Dog Walking Business Insurance

Starting a dog walking business offers rewarding opportunities, but it also comes with unique risks that require careful consideration. From accidental pet injuries to property damage or unexpected incidents during walks, unforeseen events can quickly escalate into costly liabilities. Dog walking business insurance provides essential protection, ensuring both your enterprise and clients are safeguarded against financial strain. Policies typically cover general liability, care custody and control, and equipment protection, addressing scenarios like veterinary bills, legal claims, or lost keys. Understanding the right coverage not only demonstrates professionalism but also builds client trust, allowing you to focus on delivering quality service while securing your business’s future.

- Understanding Dog Walking Business Insurance: Coverage and Importance

- What type of insurance do I need for dog walking?

- What is the best insurance for dog walking?

- How much do people charge for a 1 hour dog walk?

-

What is the best insurance for dog training a business?

- What Types of Insurance Are Essential for a Dog Training Business?

- Why Is Professional Liability Insurance Important for Dog Trainers?

- How Does Animal Bailee Coverage Protect Your Dog Training Business?

- What Role Does Commercial Auto Insurance Play for Mobile Dog Trainers?

- Should Dog Trainers Consider Business Interruption Insurance?

- Frequently Asked Questions (FAQs)

Understanding Dog Walking Business Insurance: Coverage and Importance

What Does Dog Walking Business Insurance Typically Cover?

Dog walking business insurance protects against risks associated with pet care services. Policies often include general liability insurance, covering injuries to third parties or property damage caused by a dog under your care. Care, custody, and control (CCC) coverage is critical, as it addresses veterinary costs if a pet is injured while in your custody. Some policies also offer bonding insurance to protect against theft accusations. Additionally, commercial auto insurance may be required if you transport pets.

See AlsoDoes Liability Insurance Cover Theft?| Coverage Type | Description |

|---|---|

| General Liability | Covers third-party injuries or property damage |

| CCC Coverage | Addresses pet injuries or accidents |

| Bonding Insurance | Protects against client theft claims |

| Commercial Auto | Required for business-related vehicle use |

Why Is Liability Insurance Crucial for Dog Walkers?

Liability insurance is essential because dog walkers face unpredictable risks, such as a dog biting a passerby or damaging property. Without coverage, legal fees and settlements could bankrupt a small business. Public liability insurance also builds client trust, showing professionalism and preparedness.

| Risk | Coverage Benefit |

|---|---|

| Dog bites | Medical and legal costs |

| Property damage | Repairs or replacements |

| Client lawsuits | Legal defense fees |

How Much Does Dog Walking Insurance Cost?

Costs vary based on factors like business size, services offered, and coverage limits. Basic liability insurance averages $300–$600 annually, while comprehensive plans with CCC and bonding may exceed $1,000. Providers also consider your claims history and location.

See AlsoDump Trailer Rental Business Insurance| Factor | Impact on Cost |

|---|---|

| Number of dogs | Higher volume = higher premiums |

| Coverage add-ons | Increases total cost |

| Business location | Urban areas often cost more |

What Are Common Exclusions in Dog Walking Insurance?

Most policies exclude pre-existing pet conditions, intentional misconduct, or off-premises incidents (e.g., walks in restricted areas). Pet illness unrelated to your care may also be excluded. Always review policy details to avoid coverage gaps.

| Exclusion | Example |

|---|---|

| Pre-existing conditions | Chronic illnesses diagnosed before coverage |

| Negligence | Failure to leash a dog as agreed |

| Unauthorized areas | Walking in prohibited parks |

How to Choose the Right Insurance Provider?

Select providers specializing in pet business insurance for tailored coverage. Compare policy limits, deductibles, and customer reviews. Verify the insurer’s financial stability through ratings agencies like A.M. Best.

See AlsoComputer Repair Business Insurance| Criteria | Consideration |

|---|---|

| Specialization | Experience with pet care businesses |

| Coverage flexibility | Customizable add-ons |

| Claim response time | Fast resolution processes |

What type of insurance do I need for dog walking?

What is General Liability Insurance for Dog Walkers?

General liability insurance is essential for dog walkers as it protects against claims related to third-party bodily injuries or property damage. For example, if a dog you’re walking damages a client’s property or injures a passerby, this coverage helps cover legal fees, medical bills, or repair costs. Key aspects include:

See AlsoWhat Licenses and or Permits Do I Need for a Mobile Mechanic Business?- Bodily injury coverage: Addresses medical expenses if someone is hurt due to your services.

- Property damage coverage: Covers repairs or replacements if a dog in your care damages others’ belongings.

- Legal defense costs: Helps pay for attorney fees if a lawsuit arises.

Why Do Dog Walkers Need Professional Liability Insurance?

Professional liability insurance (or errors and omissions insurance) protects against claims of negligence, mistakes, or failure to deliver promised services. For instance, if a client alleges you lost their pet or provided inadequate care, this policy covers related expenses. Key benefits include:

- Negligence claims: Shields against accusations of poor judgment or oversight.

- Breach of contract: Covers disputes over service agreements.

- Lost or stolen pets: May include compensation for recovery efforts.

Is Commercial Auto Insurance Necessary for Dog Walking?

If you use a vehicle for dog walking, commercial auto insurance is crucial. Personal auto policies often exclude business-related incidents. This coverage protects against accidents, pet injuries during transit, or vehicle damage. Key features:

- Accident coverage: Pays for repairs if your work vehicle is damaged.

- Pet injury protection: Covers veterinary bills if a dog is hurt during transport.

- Liability for third-party damage: Addresses costs if you cause an accident while working.

What is Bonding Insurance and Why Does It Matter?

Bonding insurance (a surety bond) builds client trust by covering theft or dishonesty claims. If a client accuses you of stealing property, the bond reimburses them up to a set amount. Key points:

- Theft protection: Compensates clients for stolen items.

- Client reassurance: Signals professionalism and reliability.

- Affordable coverage: Typically low-cost compared to other policies.

Should Dog Walkers Consider Workers’ Compensation Insurance?

If you hire employees, workers’ compensation insurance is often legally required. It covers medical bills and lost wages if an employee is injured on the job. Benefits include:

- Employee injury coverage: Pays for treatments and recovery costs.

- Legal compliance: Meets state requirements for businesses with staff.

- Lawsuit prevention: Reduces the risk of employee lawsuits over workplace injuries.

What is the best insurance for dog walking?

What Types of Insurance Are Essential for Dog Walkers?

Dog walkers should prioritize general liability insurance, which covers accidents like injuries to third parties or property damage. Additionally, care, custody, and control (CCC) coverage protects against incidents involving the dogs under their supervision. Bonding insurance is also valuable for safeguarding against theft accusations.

- General liability insurance: Covers legal fees and medical costs if a client or bystander is injured.

- Care, custody, and control coverage: Addresses vet bills if a dog is injured during a walk.

- Surety bonds: Builds trust by reimbursing clients for theft or property damage claims.

Why Do Dog Walkers Need Professional Liability Insurance?

Professional liability insurance, or errors and omissions (E&O) insurance, protects dog walkers against claims of negligence or mistakes in their services. For example, if a client alleges improper handling led to a lost pet, this coverage helps with legal defense and settlements.

- Legal protection: Covers lawsuits related to alleged negligence.

- Client disputes: Resolves conflicts over service quality or contractual misunderstandings.

- Reputation management: Mitigates financial risks from negative reviews or claims.

How Does Pet-Specific Insurance Benefit Dog Walkers?

Pet-specific insurance policies focus on risks unique to animal care, such as veterinary expenses for injured pets or coverage for breed-specific liabilities. This ensures walkers aren’t financially responsible for unexpected accidents.

- Veterinary coverage: Pays for treatments if a dog is hurt during a walk.

- Breed exclusions: Some policies cover breeds often excluded from standard plans.

- Lost pet recovery: Funds search efforts or rewards if a dog goes missing.

What Should Dog Walkers Look for in an Insurance Provider?

Choose providers offering customizable policies tailored to pet care services. Look for affordable premiums, clear coverage limits, and positive reviews from other pet professionals.

- Customizable coverage: Adjust policies to include walking, boarding, or grooming.

- Transparent pricing: Avoid hidden fees with clear premium structures.

- Industry experience: Prioritize insurers familiar with pet care risks.

Can Dog Walkers Rely on Business Owner’s Policies (BOP)?

A business owner’s policy (BOP) bundles general liability, property insurance, and business interruption coverage. It’s cost-effective for full-time walkers but may require add-ons for pet-specific risks.

- Cost efficiency: Combines multiple coverages at a lower rate.

- Property protection: Covers equipment like leashes or vehicles used for work.

- Gap coverage: May need supplemental CCC or pet injury policies.

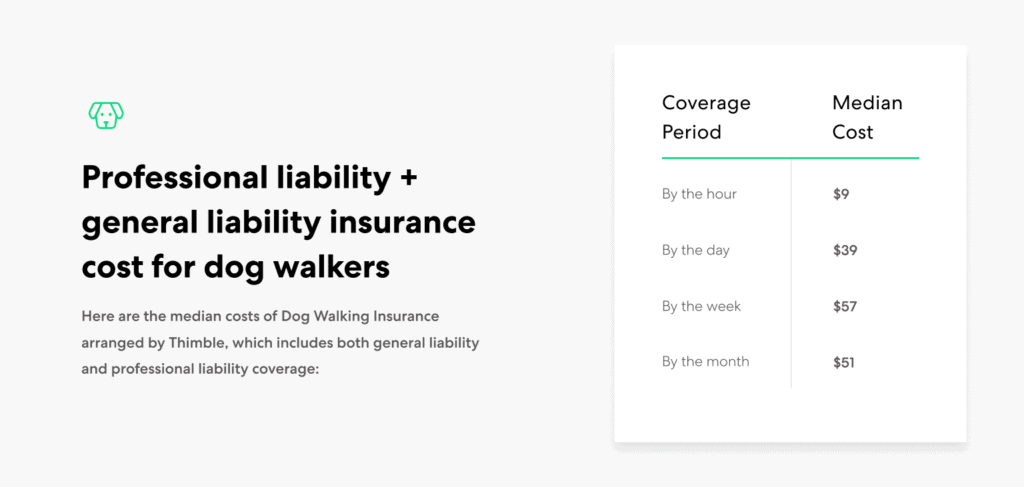

How much do people charge for a 1 hour dog walk?

Factors Influencing the Cost of a 1-Hour Dog Walk

The price of a 1-hour dog walk varies based on factors like location, walker experience, and additional services. Urban areas often charge more due to higher living costs, while rural regions may offer lower rates. Experienced walkers or those with certifications (e.g., pet first aid) typically command higher fees.

- Location: Rates range from $15–$25 in suburbs to $20–$35+ in cities like NYC or SF.

- Number of dogs: Adding a second dog may cost $5–$10 extra per hour.

- Special requests: Services like puppy care or medication administration increase costs.

Average Hourly Rates for Dog Walking Services

Most professional dog walkers charge between $15 and $30 per hour, depending on their qualifications and local demand. Independent walkers may offer lower rates ($15–$20), while agencies often charge $25–$30+ due to added insurance and vetting.

- Independent walkers: Typically $15–$25/hour.

- Agency walkers: $25–$35/hour with guaranteed backups.

- Subscription packages: Discounts for weekly/monthly bookings (e.g., 10% off recurring walks).

Additional Costs and Services in Dog Walking

Beyond basic walks, many providers offer add-ons like playtime, grooming, or training reinforcement. These extras can raise the total cost by $5–$15 per session.

- Extended play: $5–$10 extra for park visits or fetch sessions.

- Grooming: Brushing or paw cleaning for $8–$15.

- Emergency care: Fees for last-minute bookings (e.g., +$10–$20).

Regional Price Differences for Dog Walking

Geographic location heavily impacts rates. For example, major cities like Los Angeles or Boston average $25–$35/hour, while smaller towns may charge $12–$20. Seasonal demand (e.g., holidays) can also spike prices.

- High-cost cities: $30+ in areas with high pet ownership density.

- Mid-sized towns: $18–$25 for standard walks.

- Rural areas: As low as $12–$18 due to lower overhead.

How to Find Affordable Dog Walkers

To save money, compare prices on platforms like Rover or Wag, negotiate package deals, or hire part-time walkers (e.g., students). Always verify reviews and insurance coverage to ensure quality.

- Apps/platforms: Compare rates and read reviews transparently.

- Local referrals: Ask vet offices or pet stores for trusted walkers.

- Group walks: Split costs by joining neighborhood group walks ($10–$15/dog).

What is the best insurance for dog training a business?

What Types of Insurance Are Essential for a Dog Training Business?

For a dog training business, general liability insurance is critical to cover accidents like bites or property damage. Professional liability insurance (errors and omissions) protects against claims of negligence or inadequate training results. Additionally, commercial property insurance safeguards equipment and facilities.

- General Liability Insurance: Covers third-party injuries or property damage.

- Professional Liability Insurance: Addresses claims of negligence or failure to deliver promised services.

- Commercial Property Insurance: Protects business-owned equipment, tools, and physical locations.

Why Is Professional Liability Insurance Important for Dog Trainers?

Dog trainers face risks like dissatisfied clients or unintended behavioral issues in pets. Professional liability insurance shields against lawsuits alleging mistakes, poor advice, or unmet expectations. It also covers legal fees and settlements.

- Legal Defense Costs: Covers attorney fees and court expenses.

- Client Disputes: Addresses claims of ineffective training methods.

- Breach of Contract: Protects against allegations of failing to meet service agreements.

How Does Animal Bailee Coverage Protect Your Dog Training Business?

Animal bailee coverage is vital if you temporarily care for clients’ dogs. It covers veterinary costs, injuries, or loss of animals under your supervision. This policy is separate from general liability and ensures financial protection for incidents involving the pets.

- Veterinary Expenses: Pays for medical treatments if a dog is injured.

- Theft or Escape: Compensates for lost or stolen animals.

- Accidental Death: Provides coverage if a pet dies due to training-related incidents.

What Role Does Commercial Auto Insurance Play for Mobile Dog Trainers?

Mobile dog trainers using vehicles for services need commercial auto insurance. It covers accidents, vehicle damage, or injuries caused while transporting equipment or pets. Personal auto policies often exclude business-related incidents.

- Accident Coverage: Protects against collision costs during work-related travel.

- Equipment Protection: Covers damage to tools or crates in the vehicle.

- Third-Party Liability: Addresses injuries or property damage caused by your business vehicle.

Should Dog Trainers Consider Business Interruption Insurance?

Business interruption insurance helps recover lost income if operations halt due to disasters, like fire or natural events. It covers ongoing expenses (rent, salaries) and temporary relocation costs, ensuring financial stability during closures.

- Income Replacement: Compensates for lost revenue during downtime.

- Operating Expenses: Pays rent, utilities, and employee wages.

- Relocation Support: Covers costs of moving to a temporary workspace.

Frequently Asked Questions (FAQs)

What Types of Insurance Do Dog Walking Businesses Need?

Dog walking businesses typically require several types of insurance to mitigate risks. General liability insurance is essential to cover third-party injuries or property damage, such as a client tripping over a leash. Professional liability insurance (errors and omissions) protects against claims of negligence or mistakes in services. Additionally, care, custody, and control (CCC) coverage is critical, as it addresses injuries or illnesses to pets under your supervision. If you use a vehicle, commercial auto insurance may also be necessary to cover accidents during transportation.

Why Is General Liability Insurance Important for Dog Walkers?

General liability insurance is vital because it safeguards your business from common risks, such as a dog injuring a bystander or damaging a client’s property. For example, if a dog you’re walking knocks over a cyclist, this policy can cover medical expenses or legal fees. Without this coverage, your business could face devastating financial losses. It also enhances credibility, as many clients prefer working with insured professionals who demonstrate responsibility.

Does Dog Walking Insurance Cover Veterinary Expenses?

Coverage for veterinary expenses depends on your policy. Some insurers include care, custody, and control (CCC) coverage, which may cover vet bills if a pet is injured due to your negligence. However, pre-existing conditions or illnesses unrelated to your services are typically excluded. Always review your policy details and consider adding endorsements if needed. For comprehensive protection, discuss accidental injury coverage with your provider to ensure unexpected costs are addressed.

How Much Does Dog Walking Business Insurance Cost?

The cost of dog walking insurance varies based on factors like business size, location, and services offered. On average, basic policies range from $500 to $1,500 annually. General liability insurance may start as low as $300 per year, while adding CCC or commercial auto coverage increases premiums. Claims history and the number of employees also influence pricing. To get accurate quotes, provide insurers with details about your operations, and compare policies to balance affordability and coverage scope.

Leave a Reply

Our Recommended Articles