How Much is a Dj Business Insurance?

Starting a DJ business involves more than just talent and equipment; securing the right insurance is a critical step to safeguard your livelihood. The cost of DJ business insurance varies based on factors like coverage type, business size, location, and services offered. Basic liability policies might start as low as $300 annually, while comprehensive plans covering equipment, cancellations, or event-specific risks can exceed $1,000 per year. Understanding your unique needs—whether you’re a mobile DJ, event DJ, or studio owner—is key to balancing coverage and affordability. This article breaks down average costs, essential policy options, and tips to find tailored protection without breaking the bank.

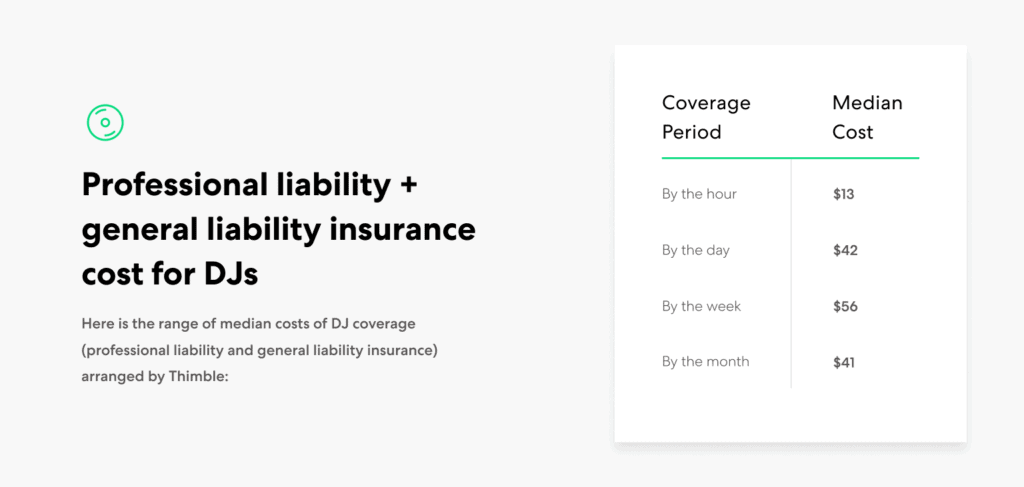

Understanding the Cost of DJ Business Insurance

The cost of DJ business insurance varies depending on factors like coverage type, business size, location, and risk factors. On average, annual premiums range from $500 to $2,000, but specialized coverage or high-risk events may increase costs. Policies often bundle general liability, equipment insurance, and professional liability to protect against lawsuits, equipment damage, or event cancellations. Always compare quotes and tailor coverage to your specific needs.

See AlsoVending Machine Business InsuranceFactors Influencing the Cost of DJ Business Insurance

The price of DJ insurance depends on coverage limits, business revenue, geographic area, and equipment value. For example, DJs working in high-risk venues or expensive urban areas may pay higher premiums. Additionally, claims history and event types (e.g., weddings vs. corporate events) impact costs.

| Factor | Impact on Cost |

|---|---|

| Coverage Type | Basic plans cost less; full coverage raises premiums |

| Business Size | More employees/staff = higher liability costs |

| Equipment Value | High-end gear requires pricier insurance |

| Location | Urban areas often cost more than rural |

Common Types of DJ Insurance Coverage

DJs typically need general liability insurance, equipment coverage, and professional liability. Some opt for event cancellation insurance or commercial auto insurance if transporting gear.

See AlsoDump Trailer Rental Business Insurance| Coverage Type | Details |

|---|---|

| General Liability | Covers injuries or property damage |

| Equipment Insurance | Protects gear from theft or damage |

| Professional Liability | Shields against client lawsuits |

| Event Cancellation | Refunds fees if events are canceled |

Average Insurance Costs for DJs

Most DJs pay $40–$150 monthly for basic coverage. High-limit policies or add-ons like cyber liability insurance can exceed $200/month.

| Coverage Level | Average Annual Cost |

|---|---|

| Basic Plan | $500–$1,000 |

| Mid-Tier Plan | $1,000–$1,500 |

| Comprehensive Plan | $1,500–$2,500+ |

To reduce costs, bundle policies, increase deductibles, or maintain a claims-free history. Insurers may offer discounts for safety certifications or annual payments.

See AlsoDoes Liability Insurance Cover Theft?| Strategy | Potential Savings |

|---|---|

| Policy Bundling | Save 10–20% |

| Higher Deductible | Lower monthly premiums |

| Safety Training | Qualify for discounts |

Top Insurance Providers for DJ Businesses

Providers like Thimble, Next Insurance, and Hiscox specialize in flexible DJ policies. Compare customizable plans and customer reviews before choosing.

| Provider | Key Features |

|---|---|

| Thimble | Pay-per-event coverage |

| Next Insurance | Affordable annual plans |

| Hiscox | High liability limits |

How much is insurance for DJs?

Factors Influencing DJ Insurance Costs

The cost of insurance for DJs depends on variables like coverage type, business size, and location. General liability insurance, equipment coverage, and event-specific policies are common options. Providers also consider your experience level, annual revenue, and risk exposure during events.

- Coverage Type: Basic liability plans start at $250/year, while comprehensive policies (including equipment) may exceed $1,000.

- Event Frequency: Full-time DJs pay more than part-time professionals due to higher exposure.

- Geographic Region: Urban areas often have higher premiums than rural locations due to liability risks.

Average Cost of DJ Insurance Policies

Most DJs pay between $300 and $800 annually for standard coverage. Temporary or per-event policies range from $50 to $200 per gig, depending on duration and attendee count.

See AlsoDog Walking Business Insurance- General Liability: Averages $350–$600/year, covering injuries or property damage.

- Equipment Insurance: Adds $100–$300/year to protect gear from theft or damage.

- Errors & Omissions: Costs $400–$700/year for coverage against contractual disputes.

Types of Coverage for DJs

DJ insurance typically includes liability, equipment protection, and business interruption policies. Specialty options like liquor liability may apply for events serving alcohol.

- General Liability: Essential for accidents causing bodily harm or venue damage.

- Inland Marine Insurance: Covers equipment during transport or storage.

- Non-Owned Auto Liability: Protects against risks when using rented vehicles.

How to Reduce DJ Insurance Expenses

Lower premiums by bundling policies, maintaining a clean claims history, and opting for higher deductibles. Comparing quotes from multiple providers also helps.

- Policy Bundling: Save 10–20% by combining liability and equipment coverage.

- Risk Management: Implement safety protocols to negotiate lower rates.

- Annual Payments: Paying upfront often costs less than monthly installments.

Insurance Providers for DJs

Specialized insurers like Thimble, Next Insurance, and MusicPro offer tailored DJ policies. Traditional providers like State Farm or Hiscox may also provide customizable plans.

- Thimble: Offers flexible per-event policies starting at $50.

- MusicPro: Focuses on musicians/DJs with equipment-heavy coverage.

- Next Insurance: Provides affordable annual plans for small DJ businesses.

What kind of insurance does a DJ need?

Why Do DJs Need Insurance?

DJs require insurance to protect against financial risks associated with their profession. Events can be unpredictable, and accidents like equipment damage, injuries to attendees, or last-minute cancellations may lead to costly claims. Insurance ensures DJs can operate confidently, knowing they’re covered for liabilities, equipment loss, or legal disputes.

- General Liability Insurance: Covers third-party injuries or property damage during events.

- Equipment Protection: Safeguards expensive gear like mixers, speakers, and laptops.

- Professional Liability: Shields against claims of negligence or failure to deliver services as promised.

What Does General Liability Insurance Cover for DJs?

General liability insurance is essential for DJs as it addresses risks tied to physical harm or property damage at events. For example, if a speaker falls and injures a guest or damages a venue’s flooring, this policy covers legal fees, medical costs, or repair expenses.

- Bodily Injury: Medical bills if a guest is hurt due to your equipment.

- Property Damage: Repairs for venues or client property you accidentally damage.

- Legal Defense: Coverage for lawsuits arising from covered incidents.

How Important Is Equipment Insurance for DJs?

DJs rely heavily on specialized, expensive gear, making equipment insurance critical. This policy covers theft, accidental damage, or malfunctions during transport or events. Without it, replacing gear out-of-pocket could be financially devastating.

- Theft Protection: Reimbursement for stolen equipment.

- Accidental Damage: Repairs or replacements for drops, spills, or electrical surges.

- Off-Site Coverage: Protection for gear while traveling or stored in vehicles.

What Is Professional Liability Insurance for DJs?

Also known as errors and omissions (E&O) insurance, this covers claims of professional mistakes, like failing to show up, playing incorrect music, or technical errors that ruin an event. It addresses legal costs and settlements if clients sue over unmet expectations.

- Breach of Contract: Claims due to unmet contractual obligations.

- Copyright Issues: Unintentional use of unlicensed music.

- Service Errors: Technical failures causing event disruptions.

Should DJs Consider Event Cancellation Insurance?

Event cancellation insurance reimburses clients if a DJ must cancel due to unforeseen circumstances, like illness, severe weather, or equipment failure. It builds trust with clients and ensures they aren’t left without entertainment.

- Illness or Injury: Coverage if the DJ cannot perform.

- Weather Disasters: Protection against cancellations due to storms or floods.

- Venue Issues: Compensation if the location becomes unusable.

Do you need insurance as a DJ?

Why Liability Insurance is Crucial for DJs

As a DJ, liability insurance protects you from financial risks if accidents occur during events. For example, if a guest trips over your cables or equipment, you could be held responsible for injuries or damages. A robust policy covers:

- Third-party injury claims arising from your setup or performance.

- Property damage caused by your gear at venues.

- Legal fees if a client or attendee files a lawsuit.

Protecting Your Equipment with Insurance

DJs rely on expensive gear, and equipment insurance safeguards against theft, damage, or malfunctions. Whether you’re traveling to gigs or performing outdoors, coverage ensures:

- Replacement costs for stolen or damaged equipment.

- Coverage during transit between events.

- Technical failures that could disrupt performances.

Event-Specific Risks and Insurance Needs

Different events pose unique challenges. Event-specific insurance addresses scenarios like cancellations, weather issues, or venue requirements. Key considerations include:

- Outdoor gigs vulnerable to weather-related cancellations.

- Venue demands for proof of insurance before booking.

- Non-refundable deposits lost due to emergencies.

Legal Requirements for DJs and Insurance

In many regions, insurance is legally mandated for professionals operating in public spaces. Failing to comply could result in fines or lost opportunities. Legal aspects involve:

- Local regulations requiring liability coverage.

- Contractual obligations with venues or event planners.

- Permit acquisition for large-scale events.

Cost vs. Benefit: Is DJ Insurance Worth It?

Weighing the cost of premiums against potential losses helps determine if insurance is worthwhile. Benefits often outweigh expenses due to:

- Low annual costs compared to out-of-pocket liability payments.

- Deductible flexibility tailored to your budget.

- Peace of mind knowing your business and gear are protected.

Frequently Asked Questions (FAQs)

What Factors Influence the Cost of DJ Business Insurance?

The cost of DJ business insurance depends on several variables, including coverage type, business size, and location. General liability insurance, which covers third-party injuries or property damage, typically ranges between $500 and $1,000 annually. However, adding specialized coverage like equipment protection or event cancellation insurance can increase premiums. Your claims history and the value of your gear also play a role—high-end equipment or a risky venue may raise costs. Always compare quotes from multiple providers to find the best rate.

What is the Average Cost of DJ Business Insurance?

Average annual premiums for DJ insurance typically fall between $500 and $1,500, depending on coverage scope. A basic general liability policy might cost $500–$800 per year, while comprehensive plans covering equipment damage, cyber liability, or non-owned auto liability can exceed $1,500. Seasonal DJs or part-time operators may pay less, whereas full-time professionals with high-risk gigs (e.g., weddings or large events) often face higher rates.

How Does Coverage Type Affect DJ Insurance Costs?

Insurance costs vary significantly based on the coverage types you select. For example, general liability insurance is usually the most affordable, while equipment insurance (covering theft or damage to gear) adds 20–30% to your premium. Adding errors and omissions (E&O) insurance for contractual disputes or event cancellation coverage can further increase costs. Bundling policies into a Business Owner’s Policy (BOP) often reduces expenses compared to purchasing standalone plans.

Yes, you can reduce premiums by bundling policies, raising deductibles, or maintaining a clean claims history. Opting for a pay-as-you-go plan (if you work irregularly) or investing in safety measures (e.g., equipment locks or fireproof cases) may also lower costs. Additionally, some insurers offer discounts for professional association memberships (e.g., NADJ or PDA). Always review your policy annually to eliminate unnecessary coverage and negotiate rates with your provider.

Leave a Reply

Our Recommended Articles