What kind of insurance does a bookkeeper need?

Bookkeepers play a vital role in maintaining accurate financial records for businesses, but their work also comes with inherent risks. From handling sensitive client data to potential errors in financial reporting, even minor oversights can lead to significant legal or financial consequences. Securing the right insurance coverage is essential to safeguard both the bookkeeper’s business and professional reputation. This article explores the key types of insurance bookkeepers should consider, such as professional liability, general liability, and cyber liability policies. By understanding these protections, bookkeepers can mitigate risks, ensure compliance with client expectations, and focus on delivering reliable services with confidence.

Essential Insurance Coverage for Bookkeepers

Professional Liability Insurance (Errors & Omissions)

Professional Liability Insurance, also known as Errors & Omissions (E&O) Insurance, protects bookkeepers against claims of negligence, mistakes, or failure to deliver promised services. This coverage is critical because even minor errors in financial records or tax filings could lead to costly lawsuits. It typically covers legal fees, settlements, and court-awarded damages.

See AlsoAuto Detailing Business Insurance| Coverage Includes | Mistakes in bookkeeping, missed deadlines, incorrect financial advice |

| Key Benefits | Legal defense costs, client reimbursement, reputational protection |

| Why It’s Needed | Bookkeepers handle sensitive financial data; errors can lead to client losses |

General Liability Insurance

General Liability Insurance covers third-party claims of bodily injury, property damage, or advertising harm. For example, if a client slips in your office or their property is damaged during a consultation, this policy helps cover medical bills, repairs, or legal expenses. It’s a foundational coverage for all small businesses.

| Coverage Includes | Bodily injury, property damage, defamation claims |

| Key Benefits | Medical expense coverage, legal defense, settlement costs |

| Why It’s Needed | Protects against accidents that could disrupt operations or client trust |

Cyber Liability Insurance

Cyber Liability Insurance is vital for bookkeepers who store client data digitally. It addresses costs from data breaches, ransomware attacks, or unauthorized access to sensitive financial information. Coverage often includes client notification expenses, credit monitoring, and regulatory fines.

See AlsoBusiness Insurance for Candle Makers| Coverage Includes | Data breaches, ransomware, phishing attacks |

| Key Benefits | Breach response costs, legal liabilities, PR recovery |

| Why It’s Needed | Bookkeepers are prime targets for cyberattacks due to financial data access |

Commercial Property Insurance

Commercial Property Insurance safeguards physical assets like office equipment, computers, and furniture. If your workspace is damaged by fire, theft, or natural disasters, this insurance helps replace or repair essential tools. Home-based bookkeepers should verify if their homeowner’s policy covers business equipment.

| Coverage Includes | Equipment damage, inventory loss, building repairs |

| Key Benefits | Asset replacement, business continuity support |

| Why It’s Needed | Ensures operations continue despite physical damage or theft |

Business Owner’s Policy (BOP)

A Business Owner’s Policy (BOP) bundles General Liability and Commercial Property Insurance into one cost-effective package. Some providers also add Business Interruption Insurance, covering lost income during closures. Ideal for small bookkeeping firms, a BOP simplifies coverage while reducing premiums.

See AlsoDog Walking Business Insurance| Coverage Includes | Combined liability, property, and interruption coverage |

| Key Benefits | Lower costs, streamlined management, broader protection |

| Why It’s Needed | Offers comprehensive protection tailored to small business risks |

What type of insurance should bookkeepers have?

Professional Liability Insurance (Errors & Omissions Insurance)

Professional Liability Insurance, also known as Errors & Omissions (E&O) Insurance, is critical for bookkeepers to protect against claims of negligence, mistakes, or oversights in their work. This coverage addresses legal fees, settlements, or judgments if a client alleges financial harm due to errors in bookkeeping, tax filing, or financial reporting.

See AlsoCarry Liability Insurance- Protection against negligence claims (e.g., incorrect financial statements).

- Covers legal defense costs and settlements.

- Addresses client claims of financial loss due to errors.

General Liability Insurance

General Liability Insurance safeguards bookkeepers from third-party claims involving bodily injury, property damage, or advertising injury. While not directly tied to professional services, it covers incidents like client injuries at your office or accidental damage to a client’s property during meetings.

- Protects against physical accidents (e.g., a client slipping in your workspace).

- Covers property damage claims (e.g., spilling coffee on a client’s laptop).

- Addresses advertising-related disputes (e.g., copyright infringement in marketing materials).

Cyber Liability Insurance

Bookkeepers handle sensitive financial data, making Cyber Liability Insurance essential. This policy covers costs related to data breaches, ransomware attacks, or unauthorized access to client information, including legal fees, notifications, and credit monitoring services.

- Mitigates risks from data breaches or hacking incidents.

- Covers ransomware attack response costs.

- Funds client notifications and regulatory fines for non-compliance.

Business Owner’s Policy (BOP)

A Business Owner’s Policy (BOP) combines General Liability and Commercial Property Insurance into one package. It’s cost-effective for bookkeepers needing coverage for office space, equipment, and liability risks, such as fire damage or theft of business assets.

- Bundles property insurance (e.g., damaged computers or office furniture).

- Includes business interruption coverage for lost income during closures.

- Simplifies insurance management with combined policies.

Workers’ Compensation Insurance

If a bookkeeper employs staff, Workers’ Compensation Insurance is legally required in most states. It covers medical expenses and lost wages for employees injured on the job, reducing liability for workplace accidents.

- Covers employee injuries (e.g., repetitive strain from desk work).

- Protects against lawsuits from injured employees.

- Ensures compliance with state regulations for businesses with employees.

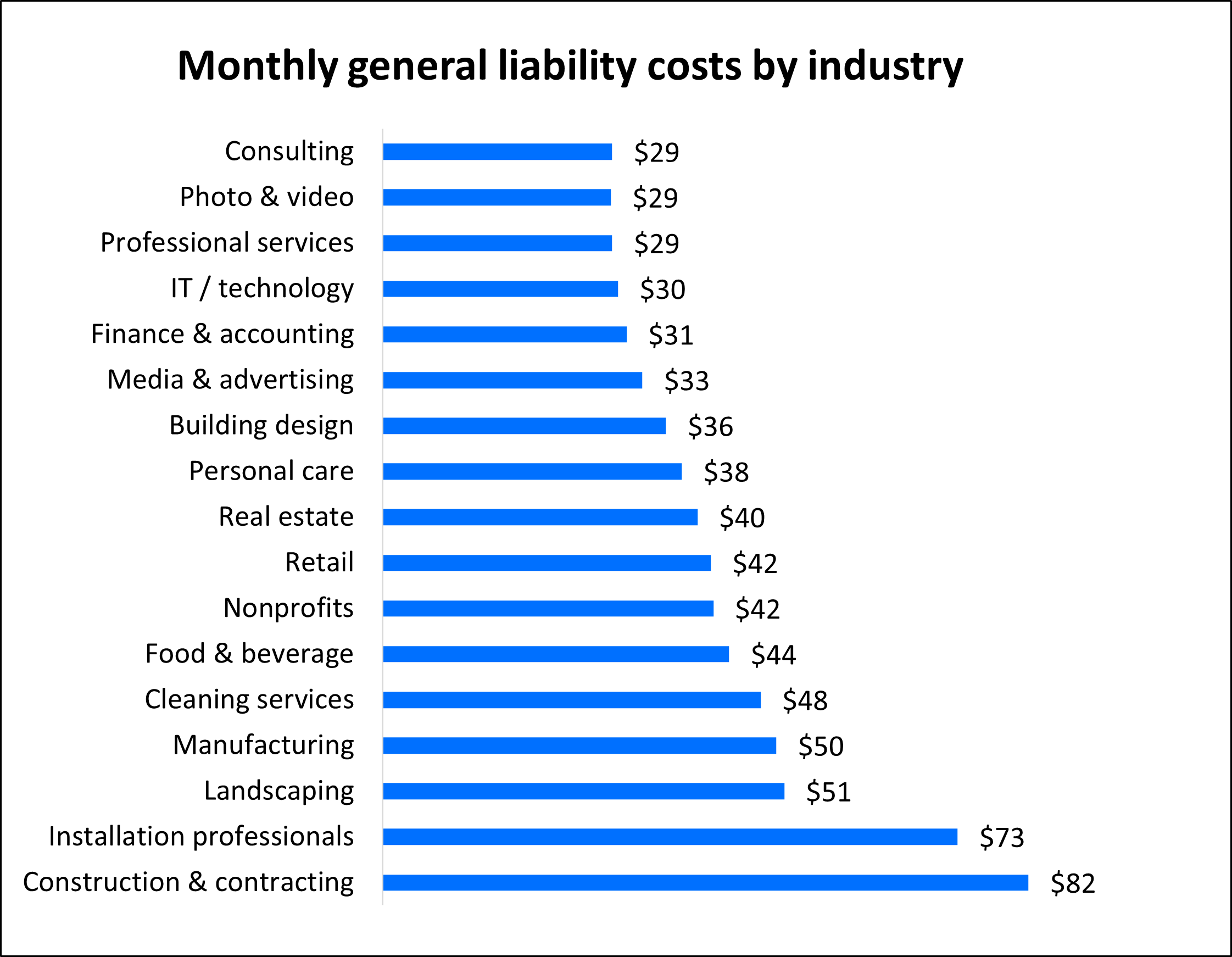

How much does a $1,000,000 liability insurance policy cost?

The cost of a $1,000,000 liability insurance policy varies widely based on factors like industry type, business size, location, and risk exposure. On average, small businesses might pay between $500 and $3,000 annually, while high-risk industries (e.g., construction) could see premiums upwards of $5,000 or more. Insurers also evaluate claims history, coverage limits, and deductibles to determine final rates.

What Factors Influence the Cost of a $1M Liability Policy?

The premium for a $1 million liability insurance policy depends on multiple variables. Business-specific risks and operational scale play a significant role in pricing.

- Industry risk level: High-risk sectors (e.g., construction) pay more due to greater exposure to accidents.

- Business location: States with higher litigation rates or strict regulations may increase costs.

- Claims history: A track record of frequent claims can lead to higher premiums.

Industry type is a primary driver of liability insurance costs. Insurers assess the likelihood of claims based on work environments and practices.

- Construction: Often pays $4,000–$10,000+ annually due to physical risks and equipment use.

- Consulting/Professional Services: Lower-risk fields may pay $500–$1,500/year.

- Retail/Hospitality: Moderate premiums ($1,000–$3,000) due to customer interaction risks.

Can You Lower the Cost of a $1 Million Liability Policy?

Businesses can adopt strategies to reduce premiums while maintaining adequate coverage.

- Increase deductibles: Higher out-of-pocket deductibles often lower annual premiums.

- Bundle policies: Combining liability insurance with other coverages (e.g., property) may yield discounts.

- Implement safety protocols: Reducing workplace risks through training or equipment can lower rates.

How Do Coverage Limits and Deductibles Impact Pricing?

Coverage limits and deductibles directly affect policy costs. A $1M policy’s structure balances risk and affordability.

- Higher limits: Exceeding $1M increases premiums but provides broader protection.

- Lower deductibles: Reduce upfront costs but raise annual premiums.

- Tailored endorsements: Adding specific coverage (e.g., cyber liability) may adjust pricing.

Why Compare Quotes from Multiple Insurance Providers?

Shopping around ensures businesses find competitive rates and optimal coverage for a $1M liability policy.

- Price variability: Insurers weigh risks differently, leading to significant quote differences.

- Customizable options: Providers may offer unique discounts or add-ons.

- Financial stability: Comparing insurers’ credit ratings ensures reliable claim payouts.

What liability does a bookkeeper have?

Professional Negligence and Errors

Bookkeepers may face liability for professional negligence if their work contains errors or omissions that cause financial harm to clients. This includes mistakes in financial statements, tax filings, or payroll processing. Courts may hold them accountable if they fail to meet the standard of care expected in their profession.

- Inaccurate financial records leading to tax penalties or audits.

- Failure to reconcile accounts, resulting in undetected fraud or discrepancies.

- Missed deadlines for tax submissions, incurring fines or interest charges.

Compliance with Laws and Regulations

Bookkeepers must ensure compliance with tax laws, financial regulations, and industry-specific standards. Liability arises if they knowingly or unknowingly facilitate illegal activities, such as tax evasion or money laundering.

- Non-compliance with IRS or local tax rules, triggering legal action.

- Overlooking anti-money laundering (AML) requirements.

- Misclassification of employees or contractors, violating labor laws.

Breach of Contractual Obligations

Bookkeepers may breach contractual terms outlined in service agreements, such as failing to deliver promised services or violating confidentiality clauses. Clients can pursue legal claims for damages.

- Unauthorized disclosure of sensitive financial data.

- Failure to perform duties as specified in the contract.

- Using client data for personal gain, violating trust agreements.

Legal Liability for Fraud or Misconduct

While rare, bookkeepers may face liability if involved in fraudulent activities, even unintentionally. This includes falsifying records or colluding with others to deceive stakeholders.

- Intentional manipulation of financial statements.

- Collusion with third parties to hide financial irregularities.

- Failure to report suspected fraud discovered during bookkeeping.

Data Security and Confidentiality Breaches

Bookkeepers handle sensitive financial information, making them liable for data breaches or failures to protect client data. This includes cyberattacks or improper storage of records.

- Inadequate cybersecurity measures leading to hacking incidents.

- Physical mishandling of documents, causing unauthorized access.

- Non-compliance with GDPR or other data privacy laws.

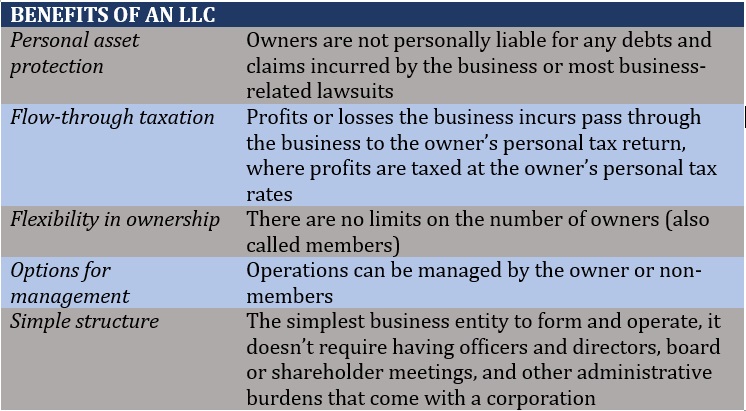

Can I operate an LLC without insurance?

Operating an LLC without insurance is legally permissible in many jurisdictions, but it carries significant risks. While there's no universal law mandating insurance for all LLCs, specific industries, contracts, or state regulations may require certain coverage. Without insurance, the LLC's personal asset protection could be jeopardized, exposing owners to personal liability in lawsuits or financial disputes.

Is Insurance Legally Required for an LLC?

Most states do not legally require general liability insurance for LLCs unless operating in regulated industries (e.g., construction, healthcare). However, specific situations may mandate coverage:

- Employees: Workers’ compensation insurance is mandatory if the LLC has employees.

- Professional services: Errors and omissions (E&O) insurance may be legally required for licensed professionals (e.g., lawyers, architects).

- Commercial vehicles: Auto insurance is compulsory if the LLC owns or uses vehicles for business.

Financial Risks of Operating Without Insurance

Operating uninsured exposes the LLC to financial vulnerabilities, including:

- Legal claims: Lawsuits (e.g., slip-and-fall accidents, product liability) could drain business funds.

- Contract breaches: Clients or partners may require proof of insurance in contracts; non-compliance risks lost deals.

- Personal liability: Courts may pierce the corporate veil, holding owners personally liable for debts.

Industry-Specific Insurance Requirements

Certain industries have non-negotiable insurance mandates to operate legally:

- Healthcare: Malpractice insurance for medical practitioners.

- Construction: General liability and surety bonds for contractors.

- Transportation: Cargo or commercial auto insurance for logistics companies.

Impact on Business Credibility and Partnerships

Operating without insurance can harm an LLC's reputation and growth opportunities:

- Client trust: Many clients avoid uninsured businesses due to perceived unreliability.

- Lease agreements: Landlords often require commercial property insurance for rented spaces.

- Vendor contracts: Suppliers may demand proof of insurance to mitigate supply chain risks.

Alternatives to Traditional Insurance for LLCs

While traditional insurance is ideal, some LLCs explore alternatives to manage risks:

- Self-insurance: Setting aside funds for potential claims (viable only for financially stable businesses).

- Captive insurance: Creating a subsidiary to underwrite the LLC’s risks (common in large enterprises).

- Industry risk pools: Joining group coverage programs tailored to specific sectors.

Frequently Asked Questions (FAQs)

What type of insurance is essential for a bookkeeper?

Professional Liability Insurance, also known as Errors and Omissions (E&O) Insurance, is critical for bookkeepers. This coverage protects against claims of negligence, mistakes, or oversights in your work that could lead to financial harm for clients. For example, if a client alleges that an error in your bookkeeping caused them tax penalties or lost revenue, this insurance can cover legal fees, settlements, or judgments. Additionally, General Liability Insurance is recommended to protect against third-party claims of bodily injury, property damage, or advertising injuries that might occur during business operations.

Why do bookkeepers need Professional Liability Insurance?

Bookkeepers handle sensitive financial data and complex transactions, making them vulnerable to disputes over accuracy. Professional Liability Insurance acts as a safety net if a client accuses you of errors, missed deadlines, or failure to deliver promised services. Even with meticulous work, misunderstandings or unrealistic client expectations can lead to lawsuits. This insurance ensures you’re not personally liable for legal costs or damages, safeguarding both your business finances and professional reputation.

Is Cyber Liability Insurance important for bookkeepers?

Yes, Cyber Liability Insurance is vital for bookkeepers, as they often store and manage clients’ financial information digitally. A data breach or cyberattack could expose sensitive data like bank accounts, tax IDs, or payroll details, leading to costly legal claims, regulatory fines, and reputational damage. This insurance covers expenses like forensic investigations, client notifications, credit monitoring services, and legal defense. Pairing it with strong cybersecurity practices (e.g., encryption, multi-factor authentication) further reduces risks.

Can a Business Owner’s Policy (BOP) benefit a bookkeeper?

A Business Owner’s Policy (BOP) combines General Liability Insurance and Commercial Property Insurance into one package, often at a discounted rate. For bookkeepers operating from a home office or rented space, this policy can cover equipment like computers, software, or office furniture against theft, fire, or vandalism. It also includes liability protection for client injuries on your premises. However, a BOP typically excludes Professional Liability or Cyber Liability coverage, so these may need to be added separately for comprehensive protection.

Leave a Reply

Our Recommended Articles