Starting a Car Rental Business Insurance

Starting a car rental business requires careful planning, and securing the right insurance coverage is a critical step in safeguarding your investment. As vehicles are high-value assets exposed to risks like accidents, theft, and liability claims, comprehensive insurance ensures financial protection against unforeseen events. Key policies typically include commercial auto liability, collision, and comprehensive coverage, alongside optional protections like rental reimbursement or uninsured motorist policies. Additionally, understanding local regulations and client requirements is essential to tailor your coverage effectively. By prioritizing robust insurance, you not only mitigate operational risks but also build trust with customers, laying a foundation for long-term success in this competitive industry.

- Essential Insurance Considerations for Starting a Car Rental Business

- What insurance do I need to start a car rental company?

- How much does insurance cost for a car rental business?

- What insurance does a rental company need?

- What kind of insurance do I need to rent my car out?

- Frequently Asked Questions (FAQs)

Essential Insurance Considerations for Starting a Car Rental Business

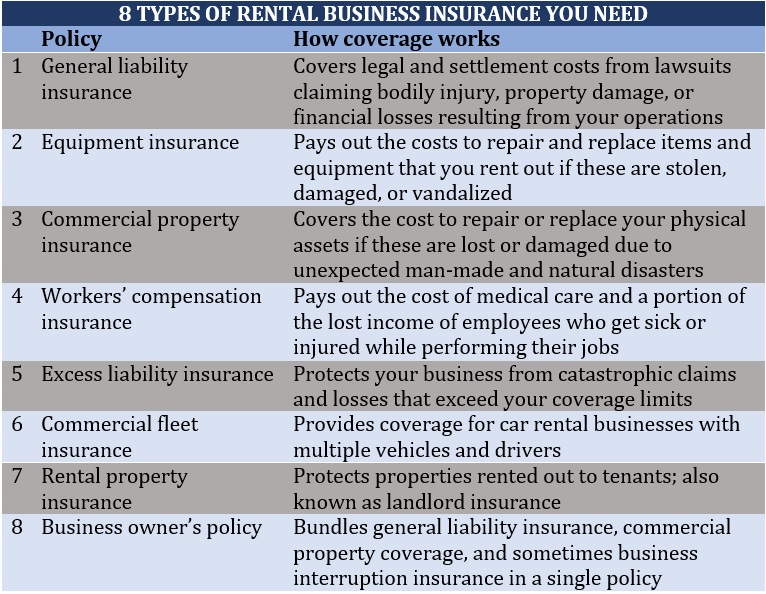

1. Understanding Liability Insurance for Car Rental Businesses

Liability insurance is a cornerstone of car rental business insurance. It protects your company from financial losses if a rented vehicle causes bodily injury or property damage to third parties. This coverage is often legally required and addresses medical expenses, legal fees, and repair costs for affected parties. Without adequate liability insurance, your business could face devastating lawsuits.

See AlsoDump Trailer Rental Business Insurance| Coverage Type | What It Includes | Why It Matters |

|---|---|---|

| Bodily Injury Liability | Covers medical costs for injured parties | Prevents out-of-pocket expenses |

| Property Damage Liability | Pays for repairs to third-party property | Mitigates legal disputes |

| Legal Defense Costs | Covers attorney fees and court expenses | Protects business assets |

2. Physical Damage Coverage for Rental Vehicles

Physical damage coverage safeguards your fleet against collisions, vandalism, or natural disasters. This includes collision insurance (for accidents) and comprehensive insurance (for non-collision incidents). Rental businesses must ensure their vehicles are protected to avoid costly repairs or replacements.

| Coverage Type | Key Protections | Common Scenarios |

|---|---|---|

| Collision Insurance | Repairs after accidents | Fender benders, crashes |

| Comprehensive Insurance | Damage from theft, fire, floods | Hailstorms, stolen vehicles |

| Theft Protection | Reimbursement for stolen cars | Vehicle theft by renters |

3. Commercial Auto Insurance vs. Personal Auto Insurance

Commercial auto insurance is tailored for business use, covering risks specific to rental operations. Personal auto insurance won’t suffice, as it excludes business-related incidents. Commercial policies often include higher liability limits and coverage for multiple drivers.

See AlsoVending Machine Business Insurance| Aspect | Commercial Auto Insurance | Personal Auto Insurance |

|---|---|---|

| Coverage Scope | Business activities, rental periods | Personal use only |

| Liability Limits | Higher to protect business assets | Lower, for individual risks |

| Driver Flexibility | Covers multiple renters | Restricted to named drivers |

4. Business Interruption Insurance for Unexpected Downtime

If your rental business halts operations due to a covered event (e.g., a fire or flood), business interruption insurance compensates for lost income and ongoing expenses like employee salaries or loan payments. This ensures financial stability during recovery periods.

| Coverage Component | Details | Example Scenario |

|---|---|---|

| Lost Revenue | Replaces income during closure | Facility damaged by storm |

| Operating Expenses | Covers rent, utilities, payroll | Temporary relocation costs |

| Disaster Recovery | Funds for reopening | Rebuilding after a fire |

5. Evaluating Insurance Costs and Coverage Limits

Balancing premium costs and coverage limits is critical. Underinsuring exposes your business to risk, while overinsuring inflates expenses. Assess factors like fleet size, vehicle value, and rental terms to customize a cost-effective policy.

See AlsoDoes Liability Insurance Cover Theft?| Factor | Impact on Insurance | Considerations |

|---|---|---|

| Fleet Size | Larger fleets = higher premiums | Discounts for bulk policies |

| Vehicle Type | Luxury cars cost more to insure | Prioritize durability |

| Deductible Amount | Higher deductibles lower premiums | Ensure affordability |

What insurance do I need to start a car rental company?

Commercial Auto Liability Insurance

Commercial auto liability insurance is essential for any car rental business. It covers damages or injuries caused to third parties if your rental vehicles are involved in an accident. This includes medical expenses, legal fees, and property damage. Key considerations include:

See AlsoWhat Licenses and or Permits Do I Need for a Mobile Mechanic Business?- State minimum requirements: Ensure coverage meets or exceeds your state’s liability limits.

- Per-vehicle vs. fleet coverage: Decide whether to insure individual vehicles or the entire fleet.

- Additional endorsements: Consider adding non-owned or hired auto coverage for employees using personal vehicles for business.

Physical Damage Coverage (Collision and Comprehensive)

Physical damage coverage protects your rental vehicles from accidents, theft, vandalism, or natural disasters. This includes both collision (damage from accidents) and comprehensive (non-collision events) policies. Important aspects include:

- Deductible options: Choose deductibles that balance affordability and risk exposure.

- Diminishing deductibles: Some policies reduce deductibles if the vehicle remains claim-free.

- Loss of use: Coverage for lost rental income during vehicle repairs.

Uninsured/Underinsured Motorist Coverage

This coverage protects your business and customers if an at-fault driver lacks sufficient insurance. It covers medical expenses and vehicle repairs. Key points include:

See AlsoCarry Liability Insurance- State-specific requirements: Some states mandate this coverage for rental companies.

- Customer protection: Reduces disputes with renters over accident-related costs.

- Stackable coverage: Allows combining multiple policies for higher limits.

General Liability Insurance

General liability insurance covers non-auto-related risks, such as slip-and-fall accidents at your rental office or property damage caused by employees. Considerations include:

- Premises liability: Covers injuries occurring at your business location.

- Product liability: Protects against claims related to vehicle defects.

- Legal defense costs: Covers attorney fees even for frivolous lawsuits.

Contingent Liability Coverage

Contingent liability coverage addresses gaps when renters fail to purchase adequate insurance or breach rental agreements. It ensures your business isn’t liable for their negligence. Focus on:

- Renter non-compliance: Covers damages if renters violate contract terms.

- Excess coverage: Acts as secondary insurance after the renter’s policy is exhausted.

- Risk mitigation: Requires strict rental agreements to enforce renter responsibilities.

How much does insurance cost for a car rental business?

Factors Influencing Insurance Costs for a Car Rental Business

The cost of insurance for a car rental business depends on variables like business size, vehicle types, geographic location, coverage limits, and claims history. High-risk areas or luxury fleets typically incur higher premiums.

- Business size: Larger fleets may qualify for volume discounts but face higher overall costs.

- Vehicle value: Luxury or specialty vehicles increase premiums due to higher repair/replacement costs.

- Location: Urban areas with higher theft or accident rates often raise insurance expenses.

Average Insurance Cost Ranges for Car Rental Companies

Car rental businesses typically pay between $5,000 to $20,000 annually per vehicle, depending on coverage. Small companies might spend $50,000–$150,000 yearly, while larger enterprises could exceed $500,000.

- Basic liability coverage: Starts at $3,000–$7,000 per vehicle annually.

- Full coverage: Ranges from $8,000–$20,000 per vehicle annually.

- Commercial umbrella policies: Add $1,000–$5,000 yearly for extended liability protection.

Types of Insurance Coverage Required for Car Rental Businesses

Mandatory policies often include liability insurance, collision coverage, and comprehensive insurance. Optional add-ons like loss damage waiver (LDW) or uninsured motorist coverage may also apply.

- Liability insurance: Covers third-party injury or property damage claims.

- Collision coverage: Pays for vehicle repairs after accidents.

- Comprehensive insurance: Protects against theft, vandalism, or natural disasters.

Ways to Reduce Insurance Costs for a Car Rental Business

Lower premiums by implementing safety protocols, driver screening processes, and telematics systems. Bundling policies or opting for higher deductibles can also reduce expenses.

- Driver age restrictions: Enforce minimum age requirements to lower risk.

- GPS tracking: Install devices to monitor vehicle usage and prevent misuse.

- Claims management: Resolve minor incidents without insurer involvement to avoid rate hikes.

Comparing Insurance Providers for Car Rental Businesses

Evaluate insurers based on industry expertise, financial stability, and customer support. Request quotes from multiple providers and review policy exclusions carefully.

- Specialized insurers: Companies like Progressive Commercial or Liberty Mutual often cater to rental businesses.

- Policy flexibility: Look for customizable coverage options.

- Discounts: Inquire about multi-vehicle, loyalty, or safety program discounts.

What insurance does a rental company need?

General Liability Insurance

General liability insurance is essential for rental companies to protect against third-party claims involving bodily injury, property damage, or advertising injuries. This coverage is critical when clients or visitors experience accidents on the rental premises or due to rented equipment. For example, if a customer slips and falls in your store, this insurance can cover medical expenses and legal fees.

- Bodily injury claims: Covers medical costs if someone is hurt on your property.

- Property damage: Protects against damage caused by your business operations to third-party property.

- Legal defense fees: Includes attorney fees and court costs in case of lawsuits.

Commercial Auto Insurance

If the rental company offers vehicles, commercial auto insurance is mandatory. Unlike personal auto insurance, this policy covers business-owned or leased vehicles used for rentals. It safeguards against accidents, theft, or damage involving rental cars, trucks, or vans.

- Collision coverage: Repairs or replaces rented vehicles after accidents.

- Liability protection: Covers damages or injuries caused by rented vehicles to others.

- Uninsured motorist coverage: Protects renters if the other driver lacks insurance.

Property Insurance

Property insurance protects the rental company’s physical assets, including buildings, equipment, and inventory, from risks like fire, theft, or natural disasters. This ensures business continuity even after unexpected events damage your facilities or rental items.

- Building coverage: Insures the physical structure of rental offices or warehouses.

- Equipment protection: Covers tools, machinery, or electronics available for rent.

- Business interruption: Compensates for lost income during repairs or closures.

Workers’ Compensation Insurance

For rental companies with employees, workers’ compensation insurance is legally required in most regions. It covers medical expenses and lost wages if employees are injured or fall ill due to job-related activities, such as handling heavy equipment or operating machinery.

- Medical bills: Pays for treatments related to workplace injuries.

- Disability benefits: Provides income if an employee cannot work temporarily or permanently.

- Legal compliance: Avoids fines or penalties for non-compliance with labor laws.

Inland Marine Insurance

Inland marine insurance covers rented equipment or goods while in transit or at a client’s location. This is crucial for businesses renting out tools, generators, or event supplies that are frequently moved off-site.

- Transit coverage: Protects items during transportation.

- Off-premises damage: Insures against losses occurring at the renter’s site.

- Theft or vandalism: Covers stolen or vandalized equipment away from your premises.

What kind of insurance do I need to rent my car out?

1. Understanding Personal Auto Insurance Limitations

When renting out your car, your personal auto insurance may not cover commercial activities. Most policies exclude coverage if the vehicle is used for rental purposes.

- Check your policy for exclusions related to car-sharing or rental activities.

- Contact your insurer to confirm whether temporary rentals are permitted under your plan.

- Consider a commercial policy if your personal insurance does not provide adequate coverage.

2. Rental Platform Insurance Options

Many car-sharing platforms (e.g., Turo, Getaround) offer built-in insurance coverage for hosts. These policies vary by platform and location.

- Review the platform’s liability limits and deductible requirements.

- Understand coverage tiers (e.g., basic vs. premium plans).

- Verify gaps in coverage that may require supplemental insurance.

3. Commercial Rental Insurance Policies

For frequent rentals or high-value vehicles, a commercial rental insurance policy may be necessary. This provides broader protection tailored to rental activities.

- Assess your rental frequency to determine if a commercial policy is cost-effective.

- Ensure coverage includes liability, collision, and comprehensive damage.

- Compare quotes from insurers specializing in car-sharing or rental businesses.

4. Gap Insurance for Leased or Financed Cars

If your car is leased or financed, gap insurance is critical to cover the difference between the vehicle’s value and your remaining loan balance.

- Check lease/finance agreements for insurance requirements.

- Confirm if gap coverage is included in your existing policy or the rental platform’s plan.

- Purchase standalone gap insurance if existing coverage is insufficient.

5. Liability Protection and Umbrella Policies

Renting your car increases liability risks. An umbrella insurance policy can provide additional coverage beyond standard limits.

- Evaluate your liability limits on current auto and home insurance policies.

- Supplement with umbrella insurance to cover severe accidents or lawsuits.

- Ensure coverage extends to rental activities and third-party drivers.

Frequently Asked Questions (FAQs)

What Types of Insurance Are Essential for a Car Rental Business?

Liability insurance, collision damage waiver (CDW), and comprehensive coverage are critical for a car rental business. Liability insurance protects against third-party claims for bodily injury or property damage. A CDW covers repairs or replacement costs if a rental vehicle is damaged, while comprehensive coverage addresses non-collision incidents like theft, vandalism, or natural disasters. Additionally, uninsured/underinsured motorist coverage is recommended to safeguard against drivers without adequate insurance.

How Much Does Insurance Cost for a Car Rental Business?

Insurance costs vary based on factors like fleet size, vehicle types, and coverage limits. On average, annual premiums range from $5,000 to $20,000+ for small to mid-sized businesses. High-value vehicles or operating in high-risk areas may increase costs. Working with an experienced insurance broker specializing in commercial auto policies can help tailor coverage to your budget while minimizing gaps.

Is Rental Car Insurance Mandatory for Customers?

While not always legally required, offering optional insurance add-ons (e.g., CDW, personal accident insurance) is standard practice. However, liability insurance is typically mandatory to operate legally in most jurisdictions. Ensure your business complies with local regulations and clearly communicates coverage options to customers to avoid disputes.

What Steps Should I Take to Secure Insurance for a Car Rental Business?

Start by assessing risks (e.g., fleet value, location hazards) and researching insurers specializing in commercial auto or rental industry policies. Prepare documentation like business licenses, vehicle registrations, and driver records. Compare quotes, review policy exclusions, and confirm coverage for employee drivers and renters. Regularly update your policy as your fleet or operations expand.

Leave a Reply

Our Recommended Articles