Pressure Washing Business Insurance

Operating a pressure washing business involves managing various risks, from accidental property damage to potential injuries. Whether you’re cleaning residential driveways, commercial facades, or industrial equipment, unforeseen incidents can lead to costly claims or legal disputes. This is where pressure washing business insurance becomes essential. Tailored coverage options help protect your equipment, employees, and clients while ensuring compliance with industry regulations and client contracts. Understanding the types of insurance available—such as general liability, commercial auto, and equipment breakdown policies—can safeguard your company’s financial stability and reputation. This article explores key insurance considerations for pressure washing professionals, offering insights to make informed decisions for long-term success.

Why Pressure Washing Business Insurance is Essential for Protecting Your Company

Types of Insurance Coverage for Pressure Washing Businesses

Pressure washing businesses require specialized insurance to mitigate risks. General liability insurance covers third-party injuries or property damage, while commercial auto insurance protects company vehicles. Equipment insurance safeguards tools like pressure washers from theft or damage. Workers’ compensation is mandatory in most states if you have employees, covering medical costs from job-related injuries. Pollution liability insurance addresses chemical runoff risks.

See AlsoDump Trailer Rental Business Insurance| Coverage Type | Key Features |

|---|---|

| General Liability | Covers third-party injuries, property damage, and legal fees |

| Commercial Auto | Protects company vehicles and drivers |

| Equipment Insurance | Replaces or repairs stolen/damaged tools |

| Workers’ Compensation | Medical coverage for employee injuries |

| Pollution Liability | Addresses environmental damage claims |

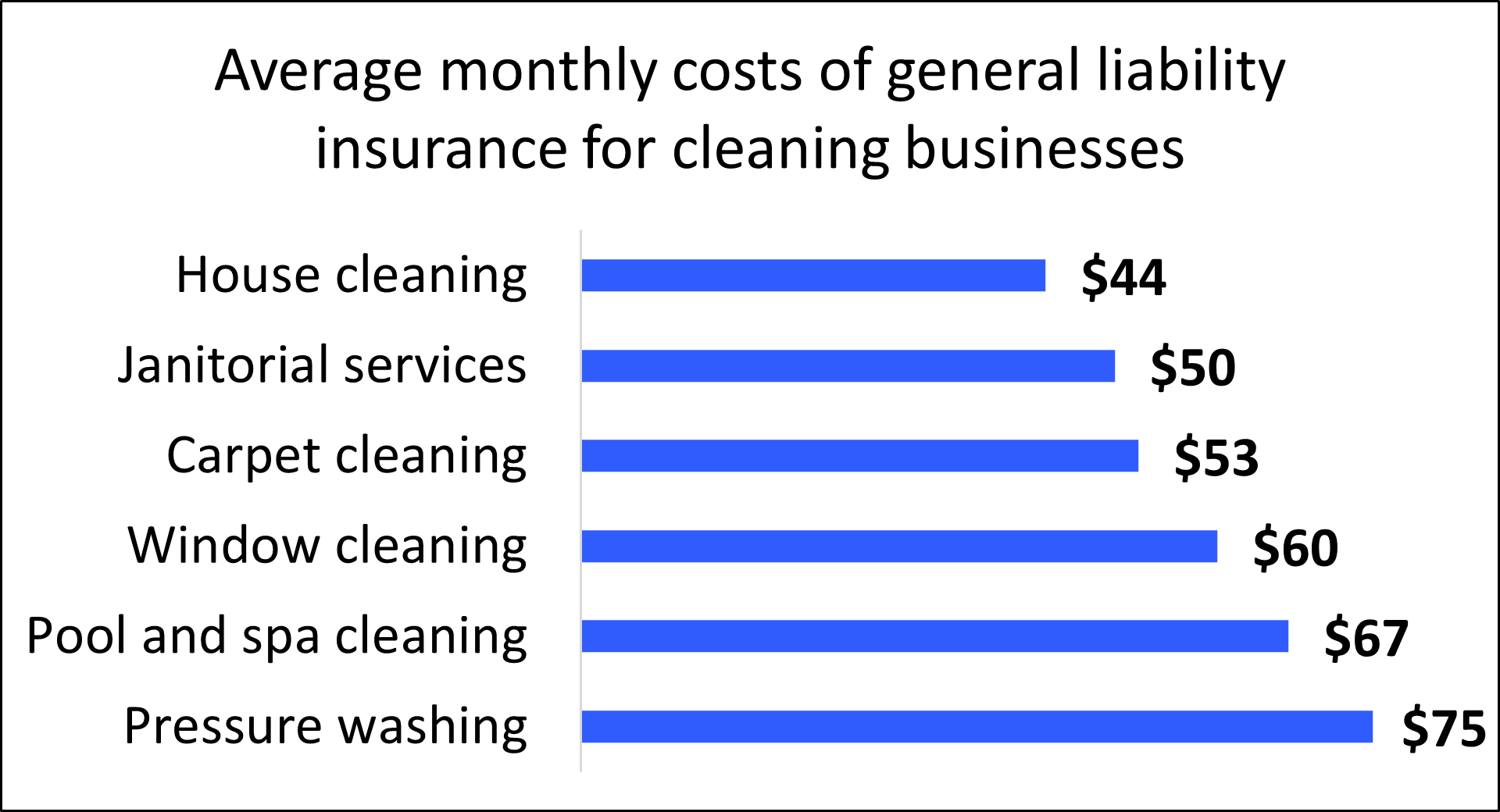

How Much Does Pressure Washing Insurance Cost?

Insurance costs vary based on business size, coverage limits, and location. A small pressure washing business might pay $500–$1,500 annually for general liability. Adding commercial auto or equipment insurance raises premiums. High-risk areas (e.g., coastal regions) may increase costs due to weather-related risks. Deductibles and claims history also impact pricing.

| Factor | Impact on Cost |

|---|---|

| Business Size | Larger teams = higher premiums |

| Coverage Limits | Higher limits = higher costs |

| Location | High-risk areas increase prices |

| Claims History | Past claims may raise premiums |

| Deductibles | Lower deductibles = higher premiums |

Legal Requirements for Pressure Washing Insurance

Most states require workers’ compensation if you have employees. Clients often demand certificates of insurance (COIs) before hiring. Local permits may require general liability coverage. Failure to comply risks fines, lawsuits, or business closure.

See AlsoVending Machine Business Insurance| Requirement | Details |

|---|---|

| Workers’ Comp | Mandatory for businesses with employees |

| Client Contracts | COIs often required for projects |

| Licensing | Some states tie licenses to insurance |

| Employee Coverage | Required for full-time/part-time staff |

| Environmental Laws | Pollution liability may be required |

How to Choose the Right Insurance Provider

Select providers experienced in commercial cleaning or contractor insurance. Compare quotes for coverage breadth and exclusions. Check reviews for claim responsiveness. Bundling policies (e.g., BOPs) can save costs. Verify the provider’s financial stability via ratings like A.M. Best.

| Consideration | Details |

|---|---|

| Industry Expertise | Look for contractors’ insurance specialists |

| Coverage Options | Ensure policies match business risks |

| Financial Stability | Check insurer ratings (e.g., A.M. Best) |

| Customer Support | 24/7 claims support is critical |

| Cost vs. Value | Balance affordability with coverage quality |

Common Claims Filed by Pressure Washing Businesses

Frequent claims include property damage (e.g., broken windows), slip-and-fall accidents, and equipment theft. Chemical damage to landscapes or water systems also triggers claims. Without insurance, these incidents lead to out-of-pocket expenses or lawsuits.

See AlsoWhat Licenses and or Permits Do I Need for a Mobile Mechanic Business?| Claim Type | Examples |

|---|---|

| Property Damage | Damaged siding, broken surfaces |

| Bodily Injury | Slip-and-fall accidents on wet surfaces |

| Equipment Loss | Theft of pressure washers or hoses |

| Pollution | Chemical runoff harming ecosystems |

| Vehicle Accidents | Collisions involving company trucks |

What permits do you need for a pressure washing business?

Business License Requirements for Pressure Washing

Starting a pressure washing business typically requires a general business license issued by your local city or county government. This license ensures your operations comply with local regulations. Requirements may vary based on your location, but common steps include:

See AlsoIs Allstate Business Insurance Legit?- Submitting an application with your business name and structure (e.g., LLC, sole proprietorship).

- Paying a licensing fee, which varies by jurisdiction.

- Renewing the license annually or biennially, depending on local rules.

Environmental Permits and Water Usage Regulations

Pressure washing often involves water runoff, which may require environmental permits to prevent contamination. Key considerations include:

- Obtaining a National Pollutant Discharge Elimination System (NPDES) permit if wastewater enters storm drains.

- Complying with local water reclamation or recycling laws to reduce environmental impact.

- Adhering to EPA guidelines for using chemicals in cleaning solutions.

Contractor’s License for Specialized Services

Some states or municipalities require a contractor’s license for pressure washing, especially if services include structural work. Requirements often involve:

See AlsoDog Walking Business Insurance- Passing a trade exam or proving industry experience.

- Securing a surety bond to protect clients against incomplete work.

- Providing proof of liability insurance coverage.

Zoning Permits for Home-Based Businesses

If operating from home, check local zoning laws to ensure compliance. Steps may include:

- Applying for a home occupation permit to legally run the business from your residence.

- Ensuring your property is zoned for commercial activity.

- Limiting signage or client visits to avoid violating residential zoning rules.

Sales Tax Permit and State Registration

Most states require a sales tax permit if you charge customers tax. Key steps include:

- Registering your business with the state’s Department of Revenue.

- Collecting and remitting sales tax on applicable services.

- Keeping detailed records of transactions for audits.

Do you need insurance to power wash?

Is Insurance Legally Required for Power Washing Services?

While insurance is not universally mandated by law for power washing, certain situations or jurisdictions may require it. For example, if you operate as a licensed contractor, many states or local governments may stipulate liability insurance as part of licensing requirements. Additionally, working on commercial properties or government contracts often necessitates proof of insurance.

- Check local regulations to confirm if insurance is legally required in your area.

- Licensing boards may tie insurance to business permits for professional power washing services.

- Commercial clients often require contractors to carry insurance to mitigate risks.

Why Do Clients Often Demand Insured Power Washing Services?

Clients, especially businesses and property managers, prioritize hiring insured power washing providers to avoid financial liability for accidents. Without insurance, clients risk bearing costs for property damage or injuries.

- Property damage claims (e.g., broken windows or eroded surfaces) could lead to lawsuits.

- Injury liability (e.g., slips from water runoff or equipment mishaps) may result in medical expenses.

- Contractual obligations in leases or property agreements often require third-party vendors to be insured.

What Types of Insurance Are Essential for Power Washing?

Power washing businesses should consider general liability insurance as a baseline, but other policies may apply depending on operations.

- General liability insurance: Covers third-party property damage or bodily injury.

- Commercial auto insurance: Protects company vehicles transporting equipment.

- Workers’ compensation: Required if employing staff, covering work-related injuries.

What Are the Risks of Power Washing Without Insurance?

Operating without insurance exposes you to significant financial and legal risks. Even minor accidents can lead to costly claims.

- Out-of-pocket expenses for repairs or medical bills if sued.

- Loss of business reputation if unable to cover damages.

- Legal penalties if operating without required insurance in regulated areas.

How to Choose the Right Insurance Policy for Power Washing?

Selecting insurance involves assessing coverage scope, deductibles, and provider reliability.

- Evaluate risks: Consider common hazards in power washing, like water damage or chemical use.

- Compare quotes from insurers specializing in contractor or cleaning services.

- Review policy exclusions to ensure coverage aligns with your services (e.g., roof cleaning or graffiti removal).

How much does a cleaning business insurance cost?

Factors Influencing Cleaning Business Insurance Costs

The cost of cleaning business insurance depends on variables like coverage type, business size, location, and risk exposure. For example, a solo operator may pay less than a company with multiple employees. Key factors include:

- Coverage scope: Basic liability insurance is cheaper than comprehensive plans.

- Number of employees: More staff increases workers' compensation premiums.

- Claims history: Past incidents may raise costs by 10–25%.

Types of Coverage and Their Costs

Common policies include general liability, workers' compensation, and commercial auto insurance. Average annual costs vary:

- General liability: $500–$1,500 per year.

- Workers' compensation: $800–$3,500 per employee annually.

- Commercial auto insurance: $1,200–$2,400 per vehicle.

Average Cost Range for Cleaning Business Insurance

Most small cleaning businesses spend $500–$5,000 annually on insurance. Costs scale with:

- Business revenue: Higher income may require increased coverage limits.

- Service types: Hazardous cleaning (e.g., biohazards) raises premiums.

- Policy add-ons: Bonding or equipment coverage adds $200–$1,000 yearly.

Reducing costs involves risk management and policy optimization. Strategies include:

- Bundling policies: Multi-policy discounts save 10–20%.

- Safety training: Certifications may lower workers' comp rates.

- Higher deductibles: Opting for $1,000+ deductibles reduces premiums.

State-Specific Insurance Cost Variations

Premiums vary by state regulations and local risk factors. Examples:

- High-cost states: California or New York due to strict liability laws.

- Low-cost states: Idaho or South Dakota with fewer claims.

- Weather risks: Coastal areas may pay more for flood-related coverage.

How do you bill for pressure washing?

How Do You Determine the Cost of Pressure Washing Services?

Pressure washing billing depends on factors like project size, surface type, and complexity. Most professionals use a combination of square footage, time estimates, and equipment requirements to calculate costs. For example:

- Square footage pricing: Charging per square foot for large, uniform areas like driveways.

- Hourly rates: Used for smaller or unpredictable jobs, such as removing graffiti.

- Flat fees: Common for standard services like house washing, with adjustments for unique challenges.

What Factors Influence Pressure Washing Pricing?

Several variables impact the final price, including surface material, dirt severity, and accessibility. Providers may adjust rates based on:

- Surface type: Delicate materials (e.g., wood) require lower pressure, increasing labor time.

- Stain intensity: Oil or mold removal often needs specialized cleaners or repeated passes.

- Obstacles: Tight spaces or high walls may demand extra equipment or safety measures.

Is Square Footage the Best Way to Bill for Pressure Washing?

While square footage is popular, it’s not always ideal. This method works well for open, even surfaces but can undervalue complex jobs. Alternatives include:

- Tiered pricing: Base rate + surcharges for obstacles or steep terrain.

- Project-based quotes: Flat fees tailored to specific client needs.

- Hybrid models: Combining square footage with hourly rates for irregular layouts.

How Do Additional Services Affect Pressure Washing Bills?

Upsells like stain treatment, sealing, or gutter cleaning can increase total costs. Common add-ons include:

- Pre-treatment: Applying detergents to break down grime.

- Post-cleaning sealing: Protecting surfaces from future stains.

- Debris removal: Hauling away leaves or dirt post-wash.

Do Pressure Washing Companies Offer Discounts or Packages?

Many providers incentivize repeat business with seasonal discounts or maintenance plans. Examples include:

- Bundled services: Discounts for combining house and driveway washing.

- Subscription plans: Reduced rates for quarterly or annual cleanings.

- Off-peak pricing: Lower costs during slower seasons (e.g., winter).

Frequently Asked Questions (FAQs)

What Types of Insurance Do Pressure Washing Businesses Need?

Pressure washing businesses typically require several key insurance policies to mitigate risks. General Liability Insurance is essential to cover third-party bodily injuries, property damage, or advertising injuries. Commercial Auto Insurance protects vehicles used for business operations, while Equipment Coverage safeguards tools and machinery like pressure washers. If you have employees, Workers’ Compensation Insurance is legally mandated in most states to cover workplace injuries. Additionally, Professional Liability Insurance (Errors & Omissions) can defend against claims of inadequate workmanship or negligence.

How Much Does Pressure Washing Business Insurance Cost?

The cost of insurance for a pressure washing business varies based on factors like revenue, number of employees, and coverage limits. On average, General Liability Insurance may cost between $500 and $1,500 annually, while Commercial Auto Insurance ranges from $1,000 to $2,500 per vehicle. Workers’ Compensation premiums depend on payroll size and risk exposure, often starting at $1,000 per year. Bundling policies into a Business Owner’s Policy (BOP) can reduce costs by up to 20%. Always compare quotes from multiple providers to secure competitive rates.

Does Pressure Washing Insurance Cover Water Damage Claims?

Standard General Liability Insurance may cover accidental water damage to a client’s property if caused by your services. However, policies often exclude gradual damage (e.g., mold from lingering moisture) or negligence, such as using excessive pressure that cracks surfaces. To address gaps, consider adding Pollution Liability Insurance, which covers environmental harm from chemical cleaners or wastewater runoff. Review your policy’s exclusions and endorsements carefully and discuss specific risks with your insurer to ensure adequate protection.

Is Insurance Required for Pressure Washing Contractors?

While insurance is not federally mandated, most states require Workers’ Compensation if you have employees. Clients, especially commercial ones, often demand proof of General Liability Insurance before signing contracts. Additionally, leasing companies or lenders may require Equipment and Auto Insurance for financed assets. Operating uninsured exposes your business to lawsuits, repair costs, and potential bankruptcy. Even solo operators should prioritize liability coverage to protect against unforeseen accidents that could jeopardize their financial stability.

Leave a Reply

Our Recommended Articles