Does Liability Insurance Cover Theft?

Liability insurance is designed to protect individuals and businesses from financial losses resulting from claims of injury or damage to others. However, when it comes to theft, coverage under a standard liability policy is typically limited. Liability insurance generally does not cover theft of the policyholder’s own property, as it focuses on third-party claims rather than personal losses. Instead, protection against theft usually falls under property insurance, such as homeowners, renters, or commercial policies. Understanding these distinctions is critical for ensuring adequate coverage. This article explores the nuances of liability insurance, its limitations regarding theft, and alternative solutions to safeguard against stolen property.

Does Liability Insurance Cover Theft?

Liability insurance is designed to cover costs associated with damages or injuries you cause to others, not losses you personally incur. Theft of your property, or theft committed by someone else, is generally not covered under standard liability insurance policies. For theft-related incidents, you would typically need comprehensive coverage (for vehicles) or renters/homeowners insurance (for personal property). Always review your policy details or consult your insurance provider to confirm coverage specifics.

See AlsoCan You Get Business Insurance Without a Business LicenseWhat Does Liability Insurance Typically Cover?

Liability insurance focuses on third-party claims resulting from accidents, injuries, or property damage for which you are legally responsible. For example, if you accidentally cause a car accident, liability insurance covers the other party’s medical bills or vehicle repairs. It does not cover theft of your belongings or intentional criminal acts.

| Covered | Not Covered |

|---|---|

| Third-party injuries | Theft of your property |

| Property damage to others | Intentional criminal acts |

| Legal defense costs | Personal property loss |

When Is Theft Covered by Insurance?

Theft coverage depends on the type of insurance policy you hold. Comprehensive auto insurance covers theft of your vehicle or parts of it, while renters or homeowners insurance covers stolen personal items. Liability insurance alone will not reimburse you for stolen goods but may apply if you’re held liable for someone else’s theft-related losses.

See AlsoHow to Get Sponsors for a Team| Insurance Type | Theft Coverage |

|---|---|

| Comprehensive Auto | Vehicle theft, parts theft |

| Homeowners/Renters | Personal belongings theft |

| Liability Insurance | No direct theft coverage |

Liability vs. Comprehensive Insurance: Key Differences

Liability insurance and comprehensive insurance serve distinct purposes. Liability covers third-party harm, while comprehensive insurance protects against non-collision incidents, including theft, vandalism, or natural disasters. To safeguard against theft, combining liability with comprehensive or property-specific coverage is often necessary.

| Liability Insurance | Comprehensive Insurance |

|---|---|

| Covers others’ losses | Covers your own losses |

| Excludes theft | Includes theft |

| Mandatory for drivers | Optional add-on |

Can Liability Insurance Cover Theft by Another Party?

If someone accuses you of being responsible for their stolen property (e.g., due to negligence), your liability insurance might cover legal fees or settlements. For instance, if a guest’s belongings are stolen from your home due to your failure to secure the premises, liability coverage could apply. However, it won’t cover theft of your own items.

See AlsoWyoming LLC Annual Report| Scenario | Coverage Applicability |

|---|---|

| Your negligence causes theft | Possible liability coverage |

| Your property is stolen | No coverage |

Steps to Take If Theft Isn’t Covered by Liability Insurance

If your liability policy excludes theft, consider these steps:

1. Review your existing policies (e.g., comprehensive, homeowners) for theft coverage.

2. File a claim under the appropriate insurance type.

3. Document the theft with police reports and evidence.

4. Purchase additional coverage if needed.

| Action | Purpose |

|---|---|

| Review policies | Identify coverage gaps |

| File a claim | Seek reimbursement |

| Document theft | Support your case |

Is theft covered by general liability insurance?

What Does General Liability Insurance Typically Cover?

General liability insurance primarily covers third-party claims related to bodily injury, property damage, or advertising injuries. It is designed to protect businesses from legal and medical costs arising from accidents or negligence on their premises. Theft is generally not included in standard policies unless it directly relates to a covered peril. For example:

- Coverage applies if a customer’s property is damaged during a service.

- It does not cover stolen business assets or client belongings.

- Intentional criminal acts, like employee theft, are excluded.

Why Theft Is Often Excluded from General Liability Insurance

General liability insurance focuses on accidents and negligence, not intentional or criminal acts. Theft is typically excluded because:

See AlsoBiberk Business Insurance Reviews- It falls under crime insurance or commercial property insurance.

- Policies avoid covering deliberate illegal activities to prevent fraud.

- Claims involving theft require specialized coverage for evidence and investigation.

Alternative Insurance Policies That Cover Theft

To protect against theft, businesses should consider additional policies, such as:

- Commercial Property Insurance: Covers stolen inventory, equipment, or tools.

- Crime Insurance: Addresses employee theft, forgery, or fraud.

- Business Owner’s Policy (BOP): Bundles liability and property coverage, sometimes including theft.

General liability policies explicitly exclude theft-related scenarios, such as:

- Stolen cash, merchandise, or intellectual property.

- Theft by employees or contractors.

- Cyber theft or data breaches (requires cyber liability insurance).

Steps to Take if Theft Occurs at Your Business

If theft happens, follow these steps to mitigate losses and file claims:

- Document the incident with photos, videos, and police reports.

- Notify your insurer if you have a relevant policy (e.g., crime insurance).

- Review security measures to prevent future incidents.

What happens if your car is stolen and you still owe money?

Immediate Steps to Take When Your Financed Car Is Stolen

If your car is stolen and you still owe money on it, acting quickly is critical. Contact the police immediately to file a theft report, as this is required for insurance claims. Next, notify your lender and insurance company about the theft. Most auto loans require comprehensive insurance, which covers theft, so your insurer will investigate the claim.

- File a police report within 24 hours to document the theft.

- Inform your lender to discuss payment obligations during the investigation.

- Submit an insurance claim promptly to start the reimbursement process.

Continued Loan Obligations After Theft

Even if your car is stolen, you’re still legally obligated to repay the loan. Theft doesn’t absolve your debt. If your insurance payout covers the loan balance, the lender is paid first. If there’s a shortfall, you may need to cover the remaining amount.

- Loan payments continue until the insurance settles the claim.

- Check for gap insurance to cover the difference between the car’s value and the loan balance.

- Negotiate with the lender for potential payment deferrals during the process.

Insurance Coverage and Reimbursement Process

Comprehensive insurance typically covers theft, but reimbursement depends on the car’s depreciated value. The insurer will assess the vehicle’s market value at the time of theft, which may be less than the outstanding loan.

- Verify your coverage (comprehensive vs. liability-only).

- Prepare for a valuation dispute if the payout seems insufficient.

- Use gap insurance (if available) to bridge any financial gaps.

Legal and Financial Risks of Unresolved Theft

If the car isn’t recovered and insurance denies the claim, you’re still liable for the loan. Defaulting could damage your credit score, lead to repossession of other assets, or result in legal action.

- Monitor credit reports for loan-related impacts.

- Consult an attorney if insurance denies the claim unfairly.

- Explore refinancing options to manage remaining debt.

Long-Term Financial Impact and Recovery

A stolen car with an unpaid loan can strain finances long-term. Even after settling the insurance claim, you might face higher premiums or need a new down payment for another vehicle.

- Budget for potential out-of-pocket costs post-theft.

- Rebuild savings if the payout doesn’t cover the full loan.

- Review insurance policies to ensure better coverage for future loans.

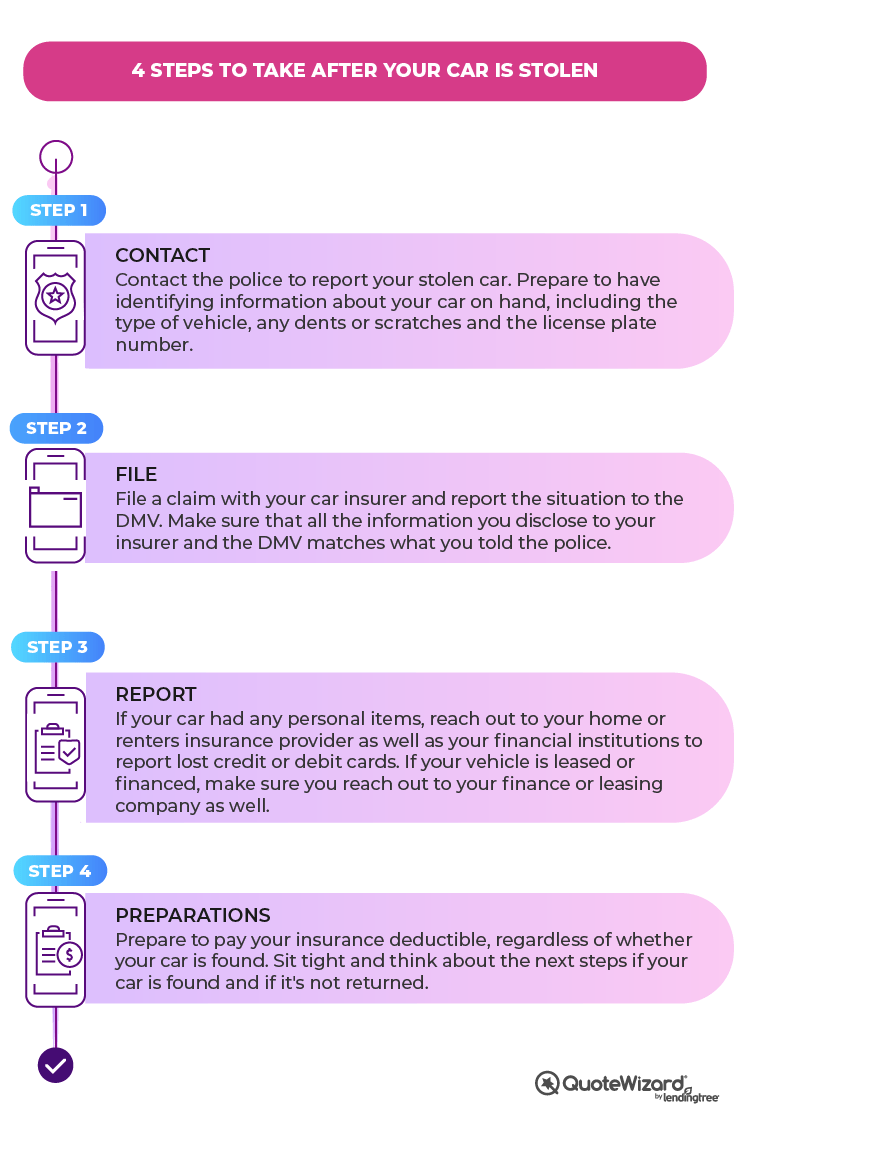

What are my rights after my car is stolen?

If your car is stolen, your first step should be to report the theft to the police immediately. Filing a police report is critical for insurance claims and potential recovery. Ensure you provide all necessary details, such as the vehicle’s make, model, license plate, and last-known location. Authorities may also use this information to track security camera footage or witnesses. Key actions include:

- Contact local law enforcement to file an official report.

- Share any GPS tracking data if your vehicle is equipped with such technology.

- Request a copy of the police report for insurance purposes.

Insurance Coverage and Claims Process

Your ability to recover financial losses depends on your insurance policy. Comprehensive coverage typically covers theft, but liability-only policies do not. Contact your insurer promptly to start the claims process. Steps to follow:

- Review your policy to confirm comprehensive coverage eligibility.

- Submit required documents, including the police report and proof of ownership.

- Cooperate with the insurer’s investigation, which may involve a waiting period for vehicle recovery.

Recovering a Stolen Vehicle

If your car is recovered, its condition determines your next steps. Authorities will notify you, and you may need to inspect the vehicle for damage or missing items. If repairs exceed the car’s value, the insurer may declare it a total loss. Important considerations:

- Arrange for towing and storage through your insurance if covered.

- Document any damage or missing property for additional claims.

- Update the police and insurer once the vehicle is recovered.

Legal Rights Against Thieves or Third Parties

You have the right to pursue legal action if the thief is identified or if a third party (e.g., a parking garage) is found negligent. Consult a lawyer to explore options like restitution or civil lawsuits. Key points:

- Work with prosecutors if criminal charges are filed to seek restitution.

- Investigate whether negligence by a third party contributed to the theft.

- Consider small claims court for uninsured losses, if applicable.

Rental Car and Transportation Reimbursement

Many insurance policies include rental car coverage to help with transportation while your claim is processed. Verify coverage limits and duration with your insurer. If not covered, you may need to pay out-of-pocket. Steps to take:

- Check your policy for rental reimbursement terms.

- Keep receipts for alternative transportation if seeking reimbursement.

- Notify the insurer if the recovery process delays your claim settlement.

Frequently Asked Questions (FAQs)

Does Liability Insurance Cover Theft of Personal Belongings?

Liability insurance generally does not cover theft of personal belongings. This type of insurance is designed to protect you financially if you are found legally responsible for causing bodily injury or property damage to others. For example, if someone slips and falls on your property, liability insurance may cover their medical bills. Theft-related losses, however, typically fall under policies like renters insurance, homeowners insurance, or commercial property insurance, depending on the context. Always review your policy details or consult your insurer to confirm coverage gaps.

What Type of Insurance Covers Theft of Business Equipment?

Commercial property insurance or a business owner’s policy (BOP) is usually required to cover theft of business equipment. Liability insurance alone will not reimburse stolen items, as it focuses on third-party claims. For instance, if a client’s property is damaged due to your negligence, liability insurance may respond. However, theft of your business assets requires separate coverage that specifically includes protection against burglary, vandalism, or robbery.

Can Liability Insurance Cover Theft Claims If Someone Sues Me?

Liability insurance may cover legal expenses if someone sues you for a covered peril, even if theft is involved. For example, if a visitor claims you failed to secure your property, leading to their belongings being stolen, your liability insurance might help pay for legal defense costs or settlements. However, it will not compensate for the stolen items themselves. The focus remains on third-party injury or damage claims, not direct reimbursement for theft losses.

Does Auto Liability Insurance Cover Theft of Items from My Car?

Auto liability insurance does not cover theft of personal items from your vehicle. This insurance only applies to damages or injuries you cause to others in an accident. To protect belongings stolen from your car, you would need comprehensive auto insurance (for the vehicle itself) or a homeowners/renters insurance policy (for items inside the car). Always report theft to the police and document losses for insurance claims.

Leave a Reply

Our Recommended Articles