Is It Illegal to Not Have Business Insurance?

Operating a business without insurance can expose entrepreneurs to significant risks, but whether it’s outright illegal depends on various factors. Legal requirements for business insurance vary by jurisdiction, industry, and the type of coverage in question. In many regions, certain policies—like workers’ compensation for employees or commercial auto insurance for company vehicles—are legally mandated. Other forms, such as general liability or professional liability insurance, may not be compulsory by law but are often essential for compliance with contracts, licensing, or industry standards. Failing to secure required coverage can result in fines, penalties, or even business closure. Understanding local regulations and assessing operational risks is critical to avoiding legal and financial pitfalls.

Is It Illegal to Not Have Business Insurance?

The legality of operating a business without insurance depends on your location, industry, and business structure. In many jurisdictions, certain types of insurance, such as workers’ compensation or commercial auto insurance, are legally required. For example, most U.S. states mandate workers’ compensation for businesses with employees. However, other forms of insurance, like general liability insurance, may not be legally required but are often essential for risk management. Failing to carry legally mandated insurance can result in fines, penalties, or even business closure.

See AlsoCan You Get Business Insurance Without a Business LicenseLegal Requirements for Business Insurance by Industry

Certain industries face stricter insurance regulations. For instance, construction companies often need contractor’s liability insurance, while medical practices require malpractice insurance. Below is a table summarizing common industries and their typical insurance obligations:

| Industry | Required Insurance | Legal Source |

| Construction | Workers' Comp, Liability Insurance | State Labor Laws |

| Healthcare | Malpractice Insurance | State Medical Boards |

| Transportation | Commercial Auto Insurance | Federal Motor Carrier Laws |

Consequences of Operating Without Required Business Insurance

Failing to comply with insurance laws can lead to severe outcomes. Authorities may impose hefty fines, revoke business licenses, or pursue legal action. For example, operating without workers’ compensation insurance could result in civil lawsuits from injured employees.

See AlsoBuying a Book of Business Insurance| Consequence | Description |

| Fines | Monetary penalties per violation |

| License Suspension | Temporary or permanent loss of business rights |

| Personal Liability | Owners may face lawsuits |

Types of Business Insurance That Are Often Mandatory

While requirements vary, these policies are commonly required by law:

- Workers’ Compensation: For businesses with employees.

- Unemployment Insurance: Mandatory in most states.

- Commercial Auto Insurance: For company-owned vehicles.

| Insurance Type | Typical Requirement |

| Workers' Comp | Required in 49/50 U.S. states |

| Professional Liability | Required for licensed professionals |

How State Laws Influence Business Insurance Obligations

State regulations heavily dictate insurance requirements. For example, California requires disability insurance, while Texas does not mandate workers’ comp for all industries. Always check local statutes to ensure compliance.

See AlsoHow to Get a Loan From Usa to Start a Small Business?| State | Unique Requirement |

| California | Disability Insurance |

| Florida | Windstorm Coverage (for coastal areas) |

Risks of Skipping Business Insurance Even If Not Legally Required

Opting out of non-mandatory insurance, like general liability, exposes businesses to financial ruin from lawsuits or property damage. Clients may also require proof of insurance for contracts.

| Risk | Impact |

| Lawsuits | High legal defense costs |

| Property Damage | Out-of-pocket repair expenses |

What happens if there is no business insurance?

Legal and Financial Liability Exposure

Without business insurance, companies face unprotected legal and financial risks. Lawsuits from customers, vendors, or employees can lead to crippling expenses, as there is no coverage for legal fees or settlements. For example:

- Legal fees from disputes or negligence claims must be paid out-of-pocket.

- Court-ordered settlements or damages could bankrupt the business.

- Personal assets of owners may be at risk if corporate structures are pierced.

Property and Asset Vulnerability

A lack of property insurance leaves physical assets exposed to unforeseen events. Damage from fires, natural disasters, or theft could result in irreplaceable losses. Key risks include:

See AlsoIllinois LLC Filing Fee- No coverage for repairs or replacements of damaged equipment, inventory, or buildings.

- Business operations may halt indefinitely due to unaffordable recovery costs.

- Lost income during downtime cannot be compensated without business interruption coverage.

Operating without workers’ compensation or employment practices liability insurance exposes businesses to employee-driven claims. Consequences include:

- Medical costs and lost wages for workplace injuries must be paid by the employer.

- Lawsuits over discrimination, harassment, or wrongful termination lack financial protection.

- Difficulty attracting talent due to inadequate employee benefits or safety assurances.

Business Interruption Costs

Unexpected disruptions, such as natural disasters or supply chain failures, can devastate uninsured businesses. Issues include:

- No financial support to cover ongoing expenses like rent or salaries during closures.

- Permanent closure if recovery funds are unavailable.

- Lost customers due to prolonged service interruptions.

Loss of Client Trust and Reputation

Clients and partners often require proof of insurance for contracts. Without it:

- Missed opportunities as clients opt for insured competitors.

- Damaged reputation if the business cannot fulfill obligations after a crisis.

- Negative publicity from lawsuits or unpaid claims may harm brand credibility.

Can I operate an LLC without insurance?

Is It Legal to Operate an LLC Without Insurance?

While operating an LLC without insurance is generally legal in many jurisdictions, specific requirements depend on state laws and industry regulations. For example, certain industries like construction or healthcare may legally mandate insurance. However, even if not required, lacking coverage exposes the LLC to risks.

- Check state-specific regulations for LLC insurance requirements.

- Review industry standards that may impose mandatory coverage.

- Consult a legal advisor to ensure compliance with local laws.

What Risks Come With Operating an LLC Without Insurance?

Operating without insurance leaves the LLC and its owners vulnerable to financial liabilities, lawsuits, and operational disruptions. Without coverage, personal assets could be at risk if the business faces legal claims.

- Personal liability if the LLC’s assets cannot cover damages.

- Legal penalties in regulated industries requiring insurance.

- Loss of business opportunities as clients may require proof of insurance.

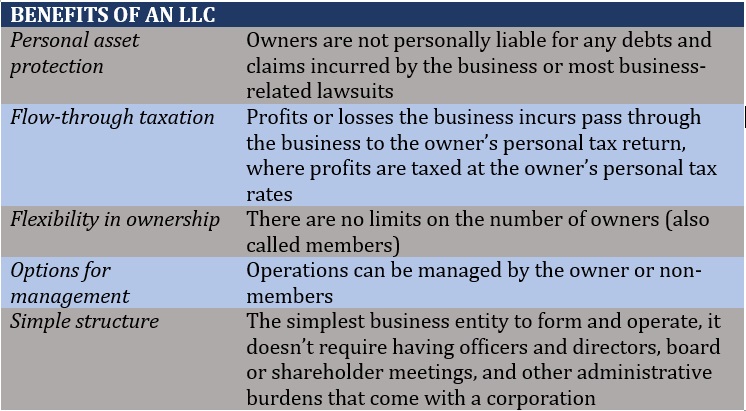

What Types of Insurance Are Recommended for an LLC?

Even if not legally required, certain insurance types mitigate risks for LLCs. General liability insurance and professional liability coverage are common safeguards.

- General Liability Insurance: Covers bodily injury or property damage claims.

- Professional Liability Insurance: Protects against negligence or errors in services.

- Workers’ Compensation: Mandatory in most states if the LLC has employees.

Can Clients or Contracts Require an LLC to Have Insurance?

Many clients, vendors, or partners may require an LLC to carry specific insurance policies as part of contractual agreements. Operating without insurance could limit business relationships.

- Contractual obligations often include insurance clauses.

- Industry certifications may demand proof of coverage.

- Lease agreements for commercial spaces frequently require liability insurance.

How Does Insurance Protect an LLC’s Limited Liability Status?

Insurance helps preserve the limited liability protection of an LLC by covering claims that could otherwise pierce the corporate veil and target owners’ personal assets.

- Shields personal assets from business-related lawsuits.

- Demonstrates compliance with legal and financial responsibilities.

- Reduces out-of-pocket costs for legal fees or settlements.

Is it required to have business insurance?

Whether business insurance is required depends on your location, industry, and specific business activities. In many jurisdictions, certain types of insurance, like workers’ compensation (for employees) or commercial auto insurance (for company vehicles), are legally mandated. Other policies, such as general liability or professional liability insurance, may be optional but are often required by clients, landlords, or lenders. Even when not legally required, insurance protects against financial risks like lawsuits, property damage, or business interruptions.

Legal Requirements for Business Insurance

Business insurance is sometimes legally required depending on your operations. For example:

- Workers’ compensation insurance is mandatory in most states if you have employees.

- Professional liability insurance may be required for licensed professions like healthcare or law in certain jurisdictions.

- Commercial auto insurance is legally required if your business uses vehicles.

Industry-Specific Insurance Needs

Industry risks often dictate insurance requirements. For instance:

- Construction businesses typically need contractor’s liability insurance to cover worksite accidents.

- Healthcare providers require malpractice insurance to protect against patient lawsuits.

- Retail stores often need product liability insurance for defective goods claims.

Contractual Obligations and Insurance

Clients, landlords, or partners may require proof of insurance. Examples include:

- Lease agreements demanding property insurance for rented office spaces.

- Client contracts stipulating general liability insurance to cover third-party injuries.

- Lenders requiring business interruption insurance as a loan condition.

Financial Protection Through Insurance

Even if not legally required, insurance safeguards finances:

- Liability claims from lawsuits can devastate uninsured businesses.

- Property damage from fires or natural disasters may lead to costly repairs.

- Data breaches often necessitate cybersecurity insurance to cover recovery expenses.

Consequences of Skipping Business Insurance

Operating without insurance risks severe outcomes:

- Legal penalties for non-compliance with mandatory policies like workers’ comp.

- Loss of contracts if clients require proof of coverage.

- Personal asset exposure if a lawsuit targets unprotected business finances.

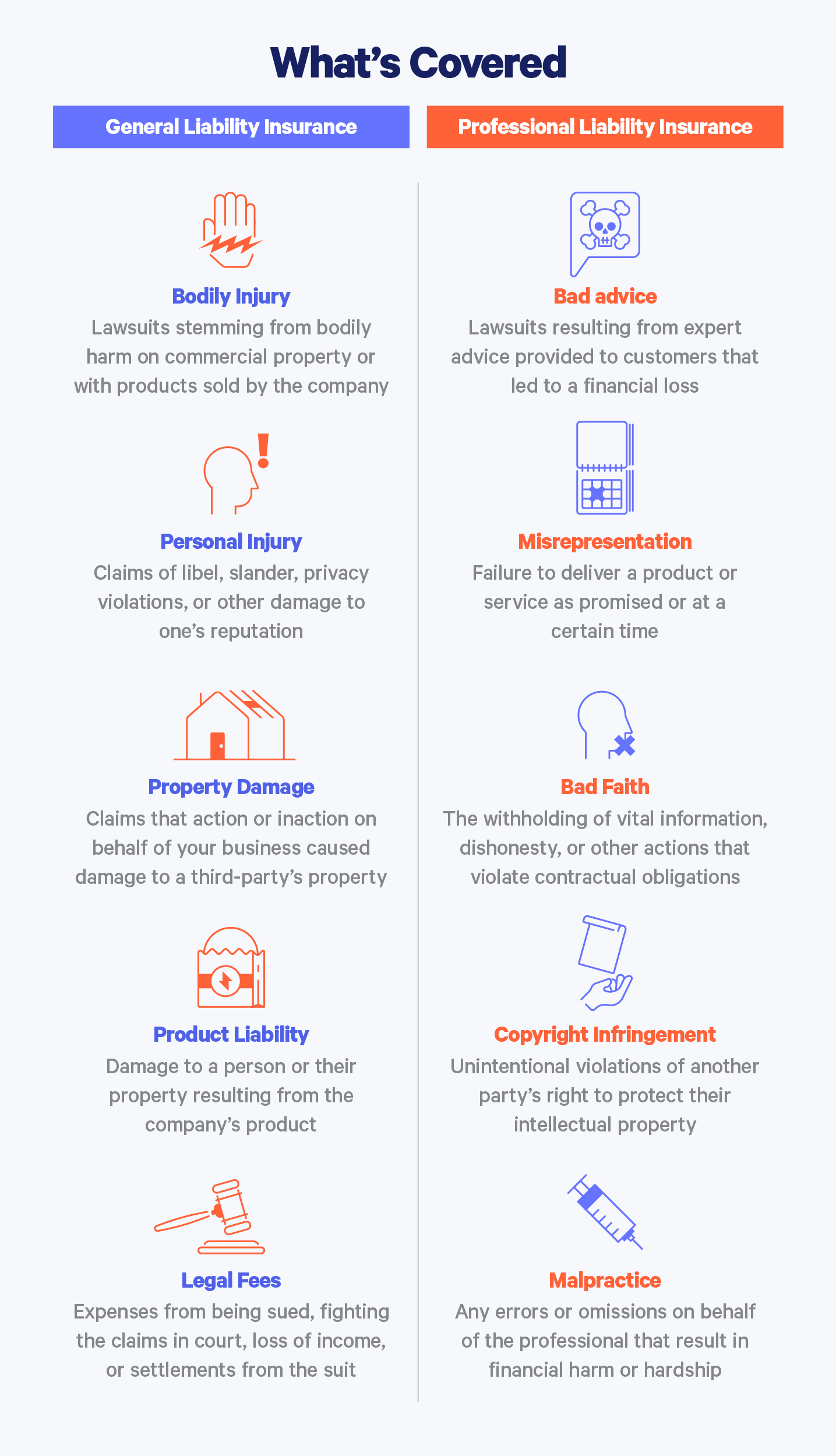

What happens if you don't have professional liability insurance?

Financial Risks of Not Having Professional Liability Insurance

Without professional liability insurance, you assume full responsibility for any financial losses stemming from claims of negligence, errors, or omissions in your work. This includes covering legal fees, settlements, or court-ordered damages out of pocket. For example:

- Legal defense costs can escalate quickly, even if the claim is unfounded.

- You may face bankruptcy if required to pay substantial settlements.

- Business savings or personal assets might be liquidated to cover expenses.

Legal Consequences for Uninsured Professionals

Professionals without liability coverage risk legal action from clients or third parties. Lawsuits can lead to prolonged court battles and judgments that permanently harm your career. Key risks include:

- Subpoenas and litigation demand time and resources, disrupting workflow.

- Judgments may result in wage garnishment or asset seizure.

- Lack of insurance weakens your ability to negotiate settlements.

Damage to Professional Reputation

A lack of insurance can erode client trust and damage your professional credibility. Clients may perceive you as unprepared for risks, leading to lost opportunities. For instance:

- Negative publicity from lawsuits can tarnish your brand.

- Clients may prefer competitors with verified coverage.

- Rebuilding trust after a legal dispute becomes exponentially harder.

Loss of Client Contracts and Opportunities

Many clients require proof of professional liability insurance before signing contracts. Without it, you may lose bids or partnerships. Consequences include:

- Exclusion from high-value projects with strict insurance requirements.

- Inability to work with government agencies or large corporations.

- Renegotiation of existing contracts to remove uninsured parties.

Personal Asset Vulnerability in Lawsuits

Without insurance, your personal assets—such as savings, property, or investments—are at risk if a lawsuit exceeds business funds. Key exposures include:

- Home equity or vehicles could be seized to pay legal judgments.

- Retirement accounts or personal bank accounts may be targeted.

- Jointly owned assets might also be subject to claims.

Frequently Asked Questions (FAQs)

Is It Illegal to Operate a Business Without Insurance?

Whether it’s illegal to operate without business insurance depends on your location, industry, and specific legal requirements. In many jurisdictions, certain types of insurance, such as workers’ compensation for businesses with employees or commercial auto insurance for company vehicles, are legally mandatory. For example, most U.S. states require businesses with employees to carry workers’ compensation. However, other forms of insurance, like general liability or professional liability insurance, may not be legally required but are often critical for risk management. Always consult local laws and industry regulations to ensure compliance.

What Are the Consequences of Not Having Required Business Insurance?

Failing to carry legally mandated business insurance can result in severe penalties. Consequences may include fines, license suspensions, or even legal action against the business owner. For instance, operating without workers’ compensation insurance could lead to lawsuits from injured employees and state-imposed fines. Additionally, lacking insurance might void contracts with clients or partners who require proof of coverage. In extreme cases, repeated violations could force a business to shut down.

Are There Specific Industries Where Business Insurance Is Legally Required?

Yes, certain industries are subject to stricter insurance requirements due to higher risks. For example, construction companies often need contractor’s liability insurance, while medical practices must carry malpractice insurance. Transportation businesses typically require commercial auto insurance, and manufacturing firms might need product liability coverage. These mandates vary by region, so businesses must research both federal and state-level regulations. Non-compliance can lead to operational restrictions or loss of licensure.

Can a Business Legally Operate Without Insurance If It Has No Employees?

In some cases, businesses without employees may avoid certain insurance requirements, but not all. For example, sole proprietorships without staff might not need workers’ compensation in some states. However, other policies, like professional liability insurance or commercial property insurance, could still be legally necessary depending on the business activities. Additionally, clients or landlords might require proof of insurance, making it practically essential even if not legally mandated. Always verify local laws and contractual obligations.

Leave a Reply

Our Recommended Articles