general liability insurance to protect against third-party claims, such as bodily injury or property damage. For example, if a customer slips near the machine or the machine malfunctions and damages a wall, this coverage helps pay for legal fees or repairs.

- Bodily injury claims: Covers medical costs if someone is hurt near the machine.

- Property damage: Addresses costs if the machine damages the location it’s placed in.

- Legal defense: Supports expenses if a lawsuit arises from an incident.

Commercial Property Insurance for Vending Machines

Commercial property insurance safeguards the vending machines themselves against physical damage or loss due to events like fire, theft, or vandalism. This ensures business continuity by covering repair or replacement costs.

- Physical damage coverage: Protects against fire, storms, or accidental breakage.

- Theft protection: Reimburses losses if machines are stolen or burglarized.

- Vandalism repairs: Covers costs to fix intentional damage to the machine.

Product Liability Insurance for Vending Machines

Product liability insurance is critical if a customer claims harm from a product sold in the vending machine, such as food poisoning or allergic reactions. This coverage mitigates financial risks from lawsuits.

- Contamination claims: Addresses incidents involving spoiled or unsafe products.

- Mislabeling issues: Covers lawsuits due to incorrect allergen or ingredient information.

- Legal settlements: Helps pay for court-ordered compensation or settlements.

Business Interruption Insurance for Vending Machine Operators

Business interruption insurance compensates for lost income if a vending machine becomes inoperable due to covered events, such as natural disasters or equipment failure.

- Lost revenue coverage: Replaces income during downtime.

- Relocation costs: Covers expenses to move machines to a new location if needed.

- Ongoing expenses: Helps pay rent or lease fees for machine placements during repairs.

Commercial Auto Insurance for Vending Machine Delivery Services

If vehicles are used to transport or service vending machines, commercial auto insurance is essential to cover accidents, cargo damage, or liability during transit.

- Vehicle accidents: Covers repairs or medical bills from collisions.

- Cargo protection: Insures products or machine parts during transport.

- Third-party liability: Addresses damages caused to other drivers or property.

How much is insurance for a vending machine business?

Factors Influencing Vending Machine Business Insurance Costs

The cost of insurance for a vending machine business depends on variables like coverage type, number of machines, location, and annual revenue. For example, a business with high-risk products or machines in high-traffic areas may pay more.

- Coverage scope: Basic liability vs. comprehensive policies.

- Machine quantity: More machines often mean higher premiums.

- Geographic risks: Areas prone to theft or vandalism increase costs.

Common Types of Insurance for Vending Machine Businesses

Vending businesses typically require general liability, product liability, and commercial property insurance. Optional coverage like equipment breakdown or cyber insurance may also apply.

- General liability: Covers third-party injuries or property damage.

- Product liability: Protects against claims from defective products.

- Commercial property insurance: Safeguards machines and inventory.

Average Insurance Costs for Vending Machine Businesses

Annual premiums typically range from $500 to $3,000+, depending on coverage. Small operations may pay closer to $500, while larger businesses with multiple machines might exceed $3,000.

- Basic liability: $400–$800/year.

- Full coverage: $1,200–$3,000/year.

- Add-ons: Equipment insurance adds $200–$500/year.

Reducing costs involves risk mitigation, bundling policies, and maintaining safety protocols. Insurers may offer discounts for proactive measures.

- Install security cameras: Lowers theft-related risks.

- Bundle policies: Combine liability and property insurance.

- Regular maintenance: Reduces equipment failure claims.

Importance of Liability Insurance for Vending Machine Owners

Liability coverage is critical to protect against lawsuits or financial losses from accidents or product issues. Without it, legal fees alone could bankrupt a small business.

- Customer injuries: Slip-and-fall claims near machines.

- Product recalls: Contaminated or mislabeled items.

- Property damage: Machine malfunctions damaging a site.

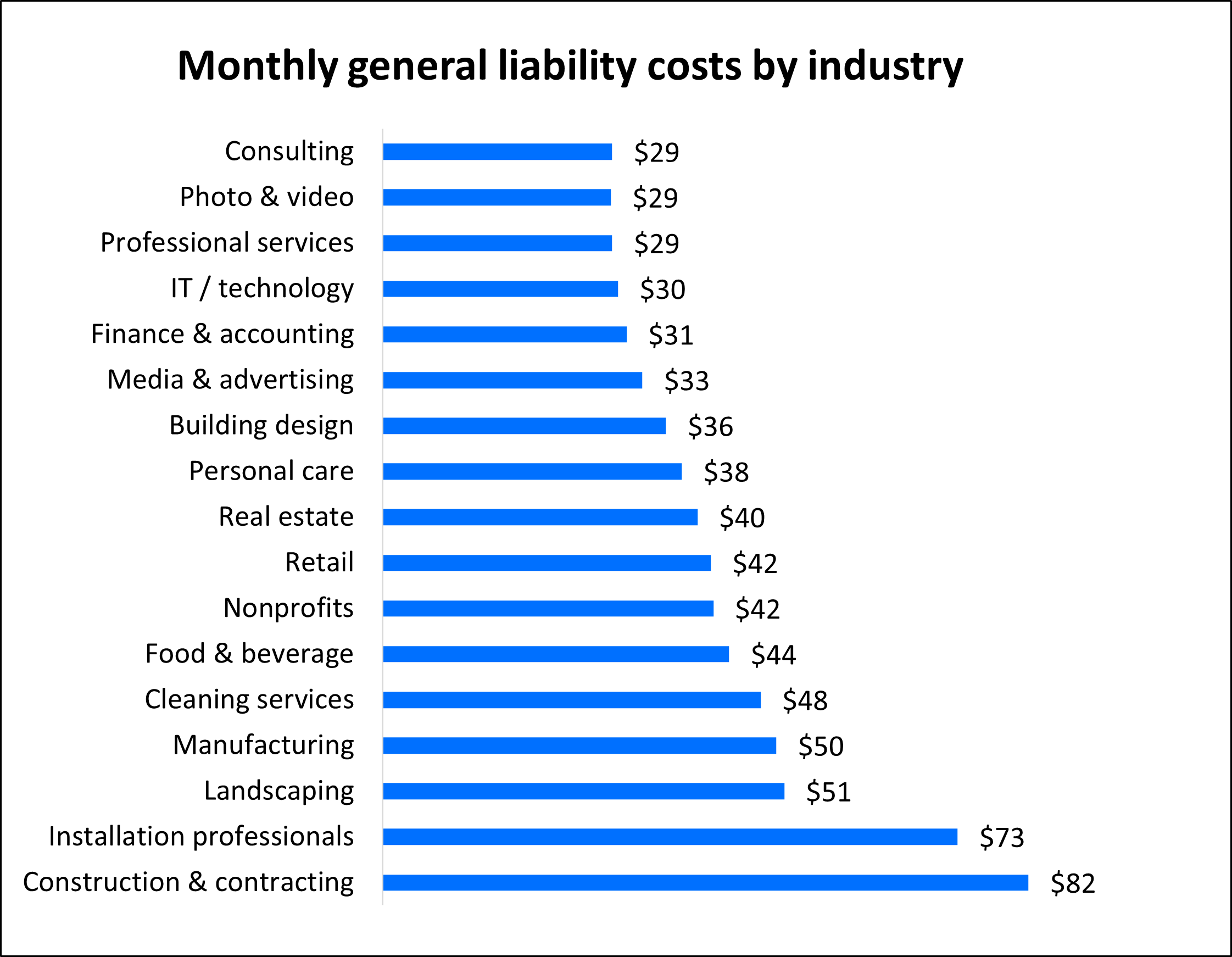

How much does a $1,000,000 liability insurance policy cost?

The cost of a $1,000,000 liability insurance policy varies widely depending on factors such as industry, business size, location, claims history, and coverage specifics. On average, small businesses might pay between $300 to $1,500 annually, while high-risk industries like construction or healthcare could face premiums ranging from $5,000 to $15,000+ per year. To get an accurate quote, insurers evaluate risk exposure and operational details.

What Factors Influence the Cost of a $1,000,000 Liability Insurance Policy?

The premium for a $1,000,000 liability policy is shaped by multiple variables. Riskier industries typically pay higher rates due to increased exposure to claims. For example:

- Industry type: Construction or manufacturing often incurs higher premiums than retail or consulting.

- Business size: Larger companies with more employees or clients may face elevated costs.

- Claims history: A track record of frequent claims can raise premiums significantly.

- Location: States with higher litigation rates or regulatory requirements may increase costs.

- Coverage limits and deductibles: Higher deductibles can lower premiums, while additional endorsements may raise them.

Industries with inherent risks or regulatory demands often see higher liability insurance costs. For example:

- Construction: High risk of property damage or injuries leads to premiums of $5,000–$20,000+ annually.

- Healthcare: Malpractice exposure can push costs to $10,000–$30,000+.

- Consulting: Lower physical risks may result in premiums closer to $500–$2,000.

- Retail: Slip-and-fall risks may cost $1,000–$4,000 yearly.

- Manufacturing: Product liability concerns often mean $3,000–$10,000+ premiums.

Can You Lower the Cost of a $1,000,000 Liability Policy?

Yes, businesses can reduce premiums through proactive risk management and strategic adjustments:

- Implement safety protocols: Training programs or equipment upgrades may qualify for discounts.

- Bundle policies: Combining liability with property or auto insurance often lowers costs.

- Choose higher deductibles: Opting for a $2,500 deductible instead of $500 can reduce premiums.

- Review coverage annually: Adjust limits or remove unnecessary add-ons as operations evolve.

- Improve credit score: Insurers in many states use credit history to calculate risk.

How Do Insurance Providers Calculate Quotes?

Insurers assess risk exposure using detailed criteria to determine premiums:

- Revenue and payroll: Higher revenue or payroll often correlates with greater liability risks.

- Number of employees: More employees increase the likelihood of workplace incidents.

- Services or products offered: High-risk services (e.g., roofing) attract higher rates.

- Claims frequency: A history of claims signals higher future risk to insurers.

- Geographic factors: Operating in areas prone to lawsuits or natural disasters impacts costs.

What Are Common Exclusions in a $1,000,000 Liability Policy?

Most policies exclude certain risks, requiring additional coverage for full protection:

- Intentional acts: Damages from deliberate misconduct are rarely covered.

- Contractual liabilities: Breaches of contract may need separate endorsements.

- Professional errors: Mistakes in services often require errors and omissions (E&O) insurance.

- Employee injuries: Workers’ compensation is needed for workplace injuries.

- Property damage from owned assets: General liability may exclude damage to business-owned property.

Do I need an LLC for a vending machine?

What Are the Advantages of Forming an LLC for a Vending Machine Business?

Forming an LLC (Limited Liability Company) for a vending machine business offers several benefits. It provides legal protection by separating personal and business assets, reducing personal liability if the business faces lawsuits or debts. Additionally, LLCs offer tax flexibility, allowing owners to choose how their business income is taxed.

- Asset protection: Shields personal savings, homes, or vehicles from business-related liabilities.

- Tax options: Choose between pass-through taxation or corporate tax structures.

- Credibility: Enhances professionalism when dealing with suppliers or leasing partners.

Does a Vending Machine Business Require Legal Protection?

While not legally required, an LLC adds a layer of legal protection critical for mitigating risks. Vending machines involve interactions with public spaces, contracts, and potential equipment malfunctions, which could lead to liability claims.

- Liability risks: Injuries from machine malfunctions or disputes over location contracts.

- Contractual obligations: Protects against breaches if unable to fulfill agreements.

- Debt separation: Business debts won’t impact personal credit scores.

How Does an LLC Affect Taxes for a Vending Machine Business?

An LLC provides tax flexibility, allowing owners to opt for pass-through taxation (income reported on personal tax returns) or elect corporate taxation. This structure can optimize deductions for expenses like machine maintenance, inventory, and travel.

- Pass-through taxation: Avoids double taxation seen in corporations.

- Deductible expenses: Write-offs for fuel, repairs, and licensing fees.

- Self-employment taxes: Owners pay Medicare/Social Security taxes on net earnings.

What Steps Are Needed to Form an LLC for a Vending Machine Business?

Forming an LLC involves state-specific processes, including registration, fees, and compliance. Key steps include choosing a business name, filing Articles of Organization, and obtaining licenses.

- Name registration: Ensure the name is unique and complies with state rules.

- Articles of Organization: File with the state and pay associated fees.

- Licensing: Obtain permits for vending operations and sales tax collection.

Are There Alternatives to an LLC for a Vending Machine Business?

Alternatives include operating as a sole proprietorship or partnership, which are simpler but lack liability protection. A corporation is another option but involves more complex regulations.

- Sole proprietorship: Easy setup but no asset protection.

- Partnership: Shared responsibility but personal liability risks remain.

- Corporation: Strong liability protection but higher administrative costs.

Frequently Asked Questions (FAQs)

What Types of Insurance Coverage Are Essential for a Vending Machine Business?

General liability insurance, commercial property insurance, and product liability insurance are critical for vending machine businesses. General liability protects against third-party claims like bodily injury or property damage caused by your machines. Commercial property insurance covers physical assets, such as vending machines, inventory, or storage facilities, from risks like theft, fire, or vandalism. Product liability insurance is vital if a customer claims illness or harm from a product sold in your machine. Additionally, consider business interruption insurance to offset lost income during unexpected closures and commercial auto insurance if you use vehicles for machine maintenance or restocking.

How Does Location Impact Vending Machine Insurance Costs?

Insurance premiums often reflect the risk level associated with your vending machine’s location. High-traffic areas, such as malls or schools, may increase liability exposure, potentially raising costs. Urban locations with higher crime rates could lead to elevated premiums for theft or vandalism coverage. Conversely, low-risk zones might reduce costs. Insurers also assess local regulations, such as health code compliance requirements, which may necessitate additional coverage. Always disclose your machine locations to ensure your policy accurately reflects site-specific risks.

Do I Need Insurance for Vending Machines I Don’t Own?

If you lease or operate machines owned by a third party, you may still require insurance. While the owner might have coverage for the machine itself, your business could be liable for accidents or damages caused during operation. Review lease agreements to confirm who is responsible for specific risks. Liability coverage is often non-negotiable, even for leased equipment, as your business could face lawsuits from customers or property owners. Consult your insurer to tailor a policy that aligns with contractual obligations and operational risks.

Can I Reduce Insurance Costs Through Risk Management Practices?

Yes, implementing risk mitigation strategies can lower premiums. Regular machine maintenance reduces malfunction risks, while security measures like surveillance cameras or tamper-proof locks deter theft. Training employees in safety protocols minimizes accident risks, and strict adherence to health codes prevents product liability claims. Insurers may offer discounts for documented safety practices or bundling policies like liability and property insurance. Additionally, opting for a higher deductible can reduce monthly premiums, but ensure your business can handle unexpected out-of-pocket costs.

Leave a Reply

Our Recommended Articles